This summer, the previously unassailable Magnificent Seven stocks have experienced some uncharacteristic weakness. Investors have been taking stock of both their large gains over the past year and their relatively elevated valuations and evaluating whether there are more attractive opportunities in other sectors of the market. This has led to something of a rotation into more value-oriented sectors like Healthcare and Financials.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

But these are still some of the world’s most dominant companies, and the upside of this summer swoon is that it has created the opportunity to buy some of their shares at more attractive entry points. So let’s take a look at three of the top Magnificent Seven stocks — GOOGL, AAPL, and MSFT — and determine which looks like the most attractive investment opportunity for investors right now.

Alphabet (GOOGL)

Amid this summer’s tech sell-off, Alphabet, the parent company of Google, YouTube, and more, is in correction territory, down 16.6% from its 52-week high. But there’s a lot to like about Alphabet stock, and I am bullish on it.

Magnificent Seven stocks aren’t typically associated with value investing, but there’s a reason that Alphabet keeps showing up in the portfolios of some of the market’s top value investors, like Li Lu of Himalaya Capital, Oakmark’s Bill Nygren, and Oakcliff’s Bryan Lawrence. In fact, between its two share classes, Google makes up nearly 40% of Himalaya’s portfolio, representing a massive bet for Lu.

These value superstars recognize that Alphabet is surprisingly cheap. The stock trades at 21.1 times 2024 consensus earnings estimates but looks even cheaper heading into 2025, where it trades at just 18.5 times forward estimates.

This means that Alphabet is trading at a discount to the broader market, with the S&P 500 (SPX) trading at 23.2 times earnings and 21.9 times forward earnings. This presents an attractive opportunity for a world-class company with a dominant position in search and other strong businesses like YouTube, especially given its impressive earnings growth of 21.6% per year over the past five years.

Yes, Alphabet faces challenges from regulators — a federal judge recently ruled that Google violated antitrust laws, and the Department of Justice may push for a breakup. But this isn’t necessarily the likeliest outcome, and Google can appeal.

And even if it does happen, it could actually be a boon for Alphabet shareholders, as owning standalone businesses could unlock additional value. Imagine receiving a spinoff of YouTube shares? Many analysts believe YouTube would be an extremely lucrative standalone company in its own right and that some of its value is obscured by being part of the larger conglomerate.

I’m bullish on Alphabet, as it is trading in value stock territory after this summer’s correction, and its cheap valuation seems like a great bargain for a dominant business with a track record of strong earnings growth. Plus, any potential jostling with regulators could have the silver lining of unlocking new value for shareholders. Additionally, analysts believe this Strong Buy stock harbors significant upside potential, as we’ll discuss below.

What Is the Price Target for Alphabet Stock?

Turning to Wall Street, GOOGL earns a Strong Buy consensus rating based on 29 Buys, seven Holds, and zero Sell ratings assigned in the past three months. The average GOOGL stock price target of $205.18 implies 27.2% upside potential from current levels.

See more GOOGL analyst ratings

Apple (AAPL)

Apple, the world’s largest company by market cap, has held up better than Alphabet and many of its tech-sector peers during this summer’s rotation. It’s down just 5.2% from its highs. While this is great for long-term Apple holders, it also means there is less of an opportunity for new investors to buy ahead of a rebound. Apple stock is also quite a bit more expensive than Alphabet (not to mention the broader market), making me neutral on the stock. Shares trade at 33.1 times 2024 earnings and 29.9 times consensus 2025 earnings estimates.

The stock’s earnings growth has also been slower than Google’s. While Google has grown earnings 21.6% per year over the past five years, Apple has grown them at a solid but slower 15.6%. Apple’s growth over the next five years is also projected to be slower than Alphabet’s, with 11.1% growth projected versus 20.5% for Alphabet. Obviously, five years is a long way out, so these numbers should be taken with a grain of salt, but this is a large gap.

Lastly, Warren Buffett’s Berkshire Hathaway (NYSE:BRK.B), the company’s top shareholder with a massive stake, recently shocked the market when it sold nearly half of its position. Apple is still Berkshire’s largest holding, but perhaps Buffett sees Apple as having less upside than it did in the past.

