Starbucks (SBUX) has faced significant challenges recently, with its stock trading close to is 52-week low four times this year. To revitalize the company’s return to growth, the board announced the hiring of Brian Niccol, the former CEO of Chipotle (CMG), with a substantial compensation package. Following this announcement, the stock surged to new highs. As Niccol officially took the helm on September 9th, investors are contemplating whether to buy Starbucks stock now or wait for a turnaround. In my view, SBUX is a Buy, and this article will explore the reasons why.

Confident Investing Starts Here:

- Quickly and easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

Let’s delve in.

Recent Developments in Starbucks Stock

My bullish outlook on Starbucks gained new momentum in September, marking a pivotal moment for the company’s stock performance. Following Brian Niccol’s hiring, the stock entered positive territory for the year, recovering from a decline of up to 20% by the end of July; but still about 22% below its all-time highs.

A significant portion of this decline was attributed to recent earnings reports indicating a decrease in comparable store sales across various retail giants, including Starbucks. Many market participants believe this trend is due to a cautious consumer base. Notably, while companies like Target (TGT) and Home Depot (HD) reported drops in recent quarters, Walmart (WMT) saw growth, highlighting a shift in consumer spending patterns.

In its most recent quarter, Starbucks’ comparable store sales in North America dipped by 2%, with transaction counts declining even further—down 6% year-over-year when adjusted for price hikes and sales mix. Overall, Starbucks experienced a 4.2% year-over-year decline in company-wide operating income, falling to $1.52 billion, alongside a 70 basis point reduction in non-GAAP operating margin. Notably, operating margins in the International segment decreased by 340 basis points to 15.6%, a steeper decline than in North America.

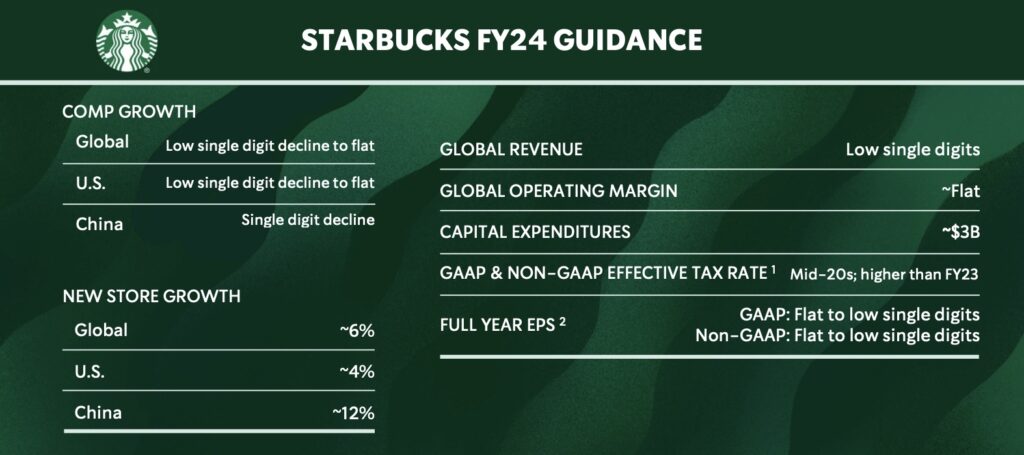

In light of these challenges, Starbucks is projecting low single-digit declines in comparable sales globally, with particularly weak performance noted in China. To address these issues, the company plans to increase its store openings, targeting a 12% growth in locations in China by the end of Fiscal year 2024.

Assessing Starbucks’ Turnaround

The concept of a “turnaround” can be subjective and does not significantly affect my bullish view on SBUX. While comparable store sales have declined, I believe this is largely due to a weaker consumer base rather than any inherent issues with the company. Despite these challenges, Starbucks continues to perform well, particularly in terms of cash generation.

Starbucks offers a dividend yield of 2.34%, which amounts to $2.55 billion in cash flow. The dividend appears sustainable, as the company generated $3.6 billion in free cash flow last year, with an average of $2.81 billion over the past five years. Assuming last year’s free cash flow remains stable, Starbucks can easily maintain this dividend.

