The first half of 2023 is well behind us now, and the second quarter earnings are getting into full swing. Currently, all eyes are on two giants of the tech world, Microsoft and Alphabet, which are preparing to release their Q2 numbers today. Both stocks have surged this year, gaining traction due to their powerful combinations of product quality, market dominance, and strong presence in the burgeoning AI segment.

AI, artificial intelligence, has been grabbing headlines in recent months as it integrates into a wide range of applications and technologies. Both Microsoft and Alphabet are heavily invested in AI, embracing the technology wholeheartedly. The AI industry is rapidly emerging into the limelight, promising rapidly expanding opportunities for investors.

This is not a zero-sum game; as AI expands, so does the pie, and there will be room enough for many players. It’s still a competitive world, though, and Microsoft and Alphabet are going head-to-head. The companies are offering varying modes of exposure to AI for investors to consider – more on that below – and the comparison and contrast will make an interesting intro to AI stocks.

Against this backdrop, we’ve pulled up the recent details on both Microsoft and Alphabet from the TipRanks database. Taken with the last quarter’s results and the preview for the upcoming earnings release, the comparison should shed some light on both of these Strong Buy tech leaders – and on which one will make the better pick ahead of the print.

Microsoft Corporation (MSFT)

First up is Microsoft, one of the world’s best-known brand names. Throughout its history, this company has defined personal computing, brought us the Windows operating system, and grown to be the world’s second-largest publicly traded company, valued at more than $2.55 trillion. In recent years, Microsoft has been a major booster of AI and invested $13 billion into OpenAI, which made waves in November when it released the AI-powered chatbot, ChatGPT.

That release shook the computing world. ChatGPT interacts with users in natural language, finding answers to questions by scouring the internet and using AI to filter the information. Microsoft’s partnership with OpenAI gives it access to ChatGPT as the power behind its Bing search engine, allowing Bing users to ask natural language search questions and receive answers the same way.

In addition to its uses for ChatGPT and online search, Microsoft is working with AI in a range of other fields and products, including its Office product suite, the Edge web browser, and its largest operating segment, the Azure business cloud infrastructure platform.

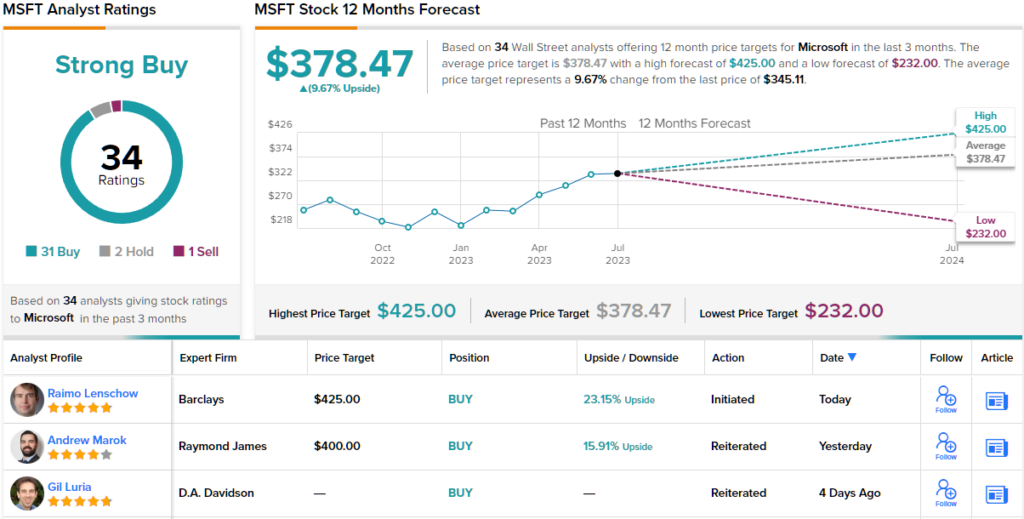

Microsoft will release its next quarterly results, for Q4 of fiscal year 2023, today – but its last quarterly release beat expectations by a wide margin. The company reported $52.9 billion at the top line, beating the forecast by $1.83 billion and growing 7% year-over-year. The high revenues supported a bottom line, non-GAAP, EPS of $2.45, a figure that came in 22 cents higher than the estimates. Shares in MSFT jumped more than 7% immediately after the release and are up 25% in the months since. Year-to-date, Microsoft’s stock has gained more than 44%.

Looking ahead, the Street expects Microsoft to report $55.5 billion in revenues for Q4 and an EPS of $2.55.

The giant tech firms pick up plenty of attention from professional analysts, and MSFT has caught the attention of Andrew Marok from Raymond James. Marok sees AI as the chief source of support for the stock and writes about the shares, “Sentiment has been definitively positive on Microsoft with AI dominating conversations around tech, and MSFT enjoying an enviable position at the vanguard of the new technology. Our conversations with investors suggest two main figures that they hope to see continue the stock’s run; no more than a modest deceleration in Azure growth with encouraging commentary for FY24, and quantification of AI tailwinds for FY24 and beyond. Our checks suggest that the first seems likely, while the scale of the conversation around AI means that MSFT will likely not be able to avoid the latter. We continue to see MSFT as best-positioned to capitalize on the long-term tailwinds that AI should bring to the tech space.”