Apple is an all-time great company and stock, but right now, it appears to have less upside than Google for these reasons.

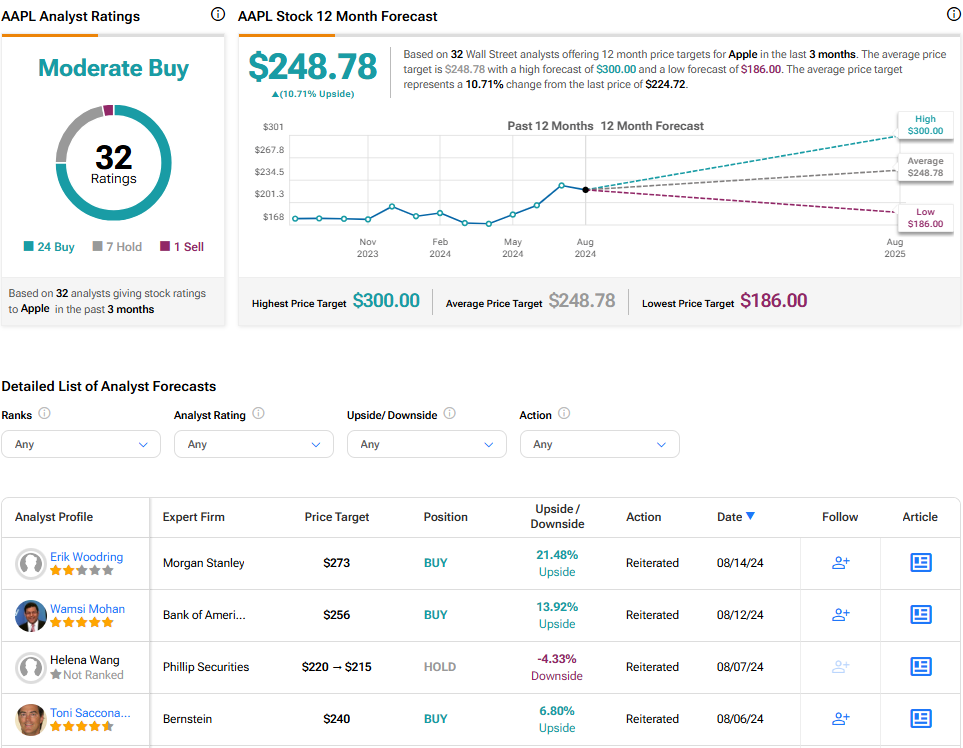

What Is the Price Target for AAPL Stock?

AAPL earns a Moderate Buy consensus rating based on 24 Buys, seven Holds, and one Sell rating assigned in the past three months. The average AAPL stock price target of $248.78 implies 10.7% upside potential from current levels.

Microsoft (MSFT)

An analysis of Magnificent Seven stocks without Microsoft just wouldn’t feel complete. Shares of the mega-cap stock have fallen 10.3% from their high — less than Alphabet but more than Apple.

In terms of its valuation, Microsoft is also much more expensive than Alphabet and roughly in line with Apple, trading at 31.6 times consensus Fiscal 2025 earnings estimates (Microsoft just reported fourth-quarter earnings and is already into Fiscal 2025).

Microsoft’s earnings growth has also fallen between that of Alphabet and Apple — the company has grown earnings per share at an 18.5% rate over the past five years and is projected to grow EPS at 14.6% per year over the next five.

This is better than Apple’s earnings growth but trails Alphabet’s, and with the large gap in valuation between the two stocks, Alphabet clearly looks like the more compelling buy. Overall, I am neutral on MSFT stock due to its relatively elevated valuation.

