Driven by the enthusiasm for all things AI, the semiconductor sector has outperformed the broader markets this year, with the SOX (the Philadelphia Semiconductor Index) – the sector’s barometer for overall performance – up by 49% year-to-date.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The gains have come against a difficult backdrop and an inventory correction that has continued to play out on the device side. Yet, Morgan Stanley analyst Joseph Moore believes that as the inventory correction runs its course over the coming months, the fundamentals for devices are “turning more positive.”

However, there’s a catch here. “In a perfect world,” notes the 5-star analyst, “that fundamental bottoming would be aligned with trough valuations.” But that is not the case, says Moore, given semis have bettered the overall market’s performance.

So, it’s time to be picky, and here, Moore recommends a “move to an overweight position in devices.” “While we still argue for being selective, the combination of recovering fundamentals and the importance of semiconductors in early stage AI argues for a higher than market weight exposure,” Moore explained. “Generally speaking, barring macro dislocation, we are past the bottom in some areas, and for most others, the bottom is in sight. Barring economic dislocation, things should improve over the course of 2024.”

So, with that in mind let’s now take a look at 3 semiconductor stocks Moore considers hot buys right now. We ran the trio through the TipRanks database to see what other experts make of these choices.

Don’t miss

- ‘Time to Upgrade,’ Says J.P. Morgan About These 2 Energy Stocks

- TipRanks’ ‘Perfect 10’ Picks: 2 Top-Scoring Stocks for 2024

- BMO Optimistic About Fintech Stocks in 2024; Here Are 3 Top Picks to Keep an Eye On

Qorvo, Inc. (QRVO)

First on our list is Qorvo, the North Carolina-based large-cap chip designer and manufacturer that has its hands in all of the leading-edge high-tech markets. Qorvo’s core business, the products that make up the bulk of its output, are top-end radio frequency (RF) and power chipsets that provide solutions in a range of applications, from aerospace/defense to IoT to mobile networking to infrastructure and power management. These are expanding niches, that combine high demand with exacting specifications, requiring quality in execution.

Qorvo has been delivering that for the better part of three decades, and in recent years has been moving into 5G technology as well. The company’s 5G-enabled chips can be found in both the new wireless infrastructure and in the newer handsets and devices, where strong execution is required to ensure that the new systems are viable.

This company has a world-wide footprint, which exposes it to multiple headwinds – but also provides plenty of strength to offset them. Case in point, Qorvo is facing some pressure in the Chinese markets, where that country’s post-COVID recovery has grown somewhat muted recently. On the positive side, however, Qorvo finds meaningful support from its stable business with the defense industry, and its overall high-quality content story.

Looking at Qorvo’s recent financial performance, we find that the last reported quarter, fiscal 2Q24 (September quarter), showed a marked turnaround from the previous three quarters. The nine months ending with June 30 of this year saw a marked reduction in the company’s revenues and earnings, but the quarter ending on September 30 showed a return to higher levels at both the top and bottom lines.

In the report for 2Q of fiscal year 2024, Qorvo showed a top line of $1.1 billion, a total that was down 5.2% year-over-year but up 70% from Q1 – and beat the forecast by approximately $100 million. The company had a non-GAAP operating income of $279 million, or $2.39 per share; that EPS figure was 62 cents per share better than had been anticipated. The company’s forward guidance for the quarterly ending this month, fiscal 3Q24, is upbeat, predicting revenue of $1 billion (compared to a consensus estimate of $991.8 million) and a non-GAAP EPS of $1.65 at the midpoint (compared to a $1.62 consensus).

This forms the background for Moore’s comments on Qorvo. He notes the potential for long-term earnings growth here, writing, “With the momentum from increased Apple share and snapback in China Android, Qorvo has enough GM expansion to get to $10+ EPS by CY2025. The stock currently trades at 10x CY25 EPS, which is on the lower end of their historical range and looks inexpensive given expectations of strong earnings growth. Valuation is going to remain at the lower end of US semis, given long term share pressure from China, high customer concentration, and modest smartphone growth, but from this level there is still material upside…”

