Johnson & Johnson (NYSE: JNJ) has received some negative press lately, but will time heal the reputational wounds? I am bullish on Johnson & Johnson stock as the company’s financial guidance indicates an all-weather business that can survive its temporary challenges.

Headquartered in New Jersey, Johnson & Johnson provides healthcare products across its Consumer, Pharmaceutical, and Medical Devices segments. The company’s pharmaceutical products run the gamut from immunology, infectious diseases, and vaccines to neuroscience, oncology, cardiovascular, and more.

Yet, everybody and his uncle seems to want to focus on Johnson & Johnson’s baby powder, not its high-conviction pharmaceutical products. That’s fine, as the market’s fear has only made JNJ stock cheaper, and value seekers should thank their lucky stars for the errors of overly-anxious financial traders.

Johnson & Johnson Lawsuits: Don’t Be Swayed by Talc Talk

I can’t ignore the elephant in the room, so let’s talk about the ongoing litigation against Johnson & Johnson concerning the company’s baby powder and related products. This story concerns roughly 40,000 lawsuits allegedly linking Johnson & Johnson’s talc products to cancer.

Reportedly, a Philadelphia federal appeals court, the Third U.S. Circuit Court of Appeals, turned down Johnson & Johnson’s request to use chapter 11 bankruptcy protection to halt those talc lawsuits. Thus, it appears that the company’s unusual “Texas two-step” legal strategy won’t stop Johnson & Johnson’s legal woes.

Johnson & Johnson has already removed its talc-based baby powder from the U.S. market. Besides, this will all probably resolve through financial settlements. JPMorgan (NYSE: JPM) analyst Chris Schott, according to the Wall Street Journal, “estimates J&J’s liabilities for talc could end up in the range of $8 billion to $10 billion.” I fully expect Johnson & Johnson to raise its product prices in order to pay for its legal issues, and eventually, the reputational damage will abate.

JNJ Stock’s Drop Only Makes it More Attractive

JNJ stock took a 3.7% hit and landed at exactly $162 after the announcement of Johnson & Johnson’s legal setback. That’s good news for prospective investors, as the stock is now close to the bottom of its year-long range of $155.72 to $186.69.

Also, Johnson & Johnson has a P/E ratio of 25x, which indicates good value. In general, I like to see a P/E ratio below 30x, and when it’s 25x or lower, that’s even better. Furthermore, JNJ stock is an ideal holding for safety-conscious investors, as its beta is ultra-low at 0.32, which means the stock isn’t volatile.

Plus, Johnson & Johnson has paid dividends for many years, and currently, the company pays a 2.65% annual dividend yield. Johnson & Johnson’s next ex-dividend date is February 16, so consider owning some shares before that cutoff date.

JNJ’s Earnings Beat is Good, and Its Guidance is Even Better

If there’s one thing that can add more excitement to an earnings beat, it’s an optimistic outlook. For 2022’s fourth quarter, Johnson & Johnson exceeded Wall Street’s expectations, but it’s also important to know that the company anticipates strong current-year earnings growth.

In Q4 2022, Johnson & Johnson’s adjusted EPS of $2.35 beat the analyst consensus estimate of $2.24. Amazingly, Johnson & Johnson has consistently been beating quarterly EPS expectations for years.

That’s great, but it only gets better when we take a look at Johnson & Johnson’s earnings guidance. For the full year of 2023, Johnson & Johnson models adjusted EPS of $10.45 to $10.65, with a midpoint estimate of $10.55. That’s ahead of the average analyst estimate of $10.33 per share.

Clearly, Johnson & Johnson’s management isn’t too worried about the company’s financial future. Its ambitious EPS forecast for 2023 suggests that the company should be able to weather its legal problems and continue to deliver outstanding value to the customers and shareholders.

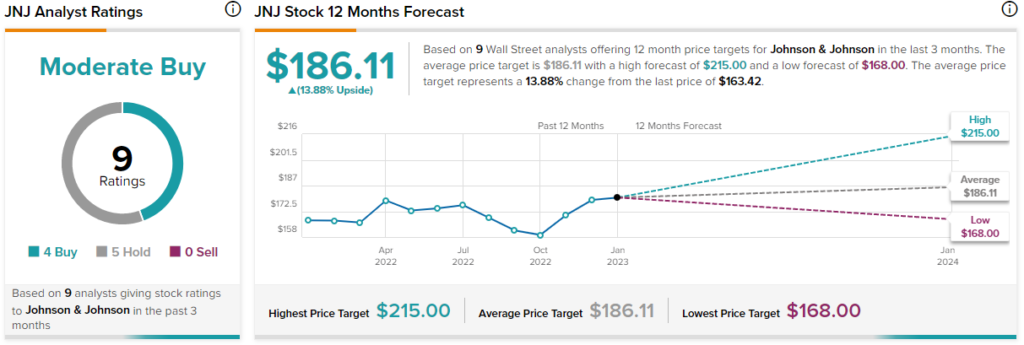

Is JNJ Stock a Buy, According to Analysts?

Turning to Wall Street, JNJ stock is a Moderate Buy based on three Buys and five Hold ratings. The average Johnson & Johnson stock price target is $185, implying 13.9% upside potential.

Conclusion: Should You Consider Johnson & Johnson Stock?

Johnson & Johnson stock is known as a defensive stock – and for good reasons. The company consistently beats Wall Street’s EPS forecasts, JNJ stock has a low beta, and it pays a healthy dividend.

So, you don’t have to let the media’s headlines dissuade you from considering JNJ stock. It’s fine to consider holding some shares for the long term, as Johnson & Johnson’s management envisions a profitable 2023 despite the perceived headline risk.