Palantir (PLTR) is making headlines after posting a beat-and-raise quarter a few weeks ago on August 5. On the one hand, investors are enthusiastic about the company’s serial deal-making, but on the other hand, they are concerned about its rich valuation. Therefore, the key question is whether PLTR stock is overpriced at current levels or if it represents a valuable growth opportunity. That’s what I’ll explore in this article.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

At its core, Palantir is a pure-play data management and analytics company that serves both government customers, such as the CIA, and commercial customers, including healthcare companies, retailers, banks, and more. The company helps clients analyze, manage, and visualize large corpora of data in real time.

Additionally, Palantir offers three products: Gotham, Foundry, and Apollo. Gotham is used by government customers, while Foundry is designed for commercial clients. Apollo, meanwhile, facilitates seamless continuous integration and continuous delivery (CI/CD) across all environments.

All things considered, whether the stock is expensive or not, I remain bullish on Palantir. This is due to its strong execution in winning commercial market share, its margin expansion, and the significant potential it holds, especially considering how early it is in its growth story.

Tracing Palantir’s Backstory

Given my bullish stance on Palantir, it’s important to understand the company’s story before investing in it. This is especially true because SaaS companies can be rather complicated, and Palantir is no exception.

To start with, Palantir was founded in 2003 by Peter Thiel, Nathan Gettings, Joe Lonsdale, Stephen Cohen, and Alex Karp. Their mission was to combat terrorism through fraud recognition systems, similar to those employed by PayPal (PYPL) at the time.

By 2005, Palantir secured the CIA as its first client for intelligence services. Following this success, the company signed deals with the FBI, NSA, NYPD, and other notable customers. Expanding further, in 2016, Palantir launched Foundry for commercial use cases like managing inventories or optimizing supply chains.

Then, in 2020, Palantir introduced Apollo, which supports Gotham and Foundry by resolving dependencies, issuing updates, and handling various operational tasks.

Over the years, Palantir has grown from a small company with a niche presence in the US into a global powerhouse for data analytics and intelligence software. Today, the company operates in 150 countries, including the US and the UK, helping clients merge structured (spreadsheets) and unstructured data (images) to draw meaningful connections.

Moreover, Palantir’s platforms are now the top choice for high-profile commercial clients, and it’s also winning deals with government clients. All of this contributed to strong Q2 2024 results and an upward revision of their Fiscal 2024 outlook.

PLTR’s Numbers Are Stronger Than Ever

Transitioning to the financial side, I find that the numbers Palantir posted in Q2 2024 further strengthen my bullish outlook. Specifically, the company reported an EPS of $0.06, outperforming analysts’ estimates by $0.03. This solid performance not only underscores Palantir’s ability to exceed expectations but also reinforces my confidence in the company’s growth trajectory. Additionally, revenue was $678 million, up 27.15% year over year and ahead of market consensus by $25.7 million. Looking ahead, for the full year, management is guiding to $2.74 – $2.75 billion in revenue (+23% year over year), which I believe solidifies the company’s position in the market and justifies my optimistic stance.

Digging deeper into the revenue breakdown, total revenue was led by growth in the commercial business, which increased 33% from Q2 2023, while their US commercial business grew 55% year over year. Moreover, government revenue was up 23%, with US government revenue growing by 24% from the same period last year.

Another impressive metric is Palantir’s US commercial customer count, which grew by 83% year over year to 295. This growth is driven by new clients like Tampa General Hospital, Panasonic Energy, and several others, all of whom are benefiting from the company’s Artificial Intelligence Platform (AIP).

Palantir’s AIP is making a significant impact, helping enterprises leverage machine learning to drive down costs and deliver better products and services to clients. Whether it’s reducing the stay of a patient at Tampa General or reducing the downtime of equipment at Panasonic, Palantir’s AIP is becoming the solution of choice.

As a result, investors are taking notice, and they’re loving the favorable client testimonials and double-digit growth in both businesses. This enthusiasm explains why the stock is making headlines.

Furthermore, commercial growth is indeed a strong driver for Palantir, and management is guiding to a 47% year-over-year increase in commercial revenue for Fiscal 2024. So, what’s driving this growth? A winning strategy.

Specifically, Palantir’s bootcamp strategy is a “key go-to-market motion” for the business right now. They set up bootcamps with clients to show prototypes of their AIP, which leads to 7-figure deals and then enterprise-wide implementations. Since the launch of their Artificial Intelligence Platform in mid-2023, Palantir has completed over 1,000 bootcamps in the US.

While the commercial business is strong, that doesn’t mean the government business is weakening. In fact, their total government revenue was $371 million, of which $278 million was US government revenue. During the quarter, they won a new five-year contract worth $480 million with the US Department of Defense for scaling AI/ML capabilities. So clearly, things aren’t bleak on the government side either.

