Heading into the New Year, the markets are facing a confusing mix of currents. The pace of inflation is dropping, but prices remain high. Interest rates remain high, but there’s hope that the Fed will start cutting back sooner rather than later. Unemployment is low and corporate profits are up, but sales numbers show that the profits are coming from higher prices rather than higher demand.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Which way things will go is still up in the air. There is still a chance of recession – or of a strong rebound. And that’s on top of the natural uncertainties of a Presidential election year.

Watching the situation from Deutsche Bank, Industrials expert Nicole DeBlase notes that the macro clouds “have yet to clear, with the possibility of recession looming into 1H24.”

Yet with that as backdrop, DeBlase has a clear idea which stocks are ripe for the picking. “We remain selective with our recommendations,” says the 5-star analyst, “seeking out names that stand to outperform even amidst a more challenging macro backdrop for various reasons, including: 1) secular growth potential, 2) superior end market exposure, 3) outstanding operational execution, 4) self-help margin improvement opportunity, 5) significant upside to consensus EPS forecasts, 6) capital allocation optionality, and 7) extremely discounted valuation paired with any of the aforementioned factors.”

Now let’s follow this lead. Using the TipRanks platform, we’ve pulled up details on 3 stocks that DeBlase is recommending as favorites; each gets a Buy-rating from the Street, and DB sees 60%+ upside on one of them. Here they are.

Don’t miss

- Bank of America Says the S&P 500 Will Hit a New Record High in 2024 — Here Are 2 Stocks to Play That Bullish Sentiment

- These 3 stocks are Cowen’s best ideas for 2024 including AstraZeneca and Datadog

- There’s an Opportunity in the Latin American Consumer Sector, Says Jefferies – Here Are 2 Stocks to Take Advantage

CNH Industrial (CNHI)

We’ll start in the realm of heavy machinery, where CNH Industrial has a global presence in the market for agricultural and construction machinery and equipment. The company owns more than 10 well-known brand names, including CASE Construction Equipment, Case IH, New Holland, and Steyr, and can trace its roots back to 1842. CNH has a strong reputation with working farmers, both large-and small-scale, for providing quality tractors and other specialized machinery.

CNH is a truly international company, with its headquarters in the UK, its corporate ownership hailing from Italy, and its incorporation established in the Netherlands. CNH has an industrial and financial presence in 32 countries, and sells its product lines in a total of 170 countries.

As of the end of 2022, the company owned 43 manufacturing facilities, with nearly half of these, 20, in the US. The firm’s factories include extensive research and development facilities, as well as manufacturing.

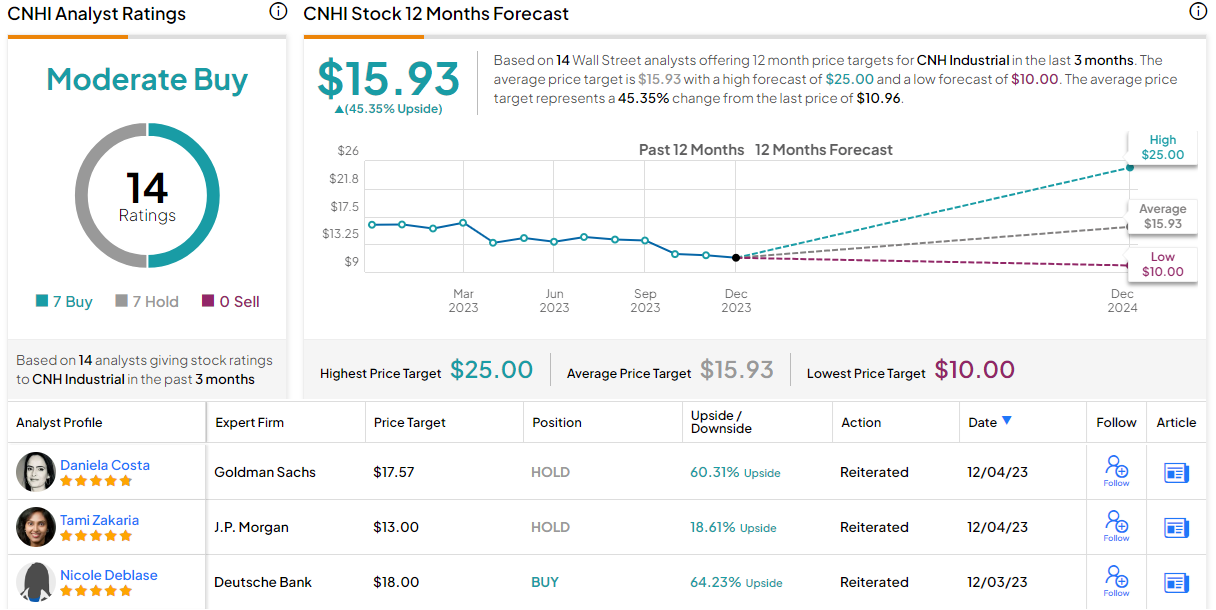

CNHI shares, though, have shed 30% this year, with disappointing results in its last quarterly release, for 3Q23, not helping its case. Citing softness in its South American market, the revenue total, of $5.99 billion, gained a modest 2% year-over-year – but missed the forecast by $220 million. The bottom line was reported as 42 cents per diluted share, in non-GAAP measures, and while it was up a penny from 3Q22 it was also a penny less than anticipated.

Despite these misses, Deutsche Bank’s DeBlase still recommends the stock. She notes that the company has a solid position relative to peers – and that recent share depreciation has put the stock into discount territory. In her words, “While we are generally avoiding ag equipment market exposure at the moment, given the cycle is only just beginning to roll over, we think CNHI brings a unique value proposition through its self-help margin initiatives. To this point, as it executes on $550m+ of cost savings in 2024, we think the company will be able to at least hold margins/earnings flattish Y/Y, which will make CNHI stand out vs. its peers. Moreover, the stock trades at a sharp discount to past pre-ag downturn multiples.”