Quantifying his stance, Marok rates Microsoft’s stock as Outperform (Buy), and he sets a $400 price target that suggests ~16% upside for the next 12 months. (To watch Marok’s track record, click here)

On the Street generally, Microsoft gets a Strong Buy rating from the analysts’ consensus, based on 34 recent analyst reviews, which include 31 Buys, 2 Holds, and 1 Sell. The shares are currently trading for $345.06, and the $378.47 average price target implies a one-year gain of ~10%. (See Microsoft’s stock forecast)

Alphabet, Inc. (GOOGL)

Next up is Alphabet, the parent company of Google. Like Microsoft, this is a giant of tech; Google has an absolutely dominant position in the online search space – although AI-powered search engines may be gearing up to challenge Google’s dominance. Google is also the web’s major player in digital advertising, making it a must-have for online marketers.

In addition to Google, Alphabet has its hands in plenty of other applications through its subsidiaries’ operations. Alphabet’s other ventures in the tech world include DeepMind, the AI research lab; Wing, a freight delivery service based on drones; and Waymo, an autonomous vehicle enterprise. One of the biggest names in Alphabet’s subsidiary list is YouTube, which has become one of the most used search engines outside of Google.

While the connection of AI to these applications may be obvious, it’s the potential impact on other areas that should grab the attention of investors. Alphabet, through Google, has been actively working in the AI ecosystem for decades now, using machine learning to fine-tune its search algorithms. However, with AI emerging into the forefront, we are likely to witness new tools and innovations from Alphabet. The company as already introduced Bard, an AI-powered chatbot that will compete directly with ChatGPT.

It looks, then, like the race is on for the lead in AI-powered natural language search responses. It’s an intriguing vision, and it provides strong support for Alphabet’s earnings outlook. We must wait until this evening to see what the company reports for 2Q23; for now, we can look at the forecast, which expects the company to show more than $72.7 billion in revenues and earnings of $1.34 per share.

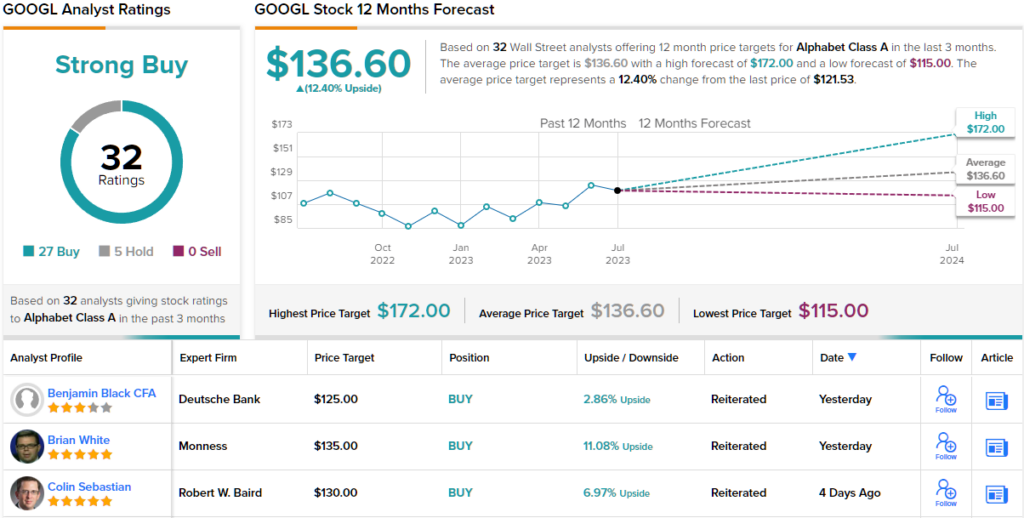

Casting our gaze backwards, it’s clear that Alphabet has already exceeded expectations with its 1Q23 numbers. The company’s revenue in the first quarter reached $69.7 billion, a 2.9% year-over-year growth, and exceeded estimates by $981.6 million. The Q1 EPS, at $1.17 per share, was 10 cents better than expected. The company’s cash assets were listed at $25.9 billion at the end of Q1, up $4.1 billion since the end of 4Q22.

Alphabet’s strong position caught the attention of Stephen Ju, a 5-star analyst from Credit Suisse. Ju is impressed by the company’s size and its ability to monetize its subsidiaries.

“As we and the Street move to value GOOGL shares on 2024 estimates, we acknowledge that macro backdrop questions remain. Given the distortion to the percentage growth rates stemming from the pandemic, we continue to run our projections based on dollars of revenue growth, with the implicit assumption being that its history of ad product development and innovation will continue to drive similar results. Our analysis of FXN growth rates over the last several years suggests that Google should add a range of $18b-$19b in revenue dollars for Search and YouTube as the head and tailwinds from macro, consumer behavior, and Apple’s privacy changes normalize,” Ju opined.

“And as we conservatively assume ongoing headwinds in 2024 and normalization in 2025, the takeaway here for GOOGL shares is that even as we leave upside potential from improving monetization potential for YouTube, Maps, and other non-Search surfaces off the table, we arrive at a positive investment conclusion,” the analyst added.

In Ju’s opinion, GOOGL shares get an Outperform (i.e. Buy) rating, and his price target, now at $150, implies a 12-month upside of 23%. (To watch Ju’s track record, click here)

Overall, Alphabet has 32 recent analyst reviews on file, breaking down 27 to 5 in favor of Buys over Holds to give the stock its Strong Buy consensus rating. The shares are priced at $121.53 and the $136.60 average price target suggests it will gain ~12% going forward into next year. (See Alphabet’s stock forecast)

The Winner Is…

Microsoft and Alphabet, both receiving a ‘Strong Buy’ rating from analysts, are compelling investment choices. However, among them, GOOGL emerges as the more alluring option for investors. With a slightly higher upside potential and a remarkable Smart Score of 10, surpassing Microsoft’s 7, Alphabet stands out as the superior choice.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.