Palantir’s Profitability Streak Continues

I also like the profitability streak of Palantir. This aspect further solidifies my bullish outlook. The company recently became profitable, and Q2 2024 marked its seventh consecutive quarter of net income profitability. Notably, operating margins also improved to 16% during the quarter, up 1,400 basis points year over year. Adding to this positive momentum, Palantir ended the quarter with $4 billion in cash on the balance sheet and no debt.

Looking ahead, for the full year, management is guiding to operating income between $966 million and $974 million and adjusted free cash flow of between $800 million and $1 billion. This strong financial positioning continues to reinforce my confidence in the company’s growth potential.

In the Software-as-a-Service (SaaS) industry, there’s an important metric called the “rule of 40,” which is used to gauge the health of a SaaS business. The rule of 40 states that the sum of the revenue growth and profit margin should be at least 40%.

Impressively, Palantir’s revenue growth and profit margins have added up to well above 40% since mid-2023. If it continues to manage its costs and grow sales simultaneously, I believe it’s going to remain a healthy and thriving SaaS business.

Palantir Is a Serial Deal Maker

Building on this strong financial foundation, I’m increasingly optimistic about Palantir’s future, especially as I see how adeptly they’re winning deals. As I highlighted earlier, the half-billion-dollar contract with the US DOD is just the tip of the iceberg. The company’s track record now showcases their prowess as a serial deal maker, consistently signing deal after deal after deal.

In Q2 2024 alone, they signed 123 new commercial deals, almost double the number from the same period last year. Furthermore, they closed 96 deals of at least $1 million, with 33 of those being valued at least $5 million and 27 carrying a price tag of at least $10 million.

Is Palantir Stock Expensive?

Given Palantir’s impressive deal-making momentum, I’m optimistic about the company’s future prospects. However, it’s equally important to assess whether the stock’s current valuation is justified. While I’m bullish on Palantir’s growth potential, I’m also wary of the high valuation, especially with the stock trading at 91 times forward earnings. To address this concern, let’s explore whether Palantir is considered expensive at this level.

To put it another way, investors are currently paying 91 times the profit the company is projected to make in 2024. This represents a 292% premium compared to the sector average.

While I’m generally wary of projecting too far into the future, I’ll use this year’s earnings growth rate for the PEG calculation. Analysts expect earnings to grow by 44% this year. When factoring in this growth, investors are effectively paying 2 times per unit of growth at $32.5 per share.

In my humble opinion, this valuation is quite high, even for a growth stock. There’s considerable execution required to make the current multiple reasonable. Although the company’s post-IPO performance was less impressive, it’s showing signs of improvement.

Looking ahead, if Palantir’s sales compound at approximately 20% annually over the next 25 years, it could surpass $200 billion in revenue by the end of this forecast period. While I doubt that PLTR will maintain a 90 times earnings multiple for long, the company’s potential remains significant and worth considering.

Is Palantir a Buy, Hold or Sell?

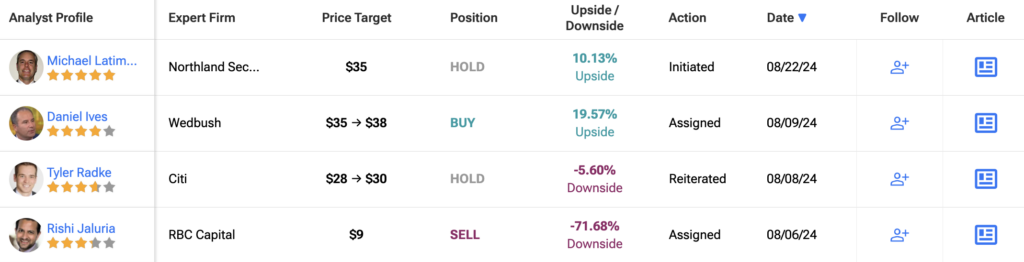

Analysts remain sidelined about PLTR stock, with a Hold consensus rating based on three Buys, five Holds and six Sells. Over the past year, PLTR has surged by more than 115%, and the average PLTR price target of $25.42 implies a downside potential of 20% from current levels.

The Bottom Line on Palantir

In conclusion, I’m cautiously optimistic about Palantir because of its strong financial results and impressive deal-making, which show great growth potential in data analytics. The company’s solid performance and increasing market share make it look promising. However, it’s important to be careful about the stock’s high valuation—trading at 91 times forward earnings. While Palantir’s achievements are impressive, investors should think about whether the current price matches the expected growth, weighing the exciting potential against the risks of a high valuation.