Nike (NYSE:NKE) stock is fresh off a forgettable 2023, actually slipping by around 13% as the rest of the market marched confidently higher. Going into the new year, many analysts on Wall Street see Nike running higher from here. I’m inclined to agree and am staying bullish.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Indeed, macro headwinds have challenged consumer appetite for discretionary (nice-to-have) goods, like those in the apparel space. But with Lululemon (NASDAQ:LULU) continuing to stretch (forgive the pun) to hit a new all-time high last year, many may be wondering if the recent wave of underperformance is more of a Nike problem than something to be blamed on the somewhat harsh industry environment.

Undoubtedly, Lululemon seems to be one of the few outliers in the big-name apparel space today, with its stock constantly making higher highs. As one of the original athleisure pioneers with some of the heftier prices in the space (Lululemon leggings are pricier than comparables offered by the likes of Nike and Gap’s (NYSE:GPS) yoga-wear brand Athleta), one would think consumers would have flocked to more affordable alternatives, rather than loosen the purse strings on the priciest product of the batch.

Lululemon’s Fantastic 2023 Shows Us There’s Still Life in Apparel

The fact that Lululemon outdid rivals and beat the S&P 500 (SPX) amid last year’s sluggish consumer conditions is a testament to the power of the Lululemon brand. As the Vancouver-based yoga-wear firm expands internationally and delves into new product categories like men’s wear and footwear, it could become a serious competitor to apparel rivals like Nike. In many ways, Lululemon’s becoming less of a yoga play and more of an apparel play — one that’s sure to keep Nike on its toes.

Despite competitive pressures arising from Lululemon, it’s hard to bet against Nike. The apparel giant has a robust brand and could take a page out of Lululemon’s lifestyle marketing playbook to save money and better resonate with more prospective consumers.

Nike is known for spending a pretty penny on big-name athletes to dawn and promote the unmistakable swoosh. In contrast, Lululemon has stealthily strengthened its brand via social-media influencers, many of whom ask for nothing more than free Lululemon products. I think it’s safe to say that Lululemon has gotten a better bang for its buck on the marketing front.

Only time will tell if Lululemon sags from here as consumers continue to feel the pinch in the new year. Regardless, I’d much rather be in Nike than Lululemon for 2024, as its cost-cutting plan looks to save the firm as much as $2 billion.

With a sizeable moat and plenty of growth levers to fend off rivals (such as Lululemon) and stage a recovery, Nike stock finally looks like a play that value-conscious investors can appreciate. As Nike spends more deliberately while keeping tabs on what Lululemon’s doing right, I wouldn’t be too surprised if Nike ends up as the top-performing apparel stock of 2024. As for Lululemon, perhaps it’s poised to become a downward dog after last year’s scorching gains.

Nike Stock: A Fairly Low Bar for the New Year

There has rarely been a time when you can pick up shares of Nike at less than 30 times trailing price-to-earnings. After sagging to $102 and change, the $155.4 billion apparel giant goes for just 29.76 times trailing price-to-earnings, well below its five-year historical average of around 39.2 times. Just a few weeks ago, Nike’s management team warned about slower consumer spending. Thus, the bar now seems quite low, especially relative to the likes of Lululemon.

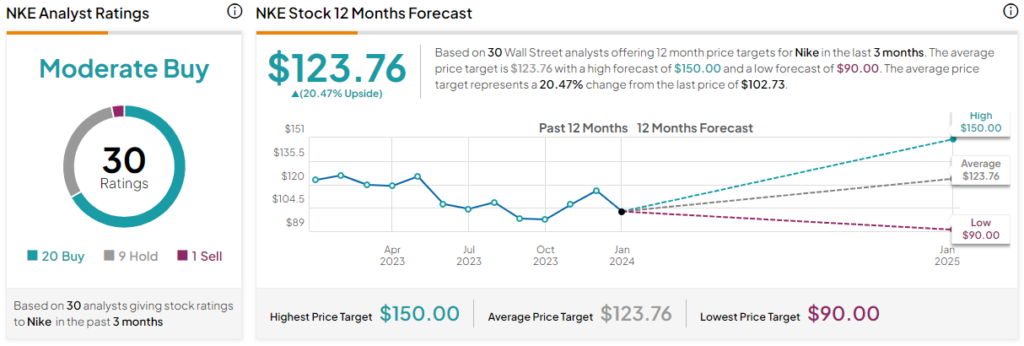

In early December, a Goldman Sachs (NYSE:GS) analyst gave NKE stock a Buy rating. Goldman Sachs’ Brooke Roach currently has a $135.00 price target on the stock, which entails 32% upside from here. This isn’t even the highest price target on Wall Street. That title goes to Oppenheimer, which touts a $150.00 target, entailing around 47% upside.

For 2024, Roach sees “innovation” and the “marketing engine” as potential sales growth drivers. Additionally, headwinds such as share growth in rivals (like Lululemon) may already be priced in. Roach certainly seems to think today’s modest valuations already account for such competitive pressures and more.

I’m inclined to agree with Roach. Nike stock is in a historic rut, and that’s made shares close to the cheapest they’ve been in years.

Is NKE Stock a Buy, According to Analysts?

Nike stock is a Moderate Buy, according to analysts, with 20 Buys, nine Holds, and one Sell assigned in the past three months. The average NKE stock price target of $123.76 implies 20.5% upside potential.

The Takeaway: A Great Low-Tech Value Play

The apparel space can be difficult to invest in when recession expectations rise. Either way, it seems like a mild economic contraction is already a given when you have a look at Nike’s share price trajectory, making it a value play. Though Nike will eventually stack up against easier year-over-year comparables, the firm may need to step outside of its comfort zone to stay up to the likes of innovative rivals like Lululemon.

At this juncture, I’d bet that Nike will be more successful taking share in the yoga wear market than Lululemon did in footwear or menswear. Perhaps Nike needs to adopt a more Lululemon-like strategy in its retail stores and marketing to gain traction in the red-hot yoga-wear scene.