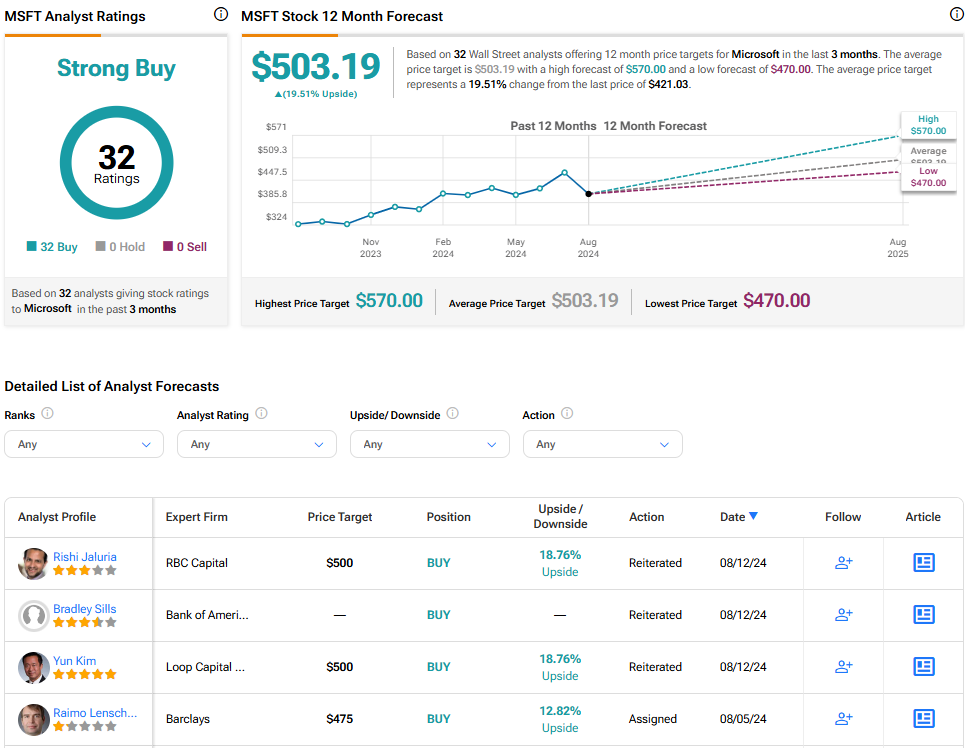

What Is the Price Target for MSFT Stock?

MSFT earns a Strong Buy consensus rating based on 32 Buys, zero Holds, and zero Sell ratings assigned in the past three months. The average MSFT stock price target of $503.19 implies 19.5% upside potential from current levels.

The Winner Is…

Of these three Magnificent Seven giants, Alphabet looks like the most attractive buying opportunity right now by some margin. Not only is the stock significantly cheaper than that of Apple or Microsoft, but it has been posting better earnings growth over the past five years and is projected to continue doing so. Alphabet has also sold off more than its peers, creating more of an opportunity to buy before a rebound.

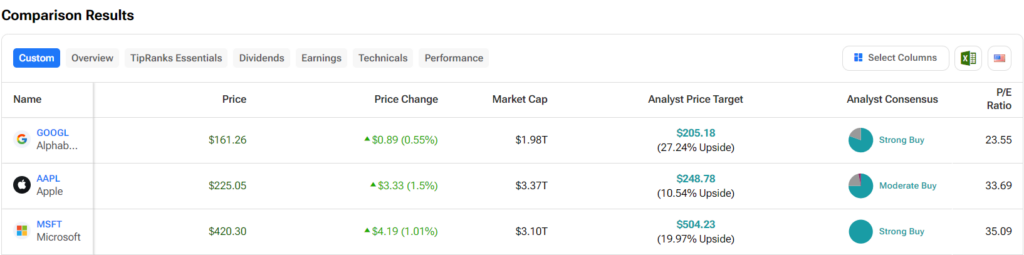

Below, you can check out a comparison of Alphabet, Apple, and Microsoft using TipRanks’ Stock Comparison Tool, which allows investors to compare up to 10 stocks at a time on a variety of factors, ranging from valuation to recent performance. As you can see from the table, Alphabet is by far the cheapest stock in terms of valuation, and analysts see it as having the most upside.

One of the primary headwinds standing in Alphabet’s way is the DOJ lawsuit, but even if it does culminate in the company splitting up, businesses like YouTube would be incredibly attractive standalone businesses, and a split up could unlock significant value for shareholders.