The large U.S. banks, including JPMorgan Chase (NYSE:JPM), Wells Fargo (NYSE:WFC), and Citigroup (NYSE:C), will announce their second quarter financial results on Friday, July 14, 2023. While a higher interest rate environment could continue to drive NII (net interest income), the expected slowdown in loan growth, higher deposit costs, and continued weakness in investment banking income could put earnings under pressure.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Key Trends to Look Out For in Q2

These large U.S. banks will likely benefit from higher average rates and improvements in loan balances. However, the loan growth rate could slow due to higher interest rates. Wedbush analyst David Chiaverini believes that “peak loan growth in the current cycle is well behind us.” In a note to investors dated June 26, the analyst said he expects loan growth to slow in the second quarter due to lower customer demand and tight underwriting standards.

Echoing similar sentiments, Goldman Sachs analyst Richard Ramsden expects industry loan growth to trend down. However, the analyst highlighted that “consumer lending is heavily concentrated in the large banks,” and he sees “less stress in consumer lending.”

While both analysts expect credit quality to stay strong, the ongoing macro uncertainty could lead to a reserve buildup (an amount kept aside by banks to absorb losses on loans).

Furthermore, the higher average rate and weak capital market activity could continue to hurt mortgage banking income and pressure investment banking fees.

Against this backdrop, let’s understand what Wall Street analysts recommend about these large U.S. banks ahead of their Q2 print.

What is the 12-Month Price Target for JPM Stock?

JPMorgan’s top line is likely to benefit from higher NII, led by an increase in loan balances and higher average rates. However, a higher deposit rate could remain a drag. JPM’s Investment Banking revenue could continue to decline, led by lower debt underwriting fees amid economic uncertainty.

Wall Street analysts expect JPMorgan to report revenues of $39.27 billion in Q2, which reflects an improvement from the previous quarter’s revenue of $38.3 billion. At the same time, analysts expect JPM to post earnings of $3.96 per share in Q2, up from $2.76 in the prior-year quarter. However, EPS is likely to decrease slightly on a quarter-over-quarter basis, reflecting a lower spread and an expected increase in reserve build-up for credit losses.

Nonetheless, analysts remain bullish about JPM stock ahead of the Q2 print. Steven Chubak of Wolfe Research upgraded JPM stock to Buy on July 7. The analyst sees JPM’s NII outlook as “conservative” and sees accretion from the First Republic deal. Chubak sees JPM stock’s premium valuation as warranted.

Along with Chubak, Ramsden is also constructive on JPM stock and sees less risk of NII guidance downgrades from an increase in deposit costs. Also, the analyst expects JPM could benefit from the First Republic deal.

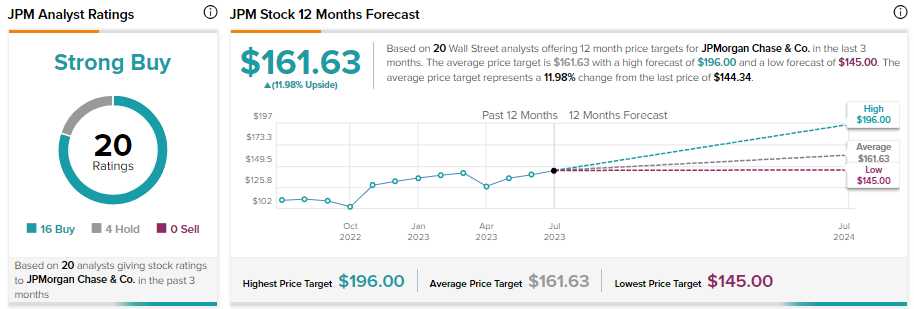

JPM stock has 16 Buy and four Hold recommendations, reflecting a Strong Buy consensus rating on TipRanks. These analysts’ average 12-month price target of $161.63 implies 11.98% upside potential from the current levels.

Is Wells Fargo Stock Predicted to Go Up?

Wells Fargo’s NII is expected to grow in Q2 due to higher interest rates and an increase in loan balances. However, lower deposit balances could hurt the NII’s growth rate. Also, mortgage banking income could continue to witness challenges reflecting lower originations. Meanwhile, investment banking fees could stay weak on account of a decline in market activity.

Wall Street expects Wells Fargo to post revenue of $20.11 billion in Q2, which reflects an improvement from the prior year. However, analysts’ top-line forecast indicates a slight decrease in revenues on a quarter-over-quarter basis. Analysts expect WFC to post earnings of $1.18 per share in Q2, reflecting a significant improvement from the prior year. However, EPS is projected to decline on a quarter-over-quarter basis.

Raymond James analyst David Long raised WFC’s price target to $51 from $48 on July 3. The analyst recommends a Buy on WFC stock ahead of Q2 earnings as he expects it to benefit from expense rationalization, opportunistic share buybacks, and solid credit trends.

WFC stock has 10 Buy, five Hold, and one Sell recommendations ahead of Q2 print, translating into a Moderate Buy consensus rating. Further, the average price target of $47.04 implies 9.98% upside potential.

Is Citigroup a Buy, Sell, or Hold?

Citigroup’s top line is expected to benefit from growth in net interest income. However, the decline in non-interest revenues could remain a drag. A higher NII and a decrease in average diluted shares outstanding are likely to support its EPS in Q2.

Analysts expect Citigroup to post revenues of $19.48 billion in Q2, lower than Q1 revenues of $21.45 billion. Wall Street expects Citigroup to post earnings of $1.34 in Q2, reflecting a significant decline on a year-over-year and sequential basis due to higher expenses.

Wells Fargo analyst Mike Mayo reduced his price target on Citigroup stock on June 28. The analyst expects the bank to benefit from higher rates. However, increased pressure on fee income could remain a drag.

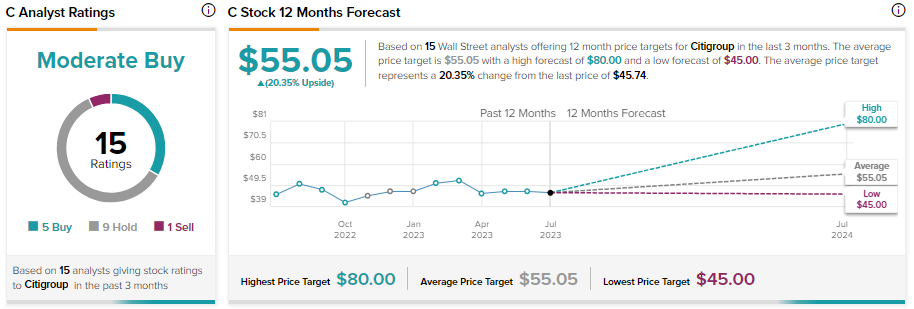

Overall, Citigroup stock sports a Moderate Buy consensus rating on TipRanks, based on five Buy, nine Hold, and one Sell recommendations. Analysts’ average 12-month price target of $55.05 implies 20.35% upside potential.

Bottom Line

The banking sector could face challenges from the deposit drain, the slowdown in loan growth, and lower fee income. However, these large banks could continue to generate higher net interest income, led by higher rates and a slight improvement in loan balances. Also, their diversified revenue base and strong balance sheet position them well to navigate the macro challenges.

Among JPM, WFC, and C, JPMorgan stock, with a Strong Buy consensus rating, remains a top pick (based on analysts’ recommendations) ahead of the Q2 print.