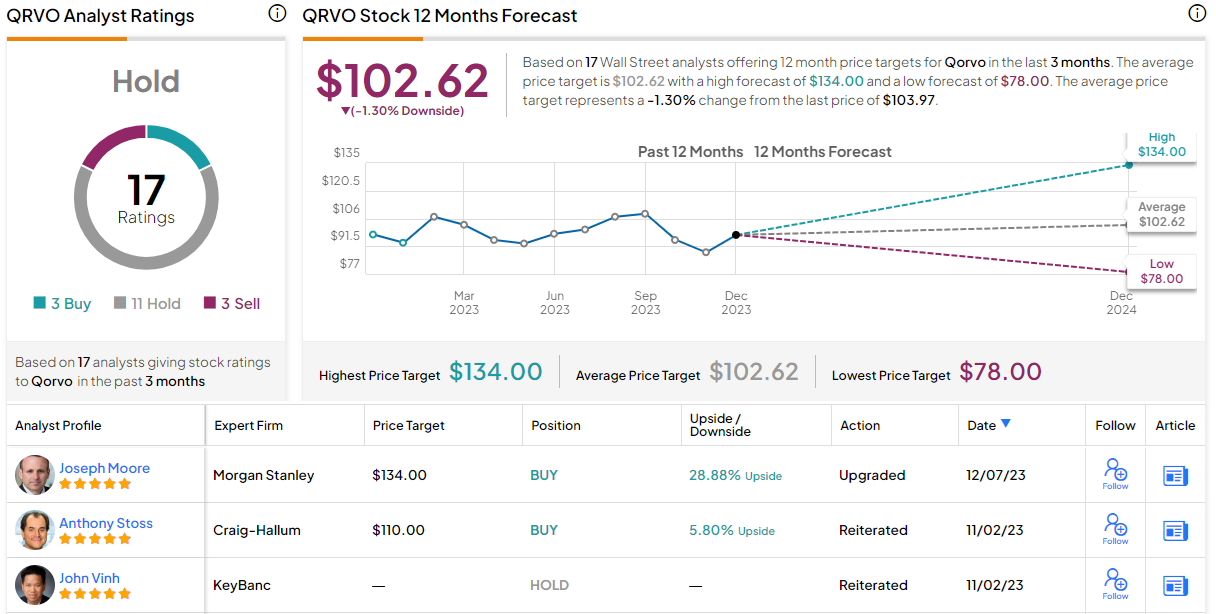

Bottom-line, Moore bumps the stock’s rating from Equal-weight to Overweight (Buy). His price target, now set at $134 (up from $120), implies an upside of 29% for the year ahead. (To watch Moore’s track record, click here.)

Where Moore and Morgan Stanley are bullish, the Street generally is more cautious; the shares have a Hold consensus rating based on 17 recent analyst reviews with a breakdown of 11 Holds, and 3 Buys and Sells, each. The average price target is $102.62, suggesting the shares will stay rangebound for the time being. (See Qorvo’s stock forecast.)

Ambarella (AMBA)

Next up is Ambarella, a $2.3 billion fabless chip company that lies squarely in the small- to mid-cap category. Ambarella specializes in designing, testing, marketing, and selling its chipsets, producing prototypes and contracting the regular production line runs to dedicated chip foundries. It’s a division-of-labor model that has worked well in the semiconductor industry.

On its own end, Ambarella works in the video application niche, creating chipsets that that are optimized for image processing and high-resolution video compression. The company’s products are found in a wide range of digital imaging technologies and systems, from wearable cameras to vehicle dash-cams, to pocket sized digital stills and video cameras to driver assistance systems and autonomous vehicle ‘eyes.’ The common factor among these applications is a need for high definition video at low power – a specialty niche that Ambarella has filled well.

This has resulted in a line of chips designed specifically for battery-powered devices, where power consumption is a primary concern. Ambarella’s products are known for outperforming in power efficiency, sometimes by a factor of 5 or more, while continuing to provide superior results in picture clarity and file compression. It all comes down to the proven quality of Ambarella’s low-power systems-on-chip high-quality video and image resolution.

Despite the company’s leading role in a growing niche, AMBA shares have lost heavily in the past year. The stock is down approximately 27% in the last 12 months, and earnings have been running negative for several quarters. The decline came as customer firms were working to clear out old inventory, resulting in lower demand for new products. At the end of November, however, Ambarella’s fiscal 3Q24 results (October quarter), while down y/y, beat the forecast at the top and bottom lines.

