ONE Gas (NYSE:OGS) offers reliable income backed by a strong track record of dividend increases. The Oklahoma-based natural gas distribution utility, serving 2.3 million customers, projects enduring earnings and dividend growth in its multi-year outlook. However, the prospects for meaningful dividend hikes are limited. Consequently, while ONE Gas may be appealing to conservative income-focused investors, I hold a neutral stance on the stock.

What’s Supporting ONE Gas’ Positive Multi-Year Outlook?

The level of predictability attached to its dividend makes ONE Gas a real gem for investors looking for reliable income. This is what sets it apart in the world of income-oriented investments. Essentially, ONE Gas is what I like to call a “sleep well at night” stock. This is because the company’s management is able to offer a multi-year outlook on both earnings and dividend growth, reducing uncertainty in the stock’s investment case.

But what exactly makes management confident enough to provide a multi-year outlook?

To begin with, it’s ONE Gas’ market share domination in the jurisdictions in which it operates. With an impressive network comprising 44,500 miles of distribution mains and transmission pipelines, ONE Gas smoothly supplies natural gas to about 2.3 million customers.

As a dominant force in the Kansas and Oklahoma markets, ONE Gas commands an impressive 71% and 88% market share, respectively. Extending its reach into Texas, the company holds a respectable 13% market share in the Lone Star State. While this may seem like a soft market presence, it’s not really, given that the market in Texas is notably more fragmented. In fact, despite its seemingly small market share, ONE Gas proudly claims its position as the third-largest gas distribution utility in this state.

Further contributing to the predictability of its future cash flows is the regulatory framework within which ONE Gas operates. Distribution base rates, crucial to ONE Gas’ future revenue, are set by state authorities. Essentially, authorities want to ensure that utility companies receive fair and reasonable returns on their capital investments. This well-defined rate-setting process gives ONE Gas a solid foundation to offer highly precise outlook estimates for its medium-term net income and dividend growth.

To quantify this argument, ONE Gas’ management forecasts base rate increments of 7% to 9% through 2028. This, coupled with prudent customer base expansion estimates, consistent natural gas consumption patterns, and predetermined CapEx requirements and share dilution, leads management to expect EPS growth of between 4% and 6% over the same period.

Meanwhile, adhering to a commitment to maintaining a healthy payout ratio, the dividend is expected to experience a steady growth rate of about 1% to 2% over the same period, ensuring a reliable income stream for investors.

Is ONE Gas’ Dividend Actually Attractive?

Backed by a robust multi-year outlook, ONE Gas offers a highly predictable dividend, projected to keep rising for years to come. ONE Gas investors are used to the company’s consistent dividend increases, with the company now boasting nine consecutive years of hikes. In fact, with ONE Gas having already paid four $0.65 quarterly dividends, investors are expecting another increase in February, which is when ONE Gas’ hikes are usually declared.

Unfortunately, this upcoming dividend increase won’t be as attractive as those in the past. Management’s dividend growth outlook, which projects hikes of about 1-2%, implies a striking deceleration from ONE Gas’ past dividend hikes. For context, the company has increased its dividend by a compound annual rate of about 10.9% over the past seven years.

Because of this sudden deceleration, I would argue that ONE Gas’ dividend isn’t that attractive despite being attached to a predictable growth outlook. Essentially, dividend growth is set to underperform inflation, eroding the main factor most investors hold utilities for (i.e., income).

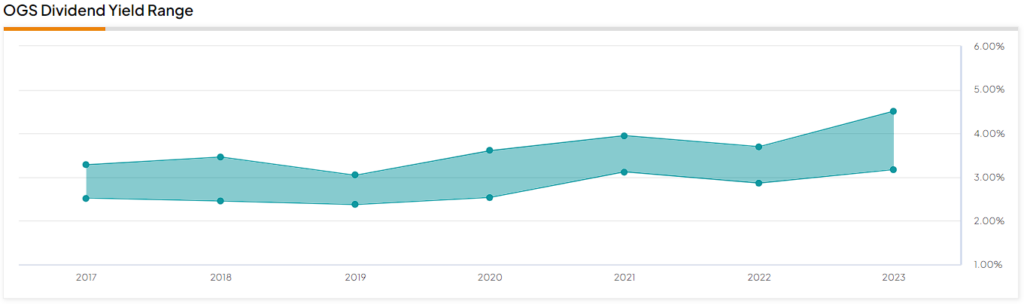

It’s not like the dividend yield (now at 4.3%) hovers in the high-single to low-double digits, thereby justifying soft dividend growth expectations. Investors can likely find equally attractive yields out there with much stronger dividend growth potential. Sure, the multi-year outlook is nice, and management’s decision to maintain a payout ratio between 55% and 65% is prudent, but that can’t do enough to increase investors’ attraction to the stock.

Evidently, since the company revised its dividend growth to 1-2% (from 4-6% previously), shares have remained under notable pressure. Even with most utilities recovering in recent months due to the market expecting interest rate cuts this year, ONE Gas stock has notably trailed behind.

Currently, shares are trading at their 2016 levels, with the 4.3% yield positioned at the upper end of its historical range. Clearly, investors are displaying a lack of interest in the stock despite this, as the dividend appears poised for stagnation in the years ahead.

In this context, I believe that the stock is best suited for highly conservative income-focused investors who may view ONE Gas as an investment akin to bonds.

Is OGS Stock a Buy, According to Wall Street?

Turning to Wall Street, analysts also seem to have mixed feelings about the stock. ONE Gas features a Hold consensus rating based on four Holds and one Sell rating assigned in the past three months. At $62, the average OGS stock forecast suggests just 5.3% upside potential.

The Takeaway

In conclusion, ONE Gas presents itself as a reliable choice for conservative income-focused investors, boasting a strong track record of dividend increases and a “sleep well at night” stock status.

The company’s dominant market position, extensive network, and regulatory framework contribute to the predictability of its future cash flows. Despite management providing a multi-year outlook, however, the rather soft dividend growth projections diminish the attractiveness of ONE Gas compared to alternative investments.

In fact, while suitable for conservative investors, the stock may struggle to attract a broader audience as the dividend appears poised for stagnation in the years ahead. Hence, meaningful upside prospects could fail to materialize.