Fintech giant PayPal (NASDAQ:PYPL) reported better-than-expected third-quarter results earlier this month. Shares have advanced 15% over the past month but are still down nearly 19% year-to-date due to concerns about growing rivalry in the fintech space and the pressure on PayPal’s margins. Recent comments from some analysts have indicated that the company is losing market share to rivals, especially Apple (NASDAQ:AAPL). Let’s delve deeper.

PayPal Losing Ground to Rivals

PayPal’s Q3 2023 revenue grew 8% to $7.4 billion, while total payment volume (TPV) grew 15% to $387.7 billion. Moreover, adjusted EPS increased over 20% year-over-year to $1.30. However, the company’s GAAP operating margin contracted 59 basis points to 15.7% while adjusted operating margin fell 18 basis points to 22.2%.

Rising competition is impacting the company’s branded checkout business and hurting margins. Moreover, the growth in lower-margin offerings like Braintree (offers unbranded payment solutions to merchants) is also weighing on PayPal’s margins.

The entry of tech giants Apple and Alphabet (NASDAQ:GOOGL) in the fintech space through their Apple Pay and Google Pay offerings, respectively, has increased the rivalry in this growing market. PayPal’s products like Braintree also face competition from private players like Stripe (which is reportedly gearing for an IPO).

Analysts’ Cautious Tone

On Tuesday, Evercore analyst David Togut reiterated a Hold rating on PYPL stock with a price target of $65, noting that Cyber Week data on online spending indicates potential share loss in PayPal’s core checkout business.

Togut said that as per a Salesforce (NYSE:CRM) report, from November 21 through November 26, 2023, PayPal’s U.S. and global usage declined 4% and 2%, respectively, underperforming overall Wallet Pays, which rose 53% in the U.S. and 59% worldwide. The report revealed that PayPal processed 13% and 14% of total Cyber Week online transactions in the U.S. and globally, respectively.

Togut contended that while the Salesforce data does not include Cyber Monday sales, he does not expect any significant change in the trends highlighted by the report. He acknowledged that the company has taken initiatives to reduce friction at checkout, with password-less checkouts accounting for more than 70% of the total (excluding European Union) transactions. However, he thinks that these initiatives might not be enough to offset the notable rise in competition.

Similarly, on November 14, Mizuho analyst Dan Dolev slashed his price target for PayPal to $72 from $92, citing Branded checkout headwinds due to growing competition. Dolev said that his firm’s e-commerce checkout tracker indicates that Apple Pay continued to hurt PayPal’s Branded Checkout share in October, with outgoing web traffic from key merchants remaining lower compared to historical levels.

That said, Dolev remains upbeat about PYPL’s future growth potential and believes that opportunities to combine the PayPal and Venmo platforms and create a global digital wallet could mitigate worries about market share losses to Apple Pay.

Is PYPL a Buy, Sell, or Hold?

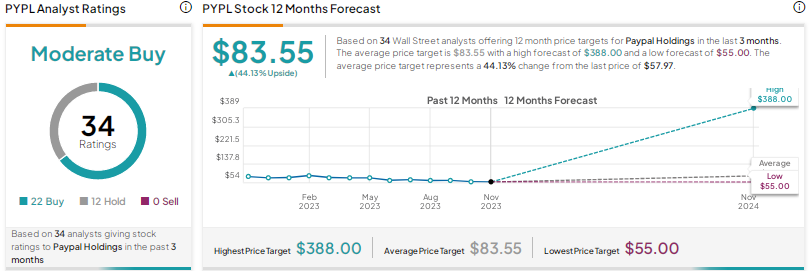

Overall, Wall Street is cautiously optimistic about PayPal, with a Moderate Buy consensus rating based on 22 Buys and 12 Holds. The average price target of $83.55 implies 44% upside potential.

Conclusion

PayPal’s declining operating margin and intense competition have raised concerns about the company’s near-term growth potential. However, the company is taking steps to reduce costs and introduce innovative solutions, which might drive long-term growth in the fintech market.