MercadoLibre (NASDAQ:MELI) stock has surged 77% year-to-date, leveraging its status as the “Amazon of Latin America” to tap into the region’s untapped market potential. Despite my bullish stance on MELI stock since early 2022, the recent prolonged rally raises concerns about potential valuation headwinds. Although sustained growth is anticipated, the current price levels suggest overvaluation, signaling caution for prospective investors. Thus, I have now switched my stance on MELI stock to neutral.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Meli is at the Forefront of Latin America’s E-commerce Growth

Emerging at the forefront of Latin America’s e-commerce and online marketplace, MercadoLibre enjoys several advantages. Notably, the company is navigating through an expansive growth terrain within an untapped market. Remember the days of Amazon (NASDAQ:AMZN) consistently growing by 30% over the past decade? Well, that pretty much mirrors what MercadoLibre is experiencing today.

With a population surpassing 670 million and no contender developing an e-commerce, logistics, and fintech nexus as all-encompassing as MercadoLibre’s, the company is strategically poised to continue its reign and perpetuate mighty growth for the foreseeable future. To offer some perspective, the company boasts impressive five and 10-year revenue compound annual growth rates (CAGRs) of 57.4% and 40.5%, respectively. Yes, you read that right; MercadoLibre’s growth has even kicked into a higher gear in recent years.

One might attribute this phenomenon to the pandemic-induced surge in e-commerce and fintech adoption, but that only scratches the surface. This is underscored by the fact that, even with the pandemic firmly in the rearview mirror, MercadoLibre’s top line maintains its upward trajectory, displaying no indications of deceleration. In its latest Q3-2023 results, MercadoLibre escalated its gross merchandise value (GMV) by an impressive 59% on an FX-neutral basis, clocking in at $11.4 billion.

The items peddled on its platform totaled a whopping 357 million, marking a 26% upswing compared to the previous year and culminating in the company attaining record quarterly revenues of $3.8 billion. This not only signifies a remarkable 69% year-over-year increase on an FX-neutral basis, but it also indicates an acceleration from last year’s (Q3-2022) revenue growth of 61% and the preceding quarter’s growth of 57%. Furthermore, it indicates an acceleration both from its five and 10-year historical averages.

It’s also worth noting that MercadoLibre’s fantastic revenue growth is being powered by the company’s monstrous growth within its fintech segment, which has been capitalizing on Latin America’s unbanked population. Total Payment Volumes (TPV) processed within MercadoLibre’s ecosystem totaled $47.3 billion in Q3, marking a staggering year-over-year increase of 121% on an FX-neutral basis.

Economies of Scale Fueling Margin Expansion

MercadoLibre’s remarkable expansion has not only driven significant revenue growth but has also propelled a robust upward trajectory in profit margins. In a fashion reminiscent of Amazon’s early days, where the retail industry’s slim margins collided with substantial reinvestment, MercadoLibre initially operated with ultra-thin margins.

For context, MercadoLibre’s EBITDA and net income margins back in Fiscal Year 2018 were -1.7% and -2.5%, respectively. However, its LTM (Last Twelve Months) EBITDA and net income margins now stand at 18.5% and 7.5%, respectively, with scale favoring improving unit economics. As a result, MercadoLibre’s LTM net income has grown at a CAGR of 103.6% over the past five years – essentially doubling every year.

MELI’s Valuation Has Reached Worrisome Levels

Undoubtedly, MercadoLibre has displayed remarkable revenue and earnings growth, a trend that has seamlessly translated into an impressive surge in its stock performance. Previously, my bullish stance on the stock stemmed from this extraordinary potential embedded in the company’s vigorous growth trend. Today, however, I find myself adopting a more cautious outlook. Specifically, I believe that the stock’s explosive rally has resulted in MELI trading at a rather worrisome valuation.

Based on the company’s 9M-2023 results and ongoing momentum, Wall Street expects that the company will achieve an EPS of $22.67 in Fiscal Year 2023. This implies shares a hefty forward P/E of 70.5.

Nevertheless, the market seems willing to pay such a premium due to MercadoLibre’s sensational earnings growth. The $22.67 estimate itself equates to a year-over-year growth of nearly 138%. Still, it’s crucial to recognize that this valuation prices in a sustained acceleration in growth over the coming years.

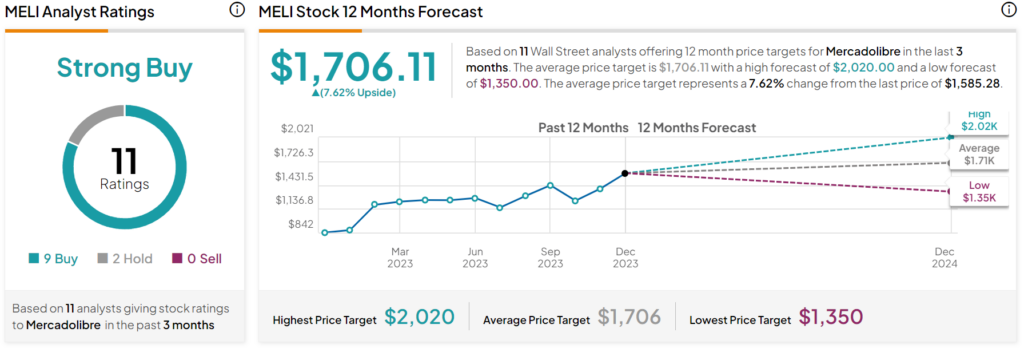

In fact, Wall Street analysts’ average MELI price target of $1,706.11 implies an upside potential of only 7.6%, as per the image below. This essentially means that the current price already reflects the company’s growth potential.

Consequently, there is minimal margin of safety for existing shareholders. Should the company’s earnings maintain their pattern of doubling annually in the medium term, as observed in the past five years, buying MELI stock, even at its present valuation, could be worthwhile. However, it is essential to acknowledge that any misstep or deceleration in earnings growth could leave current shareholders vulnerable, exposing them to significant downside risk.

Takeaway: MELI’s P/E Ratio Comes with Bold Expectations

MercadoLibre’s meteoric rise in the Latin American market, fueled by robust growth in e-commerce and fintech, has been undeniably impressive. However, the recent surge in stock prices raises concerns about potential overvaluation. While the company continues to demonstrate remarkable revenue and earnings growth, investors should exercise caution, as the current P/E ratio comes with bold expectations. The market’s optimism hinges on sustained acceleration, but this leaves a minimal margin of safety for shareholders. Consequently, my stance on MELI stock has shifted to neutral, urging caution to prospective investors.