World-famous mining company Newmont (NEM) is keeping its costs reasonable and producing vast amounts of gold while also paying out a nice dividend. Yet, Newmont stock is beaten down – but that’s fine for opportunistic, contrarian investors. I am bullish on Newmont stock.

Denver, Colorado-headquartered Newmont mines for a number of minerals, including copper, silver, zinc, and lead. However, the company is best known for its aggressive gold production. During gold bull markets, Newmont’s strong focus on gold mining often translates to steady, robust gains for investors.

Perhaps you can see the gold price returning to $1,900 or even $2,000 before the end of the year and want to get some leverage through a tried-and-true stand-by mining stock. On the other hand, maybe you just like to collect and reinvest dividend payments for steady, long-term income. Also, you might consider yourself a dyed-in-the-wool value hunter with an eye for beaten-down gems.

Regardless of your reason(s) for considering Newmont stock, this is a great time to drill for potential profits with a well-known name in North American gold mining. If you truly believe in “buy low, sell higher,” then this is your opportunity to be bold with a power player in gold.

Inflation Has Created Problems for Gold Miners Like Newmont Stock

Price inflation is deeply affecting virtually all industries, and gold mining’s no exception to the rule. At the same time, the gold price seems to be going nowhere. This is due to a number of factors, such as China’s COVID-19 lockdowns, disruptions across the commodities supply chain, and the challenge of finding qualified workers. These headwinds have even affected the biggest Western Hemisphere-based gold miner of them all, Newmont.

This company has a massive $34.5 billion market cap and a vast resource base. Yet, Newmont isn’t immune to the common problems impacting resource companies around the world. Getting gold out of the ground is becoming an expensive proposition. There are two commonly used metrics to indicate just how expensive it is: costs applicable to sales (CAS) and all-in sustaining costs (AISC).

No matter which metric you choose, it’s clear that Newmont’s expenses have risen substantially. During 2022’s second quarter, Newmont’s CAS increased 23% year-over-year to $932 per ounce. Also, in that quarter, the company’s AISC rose 16% to $1,199 per ounce.

There really wasn’t much that Newmont could do about this. The company cited “inflationary pressures, driven by higher labor costs and an increase in commodity inputs, including higher fuel and energy costs” as the reasons for Newmont’s higher operating costs. Prospective investors should keep this in mind when evaluating Newmont’s quarterly performance, which really wasn’t too bad, considering the circumstances.

Newmont Delivered Impressive Financial Stats Despite Inflationary Issues

With inflation causing major problems for Newmont, you might expect the company’s Q2 2022 financial report to be a horror story. Yet, the company demonstrated surprising resilience. Starting with the top-line results, Newmont’s quarterly sales were nearly flat year-over-year at $3.058 million, compared to $3.065 million in the year-earlier period. So far, so good – not a horror story at all.

Checking in on Newmont’s balance sheet, the company actually managed to increase its cash flow from continuing operations, from $993 million in 2021’s second quarter to $1.033 billion in Q2 2022. Also encouraging is Newmont’s commitment to deploy the company’s $1 billion share buyback program “opportunistically in 2022, with $475 million remaining.”

Furthermore, Newmont is working through supply chain issues and widespread worker shortages to produce vast amounts of gold. From 1.45 million ounces of attributable gold production in last year’s second quarter, Newmont stepped it up to 1.5 million ounces in Q2 2022.

Will Newmont be able to maintain this aggressive pace of gold production? It’s entirely possible, at least from a financial standpoint. That’s because Newmont anticipates CAS of $900 per ounce and AISC of $1,150 per ounce in Fiscal Year 2022, which aren’t very different from the standards set in 2022’s second quarter.

Newmont Stock Could Offer Price Appreciation and Dividends

Is Newmont stock a dividend stock or a growth stock? That answer could actually be both, as at least one analyst is bracing for a share-price move while Newmont remains a yield king among gold miners.

Indeed, Canaccord Genuity analysts called the post-earnings-announcement sell-off in Newmont stock “overdone” while issuing an optimistic price target of $60. The Canaccord analysts cited Newmont’s steady gold production profile, strong balance sheet, and solid operating team as reasons for optimism. Moreover, Newmont’s 5.05% forward annual dividend yield is like the icing on the cake for the company’s prospective investors.

Finally, it should be noted that Newmont isn’t only a miner of gold. The company also explores for silver, lead, and zinc, which could be high-demand minerals in the U.S. as the nation attempts to rebuild its infrastructure while supporting the transition to vehicle electrification.

Is NEM a Good Stock to Buy?

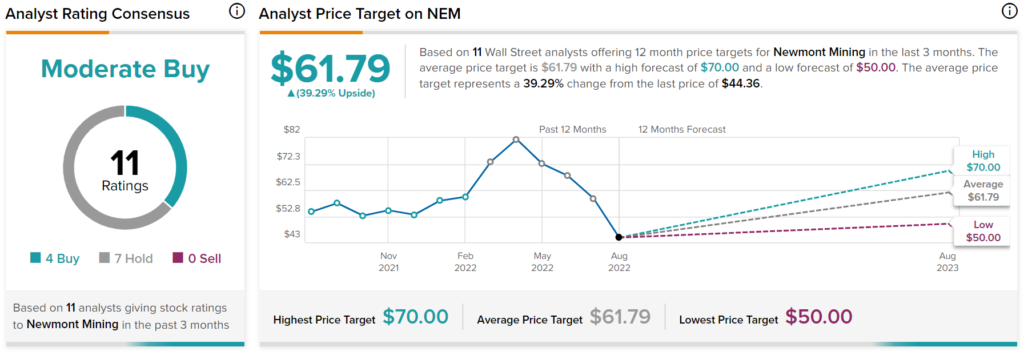

Turning to Wall Street, NEM has a Moderate Buy consensus rating based on four Buys and seven Holds assigned in the past three months. The average Newmont price target is $61.79, implying 39.3% upside potential.

Conclusion: Should You Consider Newmont Stock?

This is definitely the right time to think about owning shares of Newmont stock. At the very least, we can say that the math heavily favors Newmont. An AISC of $1,150 per ounce of gold is quite reasonable. If it costs that much to get an ounce of gold out of the ground, and gold’s trading between $1,700 and $1,800 per ounce, then Newmont should be able to turn a healthy profit.

Just imagine how much more profitable Newmont could be, then, if gold reaches $1,900 or $2,000 or more. In the meantime, you can collect dividend payments, and rest assured that Newmont is one of the more productive multi-mineral drillers in the world.