In this piece, I evaluated two artificial intelligence (AI) related stocks, Nvidia (NASDAQ:NVDA) and Ambarella (NASDAQ:AMBA), to determine which is better. Upon closer analysis, it looks like NVDA is the better pick, but caution is advised due to its recent run-up and upcoming earnings report.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Artificial intelligence has long been a hot topic, but even more so since OpenAI released its ChatGPT AI model. Although valuation is more important now than it was a couple years ago, investors are so excited about AI that they’re pushing shares of AI-relevant companies skyward — with no consideration for fundamentals or valuation.

NVDA and AMBA are both semiconductor companies. The three-year average price-to-earnings (P/E) ratio for the semiconductor industry is around 26 times, while the three-year average price-to-sales (P/S) ratio is around 5.5 times. However, these averages are of little use when the market is in euphoria mode.

Without further ado, let’s take a look at NVDA and AMBA.

Nvidia (NASDAQ:NVDA)

Nvidia is one of those stocks that just keep on giving. On the one hand, its multiples are through the roof, but on the other, there could be more gas left in the tank — eventually. The company’s multiples remain below where they’ve traded during past peaks, but next week’s earnings report could send its shares lower if the company disappoints, suggesting a neutral view might be appropriate.

Investors have a voracious appetite for Nvidia stock whenever some new technology is linked to the company. In recent years, the shares have gone on wild rides around the explosions of interest in cryptocurrency mining, electric vehicles, and now artificial intelligence.

Since going public in 1999, Nvidia has returned well over 27,000%, and since the beginning of 2023, it has gained nearly 60%. However, Nvidia shares remain significantly below their late-2021 peak of over $330. The chipmaker’s trailing P/E stands at around 97.7 times, while its P/S is around 19 times.

Nvidia’s P/E peaked at around 110 in late 2021, while its P/S was around 35 times, suggesting there might be more upside left. The chipmaker’s sales have risen steadily in recent years, granting it growth-stock status as sales rose from $10.9 billion in 2020 to $28.6 billion for the last 12 months.

Nvidia also generates plenty of free cash flow, at $8.1 billion for the fiscal year that ended in January 2022. Over the last 12 months, the chipmaker reported $4.8 billion in free cash flow after repurchasing $10.6 billion in shares. Its balance sheet is also solid.

With analysts like Vivek Arya of Bank of America Securities proclaiming that Nvidia could win big in the “AI arms race,” there’s plenty to like and perhaps even more upside, but after its latest run, Nvidia is ultra-risky.

What is the Price Target for NVDA Stock?

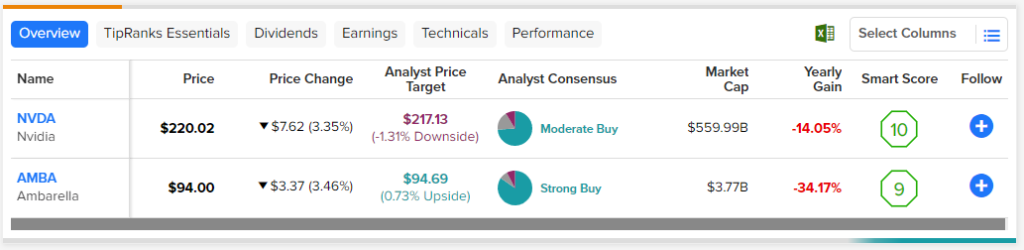

Nvidia has a Strong Buy consensus rating based on 19 Buys, five Holds, and one Sell rating assigned over the last three months. At $212.04, the average Nvidia stock price target implies downside potential of 3.6%.

Ambarella (NASDAQ:AMBA)

Ambarella shares many of the same stock-price drivers, but a deeper look at its fundamentals reveals that the company isn’t nearly as strong. Essentially, the risk of Ambarella stock running out of gas is just as high as Nvidia’s, but its comparably weak fundamentals suggest a bearish view might be appropriate.

The first thing a deep dive into Ambarella reveals is its lack of profitability. While the company has a solid track record of revenue and earnings beats, it just can’t seem to turn a profit, although it does generate a small amount of free cash flow.

Although investors have happily granted Ambarella growth-stock status with soaring multiples despite its lack of profits, the chipmaker doesn’t deserve it. The company hasn’t been growing its revenue fast enough to be granted growth status.

Ambarella’s P/S stands at around 10.6 times, remaining far below its late-2021 peak at around 26.8 times, but investors should be asking when Ambarella will become profitable. In November 2021, analysts said the chipmaker was near breakeven, so they projected profitability in 2024. In June 2022, analysts projected GAAP profitability in Fiscal 2025.

While Ambarella has a healthy balance sheet with almost no debt, its valuation and lack of profitability are unbreachable barriers for now.

What is the Price Target for AMBA Stock?

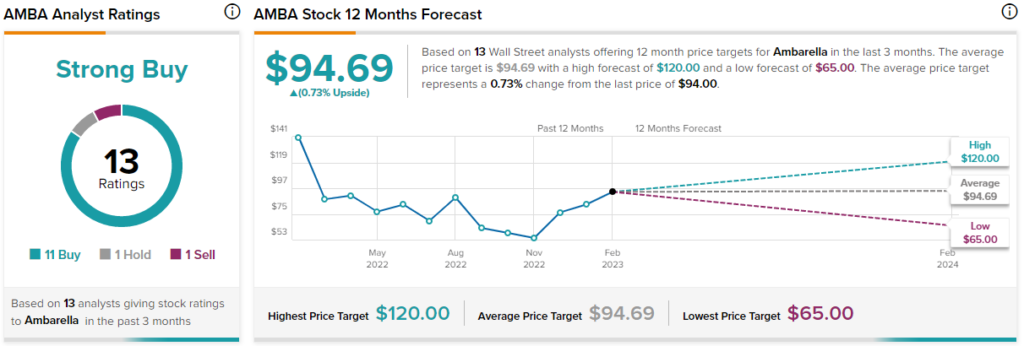

Ambarella has a Strong Buy consensus rating based on 11 Buys, one Hold, and one Sell rating assigned over the last three months. At $94.69, the average Ambarella stock price target implies upside potential of 0.73%.

Conclusion: Neutral on NVDA, Bearish on AMBA

Nvidia is a high-risk stock as it continued to skyrocket despite the over $50 million in insider sales over the last three months. While the stock looks good over the long term, investors might want to look for a better entry point, and one could appear following the next earnings report.

Meanwhile, Ambarella is not a growth stock, although it’s valued like one. Aside from its balance sheet, there’s not much to like in the near term.