Jim Cramer, host of Mad Money on CNBC and the head of the CNBC Investing Club, is miffed with the fact that mass media and entertainment giant The Walt Disney Company (NYSE: DIS) is trading almost one to one with streaming giant Netflix (NASDAQ: NFLX).

“It is getting ridiculous that Disney trades almost one for one with Netflix. I have never seen a Netflix theme park but it can’t be as good as a real-life Squid Games,” Cramer tweeted. Which brings us to the intriguing question: which streaming giant is shaping up better in the post-pandemic era?

Let us have a look at both the entertainment companies’ current performances and valuations.

Disney Dashes Devotees

After reaping the losses from the pandemic-related closures, Disney’s amusement parks are flooded with visitors with the onset of the summer season. On the other hand, Disney’s streaming platform, Disney+, is also ripe with a series of new launches, attracting massive viewership.

Yes, inflationary pressures and recessionary fears are doubling down on Disney’s park visitations. However, international tourists and parks across the globe could make up for the lost cause. However, the rising interest rates and labor charges could nibble into the margins of the House of Mouse company, as overheads remain a daunting task to manage during times of an economic downturn.

DIS stock has lost 37.8% so far this year. The company is slated to report its third-quarter fiscal 2022 earnings on August 9, with the consensus earnings per share (EPS) figure pegged at $1.00.

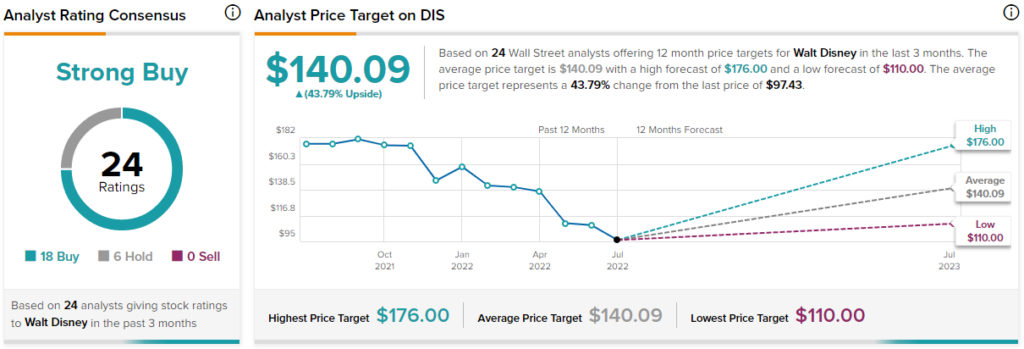

Yesterday, Citigroup analyst Jason Bazinet drastically cut the price target on DIS stock to $145 (48.8% upside potential) while maintaining a Buy rating.

Bazinet has lowered the FY23 estimates on expectations of higher expense growth but unchanged revenue estimates, resulting in declining margins. The analyst believes that recession fears are more severe for companies with higher advertising exposure and lower contractual revenue, like Disney.

However, analyst Barton Crockett of Rosenblatt Securities is highly optimistic about the stock and reiterated a Buy rating with a price target of $174 recently, which implies 78.6% upside potential to current levels.

Looking at the valuations, Disney currently trades at a price to sales (P/S) ratio of 2.28 times, which is above the sector median but way below its five-year average of 3.49 times. Notably, the price to earnings per share (P/E) ratio of 28.92 overshoots both the sector median and five-year average, making the stock look expensive at current levels.

The Street is highly optimistic about DIS stock with a Strong Buy consensus rating based on 18 Buys and six Holds. The average Walt Disney Company price forecast of $140.09 implies 43.8% upside potential to current levels.

Netflix Nets Subscriber Losses

Netflix is having a difficult time holding on to its subscriber base, which is slowly but surely declining quarter over quarter. NFLX stock has lost 68.3% so far this year. The “Stranger Things” streamer is slated to release its second-quarter Fiscal 2022 earnings on July 19. The consensus for EPS is pegged at $2.99.

Ahead of NFLX’s Q2 print, Stifel Nicolaus analyst Scott Devitt kept the model estimates unchanged while reiterating a Hold rating on the stock with a price target of $240. Devitt noted that, as per engagement data from Apptopia, engagement during Q2 showed modest growth over Q1 readings.

Furthermore, the analyst believes that Netflix’s advent into the ad-supported tier business is in its nascent stage and will take a while to materialize into a full-fledged cash-generating segment. However, “affordability constraints in international markets” may be a spoiler to the company’s growth plans alongside “heightened competition and potential maturity in core markets,” he noted.

Similarly, Needham analyst Laura Martin, who also has a Hold rating on NFLX stock, pointed out a couple of steps the company needs to take to improve its competitive advantage in the streaming industry.

As per Martin, Netflix needs to “a) launch its promised ad-driven streaming tier to expand its TAM; b) add sports and news content to improve its performance of the “Job to be Done” (i.e., entertain consumers); c) offer bundling with other products (to lower churn); and/or d) acquire a large film and TV content library (to lower churn).”

Turning to its valuation metrics, Netflix currently trades at a P/S ratio of 2.71x, which is above the sector median but more than halfway down its five-year average of 8.62x. On the contrary, its P/E ratio of 16.87x is trading much below its sector median and five-year average, implying that the stock is very cheap at current levels.

Analysts on the Street are extremely cautious about NFLX stock right now, with a Hold consensus rating based on ten Buys, 25 Holds, and six Sells. The average Netflix price forecast of $266.77 implies nearly 41% upside potential to current levels.

Closing Thoughts

Both Netflix and Disney are currently in shaky waters with the macroeconomic headwinds at play. However, with its diversified offering of theme parks, movies, and streaming services, Disney seems to be in a relatively better position than Netflix currently. Moreover, analysts are highly bullish on Disney than on Netflix.