Legendary investor Peter Lynch has a straightforward perspective on corporate insiders and their actions in the stock market. He put it simply: insiders may sell shares for a range of reasons, but they only buy shares when they believe the price is going to rise.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Keeping a close watch on insiders’ stock purchases can prove to be a profitable investment strategy. Corporate insiders, which include company officers and board members, possess valuable knowledge about company policies and performance that can influence stock prices. They can utilize this information to make informed decisions when purchasing stocks, but they are required by law to publicly disclose their own stock holdings. This transparency allows the general public to gain insights from these purchases.

Bearing this in mind, we used the Insiders’ Hot Stocks tool from TipRanks to point us in the direction of two stocks flashing signs of strong insider buying, which warrant a closer look. Furthermore, these stocks are receiving strong approval from the analysts at banking giant Morgan Stanley, and offer up to 140% upside potential. Let’s take a closer look.

Match Group (MTCH)

The first stock we’re looking at is Match Group, the parent firm and holding company of some of the most active dating sites in the online world. Match Group is the owner of Tinder, OKCupid, and match.com – as well as nine other popular and niche online matching sites. The company has been in the business for over twenty years, and boasts that 65% of all LGBT+ couples can trace their relationships to a Match Group site.

That’s not too surprising since Match Group specializes in niche dating sites. The company has built its overall success and longevity on the scale of its operations and the breadth of its reach. The firm’s apps have tallied over 750 million downloads, and the products are available in 40 languages. With 40% of all new relationships in the US starting online, Match is solidly positioned for a strong future.

For now, the company is reporting some mixed results. In the last reported quarter, 1Q23, Match reported a top line of $787.12 million in total revenue. This was down 1.5% year-over-year and missed the analyst forecast by just under $7 million. The company takes in money globally, and so also reports revenue on a foreign exchange neutral, FXN, basis; by this metric, the top line was $822, and was up 3% y/y.

At the bottom line, Match saw 42 cents in earnings per diluted share. This EPS number was down from 60 cents in the year-ago quarter, but beat the current quarter estimates by 2 cents.

Turning to the insiders, we find company CEO Bernard Kim showing his confidence in MTCH with a purchase of 31,439 shares. This cost him over $1.08 million in a non-open market buy; Kim now holds a stake in the company worth $2.5 million.

Kim may have been bullish, but he’s not the only bull on Match Group. Morgan Stanley analyst Lauren Schenk has also given an upbeat outlook on MTCH shares, writing: “Given the encouraging April update (Tinder revenue reaccelerating, downloads improving, new user growth improving), we continue to have conviction in our out of consensus call that Tinder can reaccelerate revenue growth to double-digits or better by year-end. There is a lot of runway, and thus uncertainty, between now and then but for now our thesis remains largely on track and at 11xFY23 EBITDA, our refreshed sum of the parts analysis implies the market is paying ~12x for Tinder which we believe is a compelling entry point for a 45-50% margin business even if Tinder only delivers 10-12% revenue growth going forward.”

Schenk goes on to give MTCH stock an Overweight (i.e. Buy) rating, with a $95 price target to suggest a robust 140% upside in the next 12 months. (To watch Schenk’s track record, click here)

Overall, MTCH gets a Moderate Buy rating from the Street’s analyst consensus, based on 21 recent analyst reviews that include 15 Buys against 6 Holds. The shares are selling for $39.72 and the average price target of $53.42 implies a one-year gain of ~34%. (See MTCH stock forecast)

Align Tech (ALGN)

We started with a stalwart of the online dating realm – but it’s always easier to find a date when you have a great smile, and the next stock, Align Tech, can help with that. Align works with both high tech and orthodontics; the company’s chief product is a clear orthodontic aligner used to straighten teeth. The company uses a line of high-end 3D scanners to manufacture its proprietary Invisalign product.

Align got its start back in the 1990s, and Invisalign was first approved for use in 1998. The company has grown to become a $23 billion giant in the last 25 years, and employs over 24,000 people globally. Align saw $3.8 billion in total revenue last year, and boasts some 15.1 million Invisalign patients since the product first hit the markets.

The current year started with both the top and bottom lines better than the analysts had expected. The 1Q23 revenue of $943.1 million beat expectations by $39.9 million, while the non-GAAP diluted EPS of $2.25 exceeded the consensus by 13 cents. However, the company’s case volume in 1Q23 of 575.4K slipped by 1% compared to 4Q22.

On a positive note, Align’s Clear Aligner revenue, its chief revenue driver, grew 8% quarter-over-quarter, despite the 1% slip in case volume. The company believes that increasing customer confidence, and the post-COVID easing of restrictions in China, will bring stability to the target market. Align is guiding toward 2Q23 revenue in the range of $980 million to $1 billion.

Notably, Kevin Dallas, a member of the firm’s Board of Directors, made a significant insider purchase last week. Dallas demonstrated his confidence in the company by investing nearly $2 million to acquire 7,000 shares of the stock. As a result, his total holdings of ALGN now amount to approximately $3.7 million.

Morgan Stanley’s 5-star analyst Erin Wright is also taking a bullish stance on Align. She writes of the company: “Our longer term thesis for ALGN remains, where its leadership positioning in an attractive, highly underpenetrated market, along with rising adoption of digital workflows should support +DD earnings growth LT. All in, with its shares now trading at 35.8x our 2024e EPS, at parity with its closest competitor Straumann, we do not believe its current valuation fully reflects its longer term growth prospects.”

Wright’s comments back up her Overweight (i.e. Buy) rating on the stock, and her price target of $383 implies a solid upside of 26% out to the one-year horizon. (To watch Wright’s track record, click here)

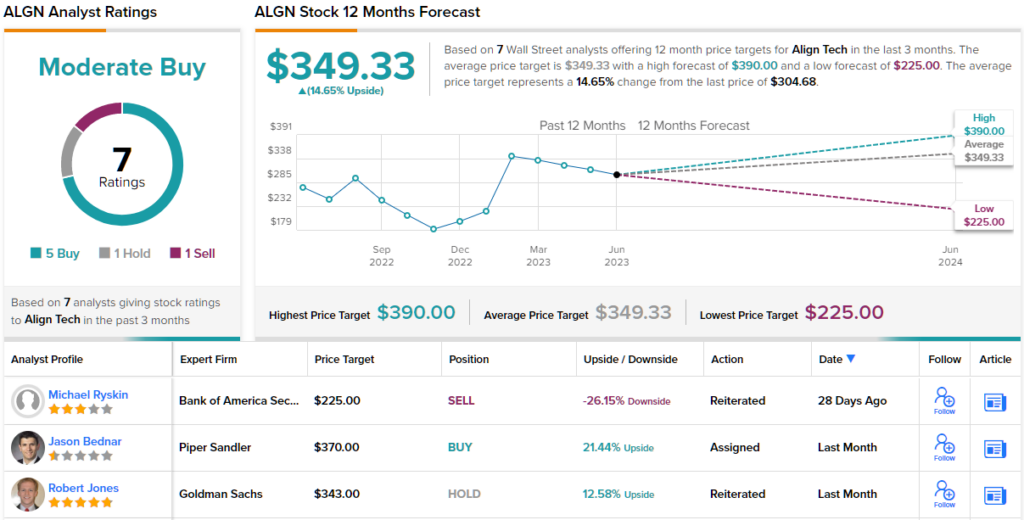

Once again, we’re looking at a stock with a Moderate Buy consensus rating from the Street. Align’s 7 recent analyst reviews break down to 5 Buys and 1 Hold and Sell each; the stock’s $349.33 average price target and $304.68 trading price suggests ~15% one-year upside potential. (See ALGN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.