There are many strategies investors can use in order to get the best out of a portfolio and one involves following the moves of the insiders.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

By insiders, we mean the corporate officers, the top-level executives and Board members who are responsible for bringing company profits and sending returns to shareholders. Their roles give them valuable insights into the inner workings of their firms, and also give them early access to information that will impact share prices. So, when the insiders start pouring millions into their own stock, it’s a clear sign they believe the shares are undervalued.

Thanks to regulatory disclosures, investors can track insider buying activity, and one tool that highlights these trends is TipRanks’ Insiders’ Hot Stocks screener. We’ve used it to pinpoint three stocks seeing major insider accumulation, each of them also rated as Buys by the analyst consensus. Let’s dive in.

Builders FirstSource (BLDR)

The first stock on our list is Builders FirstSource, a major supplier of products, services, and value-added components in the US construction and building market. Builders FirstSource operates mainly as a supplier to residential builders and construction contractors, who in turn are focusing on new residential constructions, remodeling jobs, and home repairs. The housing industry in general depends on these vital construction activities to expand housing stocks and to maintain existing housing stocks in valuable condition.

Since getting started in 1998, Builders FirstSource has built up the network that allows it to live up to its name. The company operates a network of approximately 590 manufacturing and distribution locations, spread across 91 top metropolitan statistical areas in 43 states. Through this network, the company caters to enterprise customers in the building sector, offering top-quality products and supplies, backed up by expert knowledge of local markets and the general construction industry.

On the financial side, Builders FirstSource released its 1Q25 results on the first of this month, and showed a year-over-year contraction in sales along with a miss on EPS. The top line of $3.7 billion was down 5% from 1Q24, although it did beat the forecast by $40 million. The bottom line, at 84 cents per share, missed expectations by 20 cents. The company finished the quarter with approximately $1.1 billion in liquidity, a total that included $115 million in cash on hand plus $944 million available under a revolving credit facility.

Along with the earnings release, Builders FirstSource also authorized an expansion of its share repurchase program. The company had some $100 million remaining on the previous authorization; the Board has now put its approval on a total repurchase program, including that $100 million, of up to $500 million.

This stock is down by 35% over the past year, but one insider must be sensing an opportunity. Paul Levy – of the company’s Board of Directors – made two huge purchases of BLDR stock on May 8 and 9. These buys totaled 500,000 shares, and are now worth a hefty $54.2 million.

For Goldman analyst Charles Perron-Piche, BLDR represents a sound buy. The sector expert explains his reasons for optimism on this leading building materials company.

“We remain confident that Builders FirstSource can leverage organic initiatives to outperform peers despite a decelerating housing backdrop,” Perron-Piche explained said. “Our view reflects continued momentum of commercial efforts, including digital and installation services, allowing it to capture a greater share of customers’ wallets. This also comes as headwinds from home size and complexity are stabilizing through the spring, coupled with a rising commodity backdrop, suggesting a greater lift to sales relative to starts through the balance of the year. Productivity gains are another contributor, with investments in manufacturing capabilities and technology alongside tight expense control driving flat adj. SG&A margin expectations in 2025. Lastly, we highlight its solid balance sheet and balanced capital allocation strategy, with ~$1.3bn deployed towards capex, M&A and share repurchases YTD, supporting long-term earnings growth.”

Perron-Piche’s Buy rating is backed up by a $142 price target that suggests a one-year upside potential of 31%. (To watch Perron-Piche’s track record, click here)

This company’s Moderate Buy consensus rating is based on 15 recent reviews that break down 11 to 4 in favor of Buy over Hold. The shares are priced at $108.38 and the average target price of $144.92 implies a gain of 34% on the one-year horizon. (See BLDR stock forecast)

GeneDx Holdings (WGS)

The next stock on today’s list is GeneDx Holdings, a company dedicated to improving outcomes in the medical field. GeneDx Holdings is a leader in providing accurate diagnostics based on genome and exome sequencing tests. These advanced tests are vital in securing accurate diagnoses of rare diseases – and it’s a known fact in medicine that earlier diagnosis correlates with better treatment outcomes. The company has one of the world’s largest data sets on rare diseases, the necessary foundation for industry-leading genome and exome testing. Clinicians can turn to GeneDx Holdings to get faster results, and researchers use the company to support accelerated drug discovery programs.

