High conviction refers to the stocks that an investor’s portfolio is overweight on.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Morgan Stanley (MS) analyst Michelle Weaver recently released a note with her top overweight picks. I selected three stocks from her list of 45 that I’m also bullish on.

Suncor Energy

Suncor (SU) stock has been in blistering form for most of the year. The integrated energy company has benefitted from rising oil prices, which has allowed it to maximize its profits on its oil sands projects situated in Canada.

The company posted fourth-quarter earnings of 89 cents per share amid robust production growth. The catalyst for Suncor was its utilization of Fort Hills, which had been under maintenance for most of 2021.

Additionally, it’s anticipated that Fort Hills will run at 90% capacity for the remainder of 2022, while Buzzard phase 2 is anticipated to produce 12 thousand barrels per day later this year.

Investors may be worried whether Suncor’s recent results can be retained, given the current abnormal energy prices. However, there shouldn’t be any concern as oil prices are still well above the company’s breakeven price of roughly $35.

Furthermore, Suncor’s stock is undervalued on a normalized forward basis as its forward price-to-earnings ratio is trading at a 56.15% discount. Additionally, Suncor stock is 38.67% undervalued relative to its forward price-to-cash flow, suggesting that the stock exhibits good intrinsic value.

Lastly, momentum needs to be kept in mind. Mark Carhart discovered in 2014 that momentum explains much of a stock’s returns, and that a high-performing stock could sustain its performance even after being overvalued. Suncor is trading above its 10-, 50-, 100-, and 200-day moving averages, indicating that it’s on a solid momentum run.

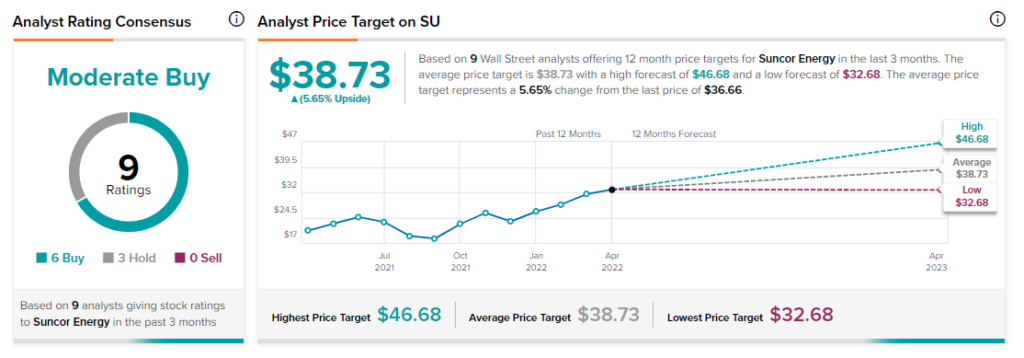

Turning to Wall Street, Suncor earns a Moderate Buy consensus rating based on six Buys and three Holds assigned in the past three months. The average Suncor Energy price target of $38.73 implies 5.6% upside potential.

Apple

Apple (AAPL) stock has lost more than 10% of its market value since the turn of the year, which is astonishing considering how well the stock is aligned with the stock market’s climate.

First off, the contractionary economic circumstances and a more than 70% year-to-date increase in the volatility index means that investors would naturally seek high-quality stocks with solid balance sheets and return metrics.

Apple provides just what’s currently required with a return on equity of 1.49x, and a return on total capital of 38.13%. Furthermore, Apple holds a robust balance sheet with an Altman z-score of 7.74x, and gross margins worth 43.32%, suggesting that economies of scale are part of the company’s furniture.

The company’s gross margins could be much more important than investors think, especially given recent supply-chain shortages.

According to Morgan Stanley analyst Katy Huberty: “The decline in D&A [Depreciation and Amortization] as a percentage of revenue has led to an average of 125 bps of gross margin tailwinds over the past 4 quarters, which we believe is structural in nature given Apple’s efforts to accelerate the in-sourcing of key components such as processors, sensors, displays, batteries, and cameras.”

If Apple can capitalize rather than expense its intangible assets and leverage its sourcing capabilities, it might beat its near-term earnings estimates.

Lastly, Apple stock’s earnings-per-share growth is still underpriced by the market as its PEG ratio is trading at a 1.45x discount relative to its benchmark, suggesting that Apple stock could find some momentum soon.

Turning to Wall Street, Apple earns a Strong Buy consensus rating based on 21 Buys and five Holds assigned in the past three months. The average Apple price target of $191.04 implies 17.9% upside potential.

SBA Communications

Real Estate is a great way to hedge against inflation, and SBA Communications (SBAC) exposure to communications site leasing in South Africa and South America.

The REIT space is lucrative at the moment as inflation could stick around for a while longer, meaning that rental income and property value appreciation could rise in tandem.

Furthermore, REITs such as SBA Communications aren’t fully priced in by the market, making this an excellent option to consider.

According to Weaver’s notes: “We favor the fundamentals of the tower model – long term contracts, operating leverage, rate escalators, low capital expenditures, high margins, strong credit tenants, and high barriers to entry.”

SBA recently beat its fourth-quarter adjusted funds from operations estimate by 62 cents per share. Additionally, SBA managed to power through the quarter’s revenue target with a $5.49 million revenue beat.

Another aspect that could favor SBA stock is that its operations are stationed in emerging markets. However, its headquarters is domiciled in the United States, allowing it to take advantage of the appreciating dollar. The dollar spot index has increased by approximately 13% in the past year, subsequently proliferating SBA’s reported earnings.

Turning to Wall Street, SBA Communications earns a Moderate Buy consensus rating based on 10 Buys, three Holds, and one Sell assigned in the past three months. The average SAB Communications price target of $384.93 implies 10.3% upside potential.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure