Let’s talk about inflation. The big news on that front was the slow-down in the rate at which prices were accelerating, from 9.1% annualized in June to 8.5% in July. While still running hot, it was definitely a move in the right direction, and some market watchers have been openly speculating that it portend further reductions in the rate of price increases going forward.

That’s an important point, as high inflation has prompted the Federal Reserve to increase interest rates at the highest pace in decades. While this is a central bank’s key move against inflation, it also increases the risk of recession.

Covering the overall situation, JPMorgan strategist Marko Kolanovic writes: “We maintain that inflation will resolve on its own as distortions fade and that the Fed has over-reacted with 75 basis point hike[s]. We will likely see a Fed pivot, which is positive for cyclical assets…”

Kolanovic believes there will be no global recession – and he is confident enough to posit a 4,800 target level for S&P 500 by year’s end – a 15% gain from current levels.

Turning Kolanovic’s outlook into tangible recommendations, JPM analysts are pounding the table on two stocks, with these pros seeing double-digit upside potential in store. We ran the two through TipRanks database to see what other Wall Street’s analysts have to say about them.

Westlake Corporation (WLK)

We will start with Westlake, one of the world’s major chemicals companies, with business and production facilities located across North America, Europe, and East Asia. The company’s products are olefins and vinyls, and Westlake supplies products, like plastic wraps, that impact our everyday lives. Westlake is also an important supplier of medical-grade plastics and commonly used chemicals such as chlorine. The company’s output reaches approximately 40 billion pounds of product annually.

Westlake’s product lines are full essential materials, and the company’s revenues and earnings have been climbing steadily for the past several quarters. In 2Q22, Westlake’s revenue hit $448 million, up 39% year-over-year. Earnings, however, fell y/y, from $25.1 million to $16.4 million.

The company’s cash flows were also down, although still sound at $120.9 million in quarterly cash from operations and $19.6 million quarterly distributable cash flow. The cash flow supported Westlake’s decision to increase the share repurchase authorization by $500 million, and to bump up the common share dividend payment by 20%, to 36 cents per share.

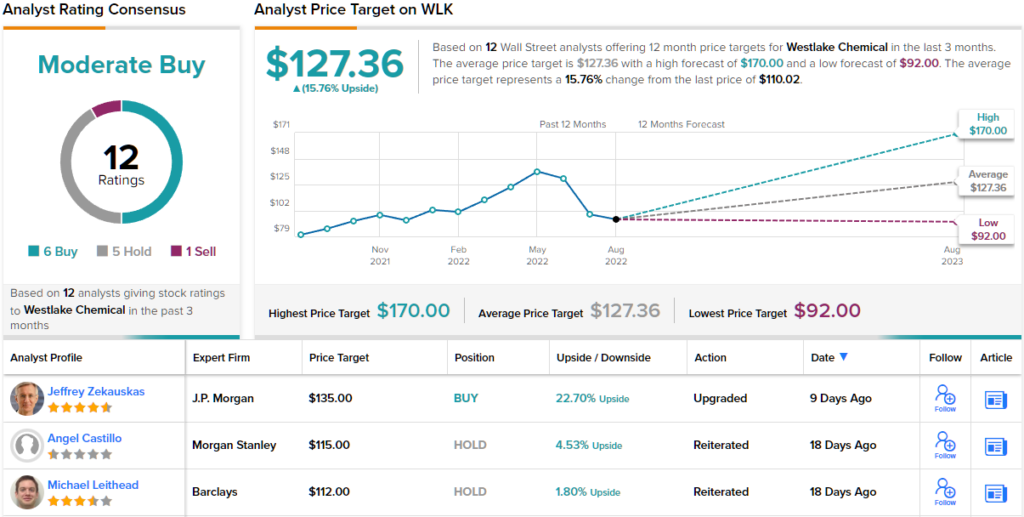

In his coverage of WLK for JPMorgan, 5-star analyst Jeffrey Zekauskas compares Westlake to its competitors and sees it in a favorable position.

“We see no reason why the gap between Westlake, on the one hand, and Olin and Dow, on the other, should not close to a degree. Dow offers more than a 5% dividend yield, and Olin is likely to repurchase about 20% of its outstanding shares in 2022, which differentiate the two companies from Westlake. All three companies have very strong balance sheets, and Westlake has an estimated 2023 free cash flow yield of 17%,” Zekauskas explained.

To this end, Westlake gives WLK an Overweight (i.e. Buy) rating to go along with this bullish outlook, and quantifies it with a $135 price target to indicate potential for 22% upside in the year head. (To watch Zekauskas’ track record, click here)

The JPMorgan view represents the bulls on Westlake, but Street is clearly split on this stock. The 12 recent analyst reviews on record break down to 6 Buys, 5 Holds, and 1 Sell – for a consensus rating of Moderate Buy. The shares are priced at $110.02, and their price target, averaging $127.36, implies an upside of 16% on the one-year time frame. (See WLK stock forecast on TipRanks)

ZTO Express (ZTO)

One thing that the digital economy has made clear is that deliver – and especially, express delivery – is still a vital service. In a way, delivery companies have helped to enable the digital economy, by providing the connecting link between online retail and real-world customers. ZTO Express lives in that niche, where it holds a 20%-plus market share in the Chinese express delivery market, and is described as a ‘key enabler’ of China’s e-commerce sector.

As befits a leading firm in a growing market with a large customer base – China has some 800 million connected internet users – ZTO has seen steady year-over-year gains in revenues for the past several years. In the most recent quarter, 2Q22, the company’s top line of $1.29 billion was up some 18% from the year-ago quarter. Diluted net earnings, at 33 cents per American depositary share, were up 42% y/y.

These solid financial numbers were supported by sound business fundamentals. The company had over 30,900 pickup and deliveries as of June 30 this year, and Q2 total parcel volume, at 6.2 million, was up 7.5% from 2Q21.

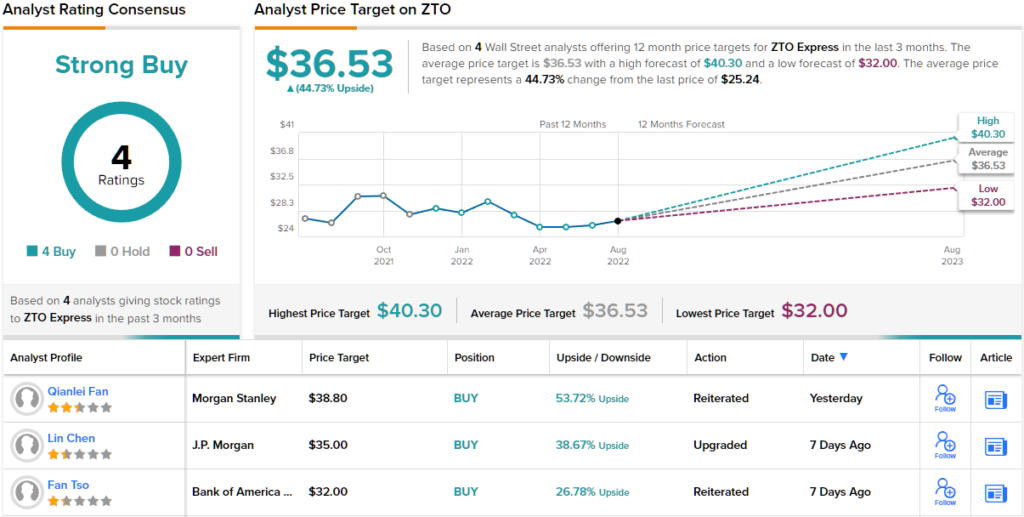

Analyst Lin Chen, covering the stock for JPMorgan, gives ZTO shares an Overweight (i.e. Buy) rating, along with a 12-month price target of $35 that implies an upside of ~39%. (To watch Chen’s track record, click here)

Supporting this outlook, Chen says, “We believe ZTO’s more established logistics infrastructure will enable market share gains amid industry-wide service disruption caused by lockdowns and logistics constraints, as evidenced by ZTO’s strongest quarterly market share gain (2ppt) since 4Q19…”

The unanimous Strong Buy consensus rating on ZTO shows that Wall Street has definitely aligned with the bulls here – all four of the recent analyst reviews on the shares are positive. The stock is selling for $25.24, and it has an average price target of $36.53 for ~45% upside potential in the coming year. (See ZTO stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.