The genetic testing offered by GeneDx is based on a solid foundation: a data set that taps into more than 1.5 million genetic samples. These include 750,000 clinical exomes and genomes that have been sequenced, along with more than 100,000 mitochondrial genomes. This database allows for broad testing for a wide range of conditions, giving patients and providers the precise answers they need. GeneDx has helped to advance the medical field, generally, by identifying over 400 new relationships between diseases and genes.

GeneDx is always looking for ways to improve its diagnostic services, and in April of this year the company announced its intent to acquire Fabric Genomics. Fabric pioneered AI-powered genomic interpretation, making this a solid match; GeneDx will be able to use Fabric’s AI capabilities in tandem with its own large database. The acquisition, completed on May 7, will cost GeneDx as much as $51 million.

On April 30, GeneDx announced its 1Q25 results, and beat the forecast for both revenue and earnings. The company had a top line of $87.1 million, nearly $7.3 million better than what had been expected. At the bottom line, GeneDx ran a net loss – not unusual for cutting-edge biotech firms – but the EPS loss of 23 cents was 1 cent better than the forecast.

Keith Meister, from GeneDx’s Board, made a notable insider purchase this month. He picked up 150,000 shares in total, buying 100,000 on May 8 and 50,000 more on May 14. At the present price, these purchases are worth more than $10.1 million.

Guggenheim analyst Subbu Nambi covers WGS shares, and she likes the company’s solid reputation, seeing that as a key asset for investors to consider.

“WGS has built a strong reputation amongst geneticists, estimating 8/10 have ordered or are familiar with using them as a vendor. Based on our checks, that reputational goodwill is becoming increasingly more valuable to clinicians with more competitors on the market. WGS continuously evaluates their menu by transitioning to more profitable tests and away from commoditized panels. They are a leader in whole genome and exome innovation which puts them, in our eyes, on a path to remain a clear leader for many years in lesser penetrated sections of the rare disease market. That will open up growth ahead of most others competing in the space… Strong execution and an increasingly differentiated and proprietary database (800,000+ clinical exomes and genomes) enriched for rare diseases positions the company to drive continued double-digit revenue growth while becoming increasingly profitable,” Nambi opined.

These comments support Nambi’s Buy rating here, while her $88 price target implies that the stock will gain 30% in the next 12 months. (To watch Nambi’s track record, click here)

This genomic testing company has earned 5 recent positive analyst reviews against a single Hold, for a Strong Buy consensus rating. The stock’s trading price of $67.78 and average target price of $95 together indicate room for a 40% upside by this time next year. (See WGS stock forecast)

Jazz Pharmaceuticals (JAZZ)

Last on our insider-buying list is Jazz Pharmaceuticals, a biotech company founded in 2003 and working in the fields of neuroscience and oncology. Jazz has managed to straddle the best of both worlds in the biotech realm, with a solid portfolio of approved medicines on the market and a strong, varied pipeline of drug candidates in development. The company has a market cap of more than $6.7 billion and is domiciled in Ireland for tax purposes.

In April of this year, Jazz completed an acquisition that strengthens the company’s development pipeline, by making Chimerix, Inc., a wholly owned subsidiary. Jazz paid $935 million in cash for Chimerix, showing both the value of the acquisition and the depth of Jazz’s own pockets. The move brought the late-clinical-stage cancer drug dordaviprone, under investigation as a treatment for gliomas, into Jazz’s pipeline.

Jazz already has an extensive clinical research pipeline, with advanced programs underway in both neuroscience and oncology. One of the most notable programs is zanidatamab, currently the company’s leading anti-cancer drug candidate. The HERIZON-GEA-01 trial of zanidatamab, as a treatment for 1L GEA, is at Phase 3, and topline data is expected for readout during 2H25. Also of note in the pipeline is the Phase 2 trial of zanidatamab underway in combination with chemotherapy against HER2-positive metastatic GEA, and the Phase 3 EmpowHER-BC-303 trial evaluating zanidatamab plus chemotherapy in HER2-positive breast cancer. The EmpowHER-BC-303 is currently enrolling patients.

Dordaviprone, added to the pipeline through the Chimerix acquisition, has recently had its New Drug Application accepted for Priority Review in the treatment of recurrent H3 K27M-mutant diffuse glioma, with a PDUFA date of August 18 this year. There is also a Phase 3 trial underway, ACTION, evaluating the drug as a treatment for newly diagnosed, non-recurrent H3 K27M-mutant diffuse glioma following radiation.

As noted, Jazz also has a strong field of approved drugs on the market, and the company’s commercial activities generated $898 million during 1Q25. That figure was relatively flat year-over-year (down a half-percent), although it did miss the forecast by $85.9 million. At the bottom line, Jazz realized a non-GAAP EPS of $1.68 per diluted share, a figure that was down from $2.63 in 1Q24.

Looking ahead, Jazz updated its 2025 full-year guidance, to account for the Chimerix acquisition as well as litigation settlements related to its drug Xyrem. The new guidance includes certain increased expenses, although the revenue outlook remains the same with a range of $4.15 billion to $4.4 billion.

The insider buy here comes from one of the company’s Board members, Seamus Mulligan. Mulligan purchased 100,000 shares on May 9, followed by another 1,621 shares on May 12. The total, 101,621 shares, is now worth approximately $11 million.

Covering this biotech stock for JPMorgan, analyst Jessica Fye is pleased that the company held its revenue guidance firm, and notes the strength of the pipeline.

“We think it’s reassuring that 2025 rev guidance remains unchanged and the majority of the other guidance adjustments were due to the Chimerix acquisition and certain Xyrem antitrust litigation settlements. On the pipeline, we continue to view the phase III HERIZON-GEA-01 readout as the most highly anticipated event for JAZZ this year and topline data remains on track for 2H25. Taking a step back, with the stock trading at just ~5x our 2026 adj EPS, we see potential for significant further upside both into (and on the back of) the phase III zani GEA data coming in 2H, which we see as underappreciated at current levels,” Fye commented.

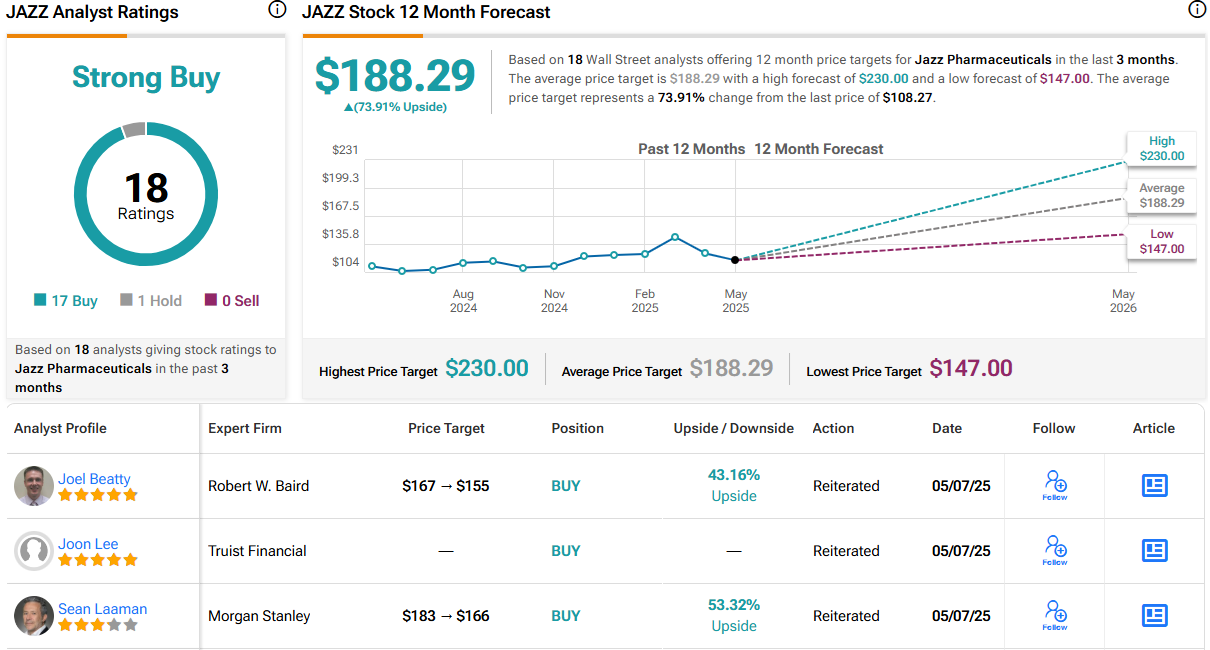

Fye puts an Overweight (i.e., Buy) rating on this stock, and she complements that with a $209 price target that points toward a 93% upside potential by next spring. (To watch Fye’s track record, click here)

The 18 recent analyst reviews here include a lopsided split of 17 Buys to 1 Hold, for a Strong Buy consensus rating. The shares have a selling price of $108.27 and their $188.29 average price target implies that the stock will gain 74% going forward into next year. (See JAZZ stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.