However, given the recent poor quarterly results, the company recognized the need to address these issues and revitalize growth. As a result, Starbucks hired Brian Niccol as its new CEO. Niccol has a strong track record, having successfully led Chipotle through a major recovery following its food safety crisis. Under his leadership, Chipotle’s revenue more than doubled, rising from $4.86 billion in 2018 to $9.8 billion in 2023. Notably, the number of Chipotle locations grew from 2,048 in 2017 to over 3,400 last year. It’s important to acknowledge that Chipotle was in a rapid growth phase during that time, presenting a different set of challenges compared to Starbucks’ more mature market.

SBUX Continues to Grow Despite Challenges

Strengthening my bullish thesis on Starbucks, the company continues to grow despite current challenges. With nearly 40,000 stores globally, up 6% year-over-year, Starbucks is far from stagnant. Brian Niccol’s potential impact could mirror the growth seen at Chipotle, especially if he leverages his experience to open new locations. The company aims to add 17,000 stores by 2030, increasing its total by about 40%.

That said, recent net income figures for Starbucks reveal a pattern of stagnation, with a compound annual growth rate (CAGR) of 2.7% over the past five years. Looking ahead, analysts project earnings per share (EPS) growth ranging from $3.55 to $4.44 between Fiscal 2024 and Fiscal 2026, indicating a potential increase of 25% during this period. Revenue growth projections suggest a 15% increase over the same period from $36.5 billion to $42.2 billion. While inflation may drive costs higher, Starbucks’ planned expansion should help mitigate these impacts.

One of Starbucks’ significant strengths is its impressive return on invested capital, currently at 32.4%. This means the money they invest in the business generates substantial returns, which is crucial as they prepare to increase their store count by 40%. These strong returns, if sustained, may suggest that analyst projections could be somewhat conservative.

When we compare future earnings projections to the current price, Starbucks trades at a P/E ratio of 27.2x and a forward P/E ratio of 22x for 2026. These figures are significantly below the historical average of 29x over the past five years, making the stock appear somewhat attractively priced.

Is SBUX a Buy, According to Wall Street?

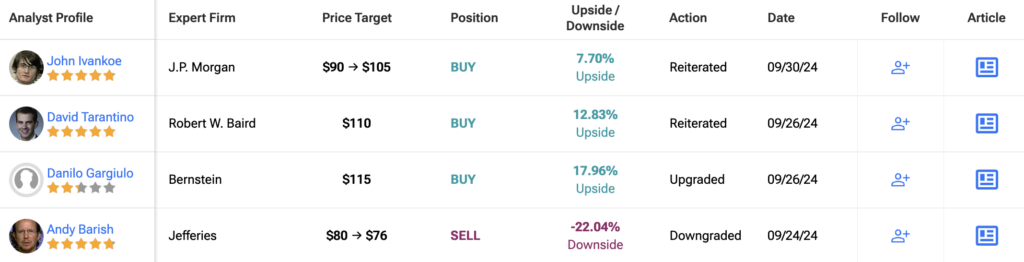

At TipRanks, the consensus among analysts on SBUX is a Moderate Buy. Of the 24 experts covering the stock, 15 have issued a Buy recommendation, seven have a Hold recommendation, and two have a Sell recommendation. The average SBUX price target is $100.75, indicating an upside potential of 3.34%.

The Bottom Line

Despite recent weak results indicated by the drop in same-store sales—an issue I believe stems more from consumer behavior than from the company’s strategy—I see Starbucks well-positioned for a recovery in its growth trajectory, particularly under the leadership of CEO Brian Niccol.

While the valuation may not be as attractive as it was a few months ago, the company’s ongoing store expansion plans and high return on investment are likely to positively impact its EPS multiple in the future. In my view, this creates a compelling long-term investment opportunity, especially given that the current valuation remains below its historical average.