The company’s revenue total was $50.6 million for fiscal Q3, down 39% from the previous year’s quarter but sliding in some $590,000 above expectations. The bottom-line earnings figure came to a loss of 28 cents per share by non-GAAP measures; this was 11 cents per share narrower than had been anticipated.

Turning to Moore’s view, we find the analyst setting this stock up as one of his favorite SMID chip firms. Moore is bullish on the risk-reward and the long-term potential to beat the headwinds, saying of the company, “For investors looking for SMID exposure, we continue to prefer AMBA on their long-term risk reward. We see high strategic value in AMBA’s technology over the long term, which we believe will support meaningful upside in the future. However, we do remain cautious near term as they are currently in the middle of a severe inventory correction and are seeing market share pressure in their legacy video. We expect headwinds in their legacy surveillance business to ease next year, and remain positive on the importance of the technology solutions the company provides long term.”

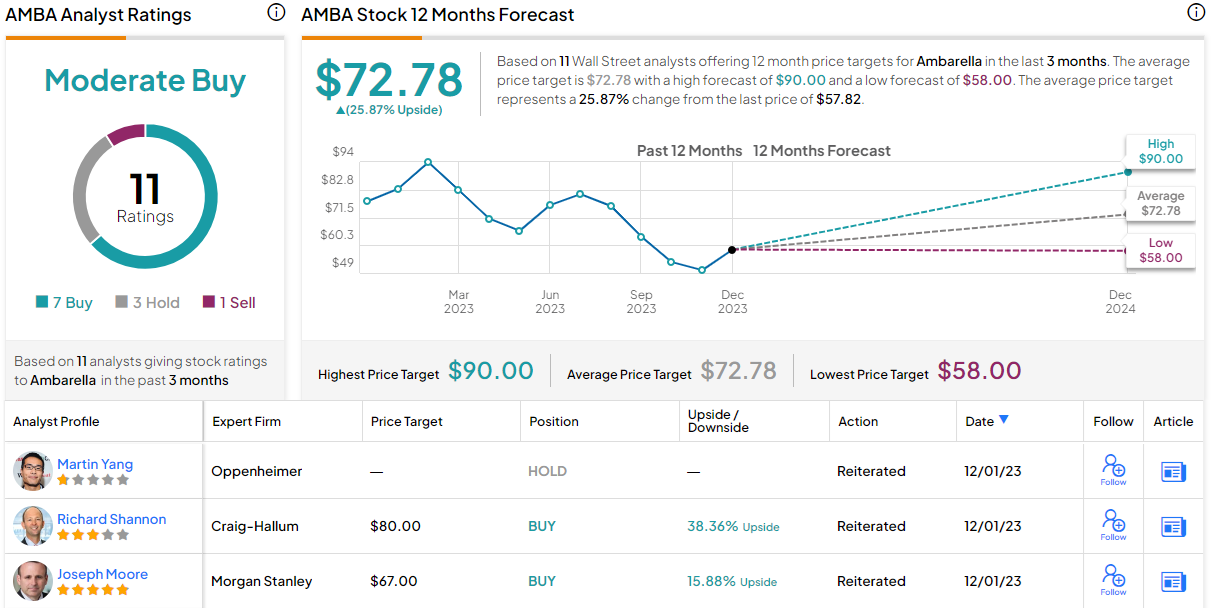

Moore rates these shares as Overweight (a Buy), with a $67 price target to point toward a 16% one-year upside potential.

This stock holds a Moderate Buy consensus rating from the Street’s analysts, based on 11 recent reviews that include 7 Buys to 3 Holds to 1 Sell. The shares are currently trading for $57.82 and the average target price of $72.78 implies a gain of 26% on the one-year horizon. (See Ambarella’s stock forecast.)

Analog Devices, Inc. (ADI)

Last on our list today is Analog Devices, a chip company that holds a solid position in the signal processing and data conversion segment. Analog’s product portfolio includes a wide range of chipsets, used in applications as varied as motor and motion control, power monitoring, clocks and timing devices, amplifiers, switches and multiplexes, and industrial ethernet solutions – and that is only a partial list.

Analog’s strategy, avoiding specialization but opting to fill a wide range of applications for its products, has paid off. The company boasts the largest market cap on this list of Morgan Stanley picks – in excess of $91 billion – and realized some $12 billion in sales last year. From an investor perspective, this is a lucrative stock, that has returned $19 billion to shareholders over the past decade.