These comments support the DB view of CNHI as a Buy, and the price target, at $18, suggests a robust upside potential of 64%. (To watch DeBlase’s track record, click here.)

Where Deutsche Bank is bullish, the Street generally takes a more guardedly positive view here. The stock’s Moderate Buy consensus rating is based on 14 recent reviews that include 7 Buys and Holds, each. The shares are trading for $10.96 and the $15.93 average price target implies a one-year gain of 45%. (See CNH Industrial’s stock forecast.)

Paccar, Inc. (PCAR)

Next up is Paccar, Inc., a name that truckers will recognize – the company is a major producer of heavy duty trucks, and it owns the Kenworth, Peterbilt, and DAF nameplates. These first two lines are known as the high-end in big-rig quality, and are found on highways all across North America, while DAF vehicles are common on Europe’s roads. Paccar has lines of light-, medium-, heavy-duty trucks under each of these nameplates, and also designs and builds the advanced diesel engines and drivetrains needed to power the vehicles.

Paccar got its start early in the history of the automotive industry, in 1905, as a builder of railway and logging equipment. In 1945, the company acquired Kenworth, and followed with Peterbilt in 1958. The 1996 acquisition of DAF, a Netherlands-based truck builder, put Paccar on the map in Europe. Today, the company has a global footprint and its high-quality products have built up a reservoir of brand loyalty and goodwill.

In addition to its core truck business, Paccar also operates Parts and Financial divisions, which in recent years have increased their share of the bottom line. On the R&D side, Paccar works with both suppliers and technology partners to streamline the process form drawing board to commercialization. Paccar’s products are available in more than 100 countries, through a network of more than 2,200 dealers. The company generates about half of its revenue and profits in the US, and half internationally.

In the third quarter of this year, Paccar reported record net income of $1.23 billion, resulting in a GAAP EPS figure of $2.34. The EPS was up some 60% year-over-year and was 21 cents per share better than the estimates. The company’s revenue total also beat the forecast, by $790 million, and came in at $8.7 billion for the quarter – a y/y gain of 23%. Shares in PCAR are up by 45% this year, outperforming the broader markets.

DeBlase, in her most recent note on the stock, points out that Deutsche Bank upgraded its stance on PCAR in October and goes on to express her belief that the company is primed for continued outperformance, writing, “We recently upgraded PCAR to Buy, as we believe that 2024 consensus forecasts are still too low, and the forthcoming Y/Y NA Class 8 truck production decline is likely to be muted and short-lived given the potential for pre-buy in 2025 ahead of the 2027 emissions standard change. PCAR also tends to execute very well during downturns, with low 15-20% decremental margins. And the balance sheet is in pristine condition, allowing the company to continue returning significant excess cash to shareholders.”

DeBlase’s Buy rating here is backed by a $115 price target indicating potential for a 23% upside in the next 12 months.

Once again, we’re looking at a stock with a Moderate Buy consensus rating with the 9 recent analyst reviews here including 4 each to Buy or Hold and 1 to Sell. Shares are trading for $93.87 and the $96.67 average price target suggests the shares will stay rangebound over the coming year. (See Paccar’s stock forecast.)

Johnson Controls (JCI)

Last on our DB-backed list is Johnson Controls, a venerable name in the world of HVAC and one of Fortune’s Global 500 names. Johnson Controls is a ~$37 billion company that brought in over $25 billion in revenue last year. The company offers solutions to building owners and facility managers for indoor climate control issues, such matters as building automation and controls, fire prevention and suppression, industrial refrigeration and energy efficiency, as well as the more traditional HVAC fare.

In addition, Johnson Controls also offers a line of Smart Building systems, designed to ensure a healthier building interior environment. These systems can improve indoor air quality while also creating a more energy efficient space, saving money for the building’s managers while providing tenants and workers with a better working environment.

Johnson Controls might not be a household name, but it’s certainly well-known in a wide range of industries. The company boasts customers across the economy, and has worked with Federal and State governments, healthcare providers, the hospitality sector, educational institutions at all levels from K through college, industrial and manufacturing facilities, and data centers – for whom proper climate control is essential.

The company’s last earnings report, for fiscal 3Q23, showed a revenue total of $7.1 billion, up 8% y/y, although $70 million under the estimates. At the bottom line, the $1.03 per share, by non-GAAP measures, was up a solid 21% y/y and matched with the pre-release estimates.

Since the August print, however, shares have mostly been in a downtrend due to a disappointing outlook. For fiscal 2023, the company said it now expects growth in high single-digits, as opposed to the 10%+ anticipated beforehand.

DeBlase, in her coverage for Deutsche Bank, does not shy away from the issues in this stock – but she also notes that the company has real potential to recover and that the share price currently presents a good entry point. DeBlase writes, “This is not a stock for the faint of heart, and we view it more as a high risk/high reward option within the MI/EE group. JCI is among the cheapest names in our coverage universe following two years of patchy operational execution, but we remain attracted to the company’s secular growth opportunity and self-help margin initiatives. If execution gets back on track, the stock could benefit from the winning combination of EPS upside and a multiple re-rating.”

These comments back up the 5-star analyst’s Buy rating, and her $74 price target implies a 36% gain waiting ahead for the stock.

Overall, it seems that Wall Street comes down on the side of the bulls here. The Moderate Buy consensus rating is based on 11 recent analyst reviews, including 8 to Buy and 3 to Hold. The stock’s $68.73 price target and $54.42 trading price together suggest a 26% potential upside by this time next year. (See Johnson Controls’ stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.