Netflix’s (NFLX) earnings release for the third quarter is scheduled for October 19, after the market closes. Over the past year, shares of the world’s leading streaming entertainment service have surged 18.4%, and are currently trading at over $628. Positive earnings data could continue to take shares on an upward trajectory, so let’s take a closer look at what analysts on the Street are expecting.

Earnings Preview

Netflix EPS is expected to be $2.56 on revenues of $7.48 billion in the third quarter, while the company guided for earnings of $2.55 per share and revenues of $7.47 billion.

Meanwhile, the Earnings Whisper number, or the Street’s unofficial view on earnings, stands at $2.70 per share.

Prior Period Results

In the previous quarter, the company reported earnings of $2.97, up 86.8% from the prior-year quarter but missed the consensus estimate of $3.15. On the other side, net revenue jumped 19.4% to $7.34 billion and marginally surpassed analysts’ expectations of $7.32 billion. (See Netflix stock charts on TipRanks)

With mixed results, subscriber additions in the quarter surpassed the company’s projections. Paid net additions in the quarter totaled 1.5 million, above the company’s estimated 1 million.

Markedly, Netflix’s earnings history depicts mixed performance over the past four quarters, with upbeat revenues in all, but earnings miss in three of the four quarters.

See Insiders’ Hot Stocks on TipRanks >>

Factors to Watch For

Netflix, the subscription-based streaming service, has dominated the streaming market, with over 209 million paid memberships currently in over 190 countries. It streams TV series, documentaries, and feature films across a wide variety of genres and languages.

The company provides even more unique and diversified content, with the launch of its first original scripted TV series in 2012. Furthermore, when expanding its original programming efforts to many additional categories globally, the company invests heavily in the production and distribution of local and foreign-language content, along with international expansion.

In the first six months of 2021, Netflix’s content amortization grew 9% year-over-year, with $8 billion spending in cash on content, up 41%. Notably, 44 Emmy wins at the 2021 Emmy Awards reflect the streaming giant’s focus on the value of content. Remarkably, for the first time ever, Netflix has nabbed more Emmys than any other platform.

Granted, the COVID-19 pandemic has created some lumpiness in the company’s subscriber growth. Notably, the year 2020 recorded high growth, while Netflix is experiencing slower membership growth now, primarily due to rising competition and easing of lockdown measures.

Netflix is working its way through to improving its service for members and releasing the best stories globally. In the third quarter of 2021, a strong set of releases, such as new seasons of La Casa de Papel (aka Money Heist), Sex Education, Virgin River, and Never Have I Ever are expected to have fueled subscriber growth. Also, movies including Sweet Girl, Kissing Booth 3, Kate, and Vivo might have attracted new subscribers.

What’s more, higher revenues are expected in the third quarter, as Netflix has become popular in the Asia Pacific (APAC) and Latin America (LATAM) due to its varied content offerings in local languages in such regions. For Q3, Netflix expects global streaming paid net additions of 3.5 million, much above 2.2 million in the prior-year period.

However, Netflix’s results might have been impacted in the to-be-reported quarter on increasing competition from other streaming providers, including HBO Max, Peacock, Apple TV+ by Apple (AAPL), Disney+ by Disney (DIS), and Amazon (AMZN) prime video.

Notably, the recent release of the South Korean drama “Squid Game” has been the biggest ever launch hit for Netflix. Yet, investors are critical about whether it will enhance the company’s results in the third quarter, or will provide upbeat expectations for the fourth quarter, or both.

Analyst Recommendations

Prior to the third-quarter Netflix earnings report, Evercore ISI analyst Mark Mahaney has reiterated a Buy rating and a price target of $695 (10.62% upside potential) on the stock.

Mahaney said, “While we view the likelihood of significant price appreciation on the print to be relatively low, we believe that given the continued content slate strength heading into 2022, the risk-reward favors the upside and any potential weakness to share prices on the print would be short-lived.”

Another analyst, Morgan Stanley’s (MS) Benjamin Swinburne maintained a Buy rating on Netflix and increased the price target to $675 (7.43% upside potential) from $650.

Swinburne considers 2022 to be “a year of healthy and accelerating net [subscriber] additions, as the rebuilt content pipeline hits the services, starting in Q4” for Netflix.

Markedly, the analyst expects 25 million net additions in 2022, with the belief that mainly Europe and Asia will show strength.

Overall, the stock has a Moderate Buy consensus rating, based on 24 Buys, 5 Holds, and 3 Sells. The average Netflix price target of $648.90 implies 3.28% upside potential from current levels.

Website Traffic

According to SEMrush Holdings (SEMR), the world’s biggest website usage monitoring service, globally, Netflix’s website recorded a 4.76% monthly decline, year-over-year, in visits in September, while Q3 depicted a 6.52% quarter-to-date growth. Markedly, year-to-date website growth, compared to year-to-date website growth in the previous year, came in at 19.91%. (See Netflix’s website traffic on TipRanks)

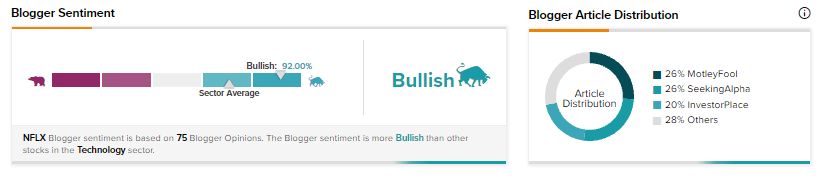

Bloggers Weigh In

TipRanks data shows that financial blogger opinions are 92% Bullish on NFLX, compared to a sector average of 71%.

Disclosure: At the time of publication, Priti Ramgarhia did not have a position in any of the securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates, and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices or performance.