Alibaba Group Holding Limited (BABA), the Chinese e-commerce juggernaut, has taken a massive hit over the past two years due to pandemic-related disruptions and the Chinese government’s crackdown on the tech industry. Alibaba’s stock dropped 51% over the last 12 months, compared to a 13% decline in the S&P 500 (SPX). Alibaba stock may be headed for a significant recovery in the long run given that Chinese regulators are now taking a more measured approach. However, the company continues to avoid making any predictions for the upcoming quarters due to the uncertainty surrounding macroeconomic conditions.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The expected slowdown of the Chinese economy, geopolitical tensions, and the threat of U.S. regulators tightening their grip on Chinese stocks do not paint a promising picture for Alibaba.

Although I am bullish about the long-term prospects of the company and the stock looks attractive at these depressed prices, things are likely to get worse before they get better.

Regulatory Challenges Are Easing for BABA

Investors abandoned Alibaba for two primary reasons. First, Alibaba was charged with a record-breaking antitrust penalty by Chinese officials. The Chinese government has been cracking down on large technology companies for alleged monopolistic data security tactics and monopolistic business practices. Alibaba’s profitability was significantly impacted after it was fined $2.75 billion by China’s State Administration for Market Regulation in April 2021.

Additionally, authorities imposed new restrictions on its e-commerce business and called off the Ant Group’s much-anticipated IPO. Chinese regulators have tightened their control over businesses trying to enter foreign financial markets ever since the $35 billion IPO of the Ant Group, the fintech division of Alibaba, was suspended by the China Securities Regulatory Commission (CSRC) in November 2020.

The Ant Group was scheduled to start trading in Hong Kong. However, this was suspended after Shanghai officials said that the listing would be halted as Alibaba was unable to meet the requirements due to changes in the regulatory environment.

Many investors continue to avoid Chinese equities in general as a result of the possibility of mass delisting in the United States. Alibaba faces the possibility of delisting from U.S. exchanges even though the SEC has not yet identified it as a violator of the Holding Foreign Companies Accountable Act (HFCAA). That said, some institutional investors are already moving to Hong Kong to invest in Alibaba while dumping its American depositary receipts (ADRs). For example, BlackRock, Inc. (BLK) sold its Alibaba ADRs in the U.S. and purchased the stock in Hong Kong.

Alibaba stock has gained some ground since March after Beijing and the U.S. announced that officials are in talks to allow American regulators to undertake on-site audits of Chinese companies listed in the United States. Chinese policymakers have also paused their regulatory pressure on the tech industry in an effort to stabilize the economy, which has dramatically improved the sentiment toward Alibaba. The focus of investors, therefore, is likely to shift to corporate earnings once again.

BABA’s Recent Earnings Highlight New Challenges

Alibaba surpassed analyst estimates and posted revenue of RMB 204,052 billion ($32.18 billion) for the fourth quarter of fiscal 2022. The China Commerce segment brought in RMB 140,330 million ($22.17 billion) in revenue, an increase of 8% from the previous year. Similarly, the Local Consumer Services segment reported RMB 10,445 million ($1.64 billion) in revenue, an increase of 29%. The all-important Cloud segment brought in RMB 18,971 million ($2.99 billion) in revenue, an increase of 12% from the previous year.

For the fiscal year ending March 31, 2022, Alibaba Group’s global active consumers totaled approximately 1.31 billion. This includes over one billion Chinese consumers and 305 million international consumers, representing a quarterly net increase of approximately 24.6 million and 3.7 million customers, respectively, and an annual net increase of 113 million and 64 million customers, respectively.

The company’s global gross merchandise value (GMV) for the fiscal year reached a record RMB 8,317 billion ($1,312 billion). However, the GMV growth in January and February was flat, and the overall GMV for the quarter had a low single-digit decline. This was due to logistics and supply chain pressures, coupled with a softening of demand due to challenging macroeconomic conditions such as inflation.

Alibaba’s gross and operating margins declined significantly in the recent quarter due to severe margin pressures brought on by inflation. The Chinese economy is struggling as a result of strict lockdowns, inflation, and sluggish consumer demand. These margin pressures have already hurt the company’s free cash flow, and a continuation of this trend will not be welcome news for investors.

Alibaba reported a negative free cash flow exceeding $1 billion for the fourth quarter of fiscal 2022, which is not encouraging given that the company has always been able to generate positive free cash flow even under challenging circumstances. Macroeconomic challenges are already taking a toll on Alibaba’s earnings, and its stock price might come under pressure yet again due to the deterioration of investor sentiment toward China and Alibaba’s growth prospects.

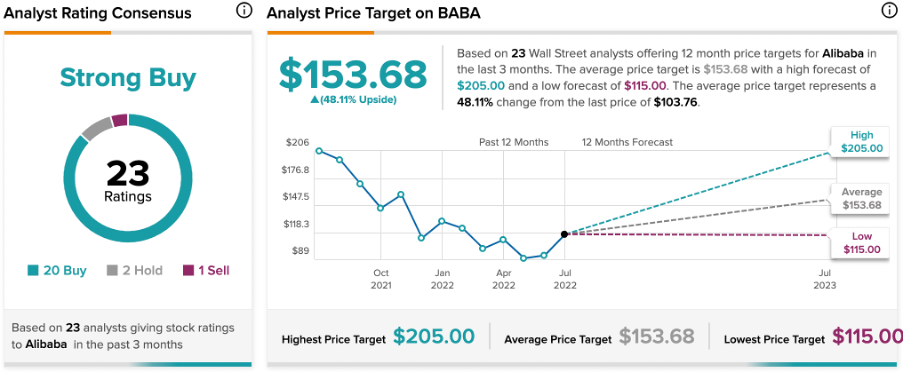

Wall Street Is Bullish about BABA

Based on the ratings of 23 Wall Street analysts, the average Alibaba price target is $153.68, which implies upside of 48% from the current market price.

Takeaway

Alibaba can finally breathe easy as regulators are taking a step back. Unfortunately, the company is now faced with macroeconomic challenges that threaten to eat into its profitability. Even on the back of a lackluster stock market performance in the last 12 months, Alibaba stock is still valued at a forward price-to-earnings (P/E) multiple of 29, suggesting investors are willing to pay a premium for expected growth. This premium, however, could quickly disappear if Alibaba fails to maintain the growth momentum in the coming quarters, which makes investing in Alibaba only suitable for investors with a long-term perspective.

Read the full Disclosure.