A significant portion of that shareholder return comes from the company’s dividend payment, which was last declared for a December 14 payment. That payment is scheduled at 86 cents per share, or $3.44 annualized. While this gives a forward yield of just 1.86%, it’s important to note that the company has a history of consistent dividend payments and boasts of 19 straight years of dividend growth.

In its last quarterly report, covering fiscal Q423 (October quarter), Analog reported a top line revenue total of $2.7 billion; this represented a 16.3% y/y drop but was in-line with analyst expectations. The bottom line, reported as a non-GAAP EPS of $2.01 per share, was a penny below the forecast. The company had an operating cash flow of $4.8 billion, a free cash flow of $3.6 billion, and returned $4.6 billion to shareholders during the fiscal fourth quarter.

In his coverage for MS, top analyst Moore points out that ADI shares are a sound choice for investors looking to pick up a resilient stock with a history of outperforming downcycles. He writes, “ADI has outperformed peers in the past 3 downcycles, as gross margin has stayed resilient through cycle, and we expect the company to exhibit gross margin resilience through this current downcycle. The company has relatively higher ASP products which should limit direct competition with emerging Chinese capacity. Their latest earnings gave us further confidence that this current downturn should bottom in Q2 2024: the company has seen sequential improvement in bookings and pointed towards stabilization, cancellations are down meaningfully for the first time in close to a year, and inventory digestion accelerated at their largest customer.”’

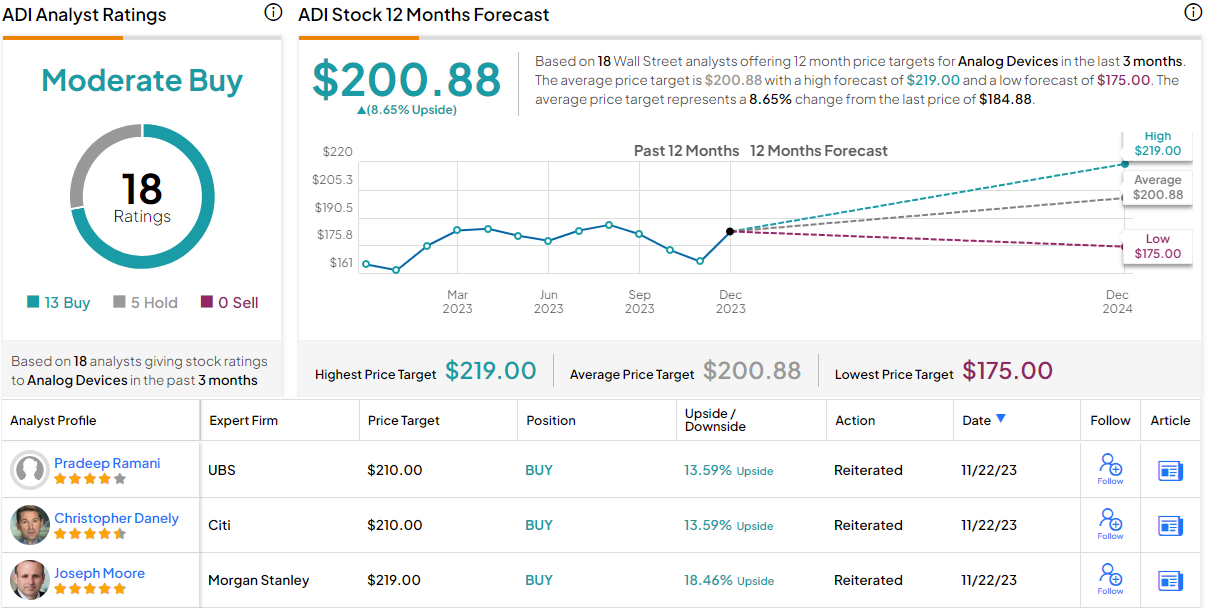

Moore goes on to put an Overweight (Buy) rating here, along with a $219 price target to imply an 18% gain in the next 12 months.

Zooming out a bit, we find that ADI gets a Moderate Buy rating from the Street’s consensus, a view based on 18 calls – 13 to Buy and 5 to Hold. ADI shares are priced at $184.88 and their $200.88 average target price indicates room for a 8.5% one-year upside potential. (See Analog Device’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.