The healthcare sector has held up strong amid the global pandemic, yet not all names have escaped COVID-19’s grasp. For several companies inhabiting the space, historically low levels of utilization for both traditional procedures and services as a result of COVID-19 and the expected mass consumption after restrictions are loosened have presented significant headwinds. It doesn’t help that unemployment also poses risks.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Against this backdrop, investment firm Goldman Sachs took a deep dive into the space, hoping to get a better sense of where healthcare stocks stand during these unprecedented times. Given the uncertainty still hanging in the balance, the firm points out that investments in the sector aren’t without risk. That being said, it argues that some names are poised to deliver a strong performance in the long run.

With this in mind, we wanted to take a closer look at two healthcare stocks that just received Goldman Sachs’ stamp of approval, with the firm projecting upside potential of more than 30% for each. Using TipRanks’ database, we found out that the rest of the Street is also on board as both have earned a “Strong Buy” consensus rating.

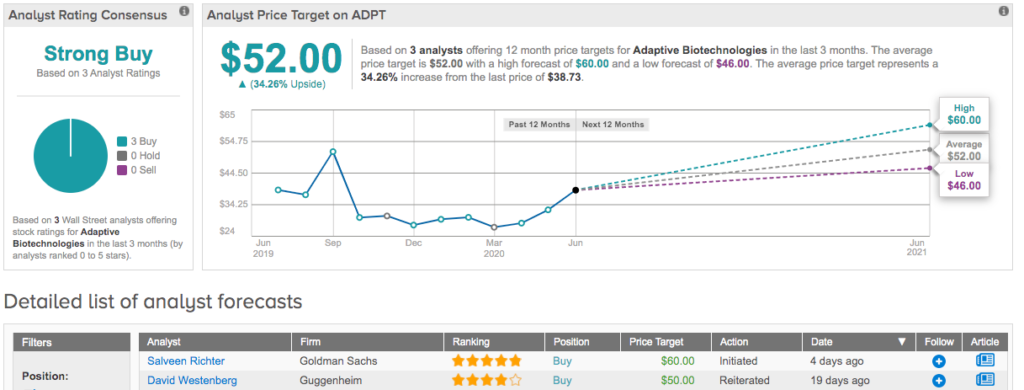

Adaptive Biotechnologies Corporation (ADPT)

Taking advantage of the inherent biology of the immune system, Adaptive Biotechnologies wants to transform the way diseases are diagnosed and treated. Based on the strength of the sequencing and diagnostic company’s portfolio, Goldman Sachs believes that now is the time to pull the trigger.

Representing the firm, five-star analyst Salveen Richter tells clients ADPT offers commercial technologies designed for specific use cases. Its immunoSEQ platform is used in academic and biopharma research while clonoSEQ was developed for a clinical setting, with the latter able to detect minimal residual disease (MRD). This will be expanded to include blood-based (liquid biopsy) testing (versus bone marrow), and will increasingly be used as a primary endpoint during clinical trials.

The good news doesn’t end there. Richter argues that its clinical diagnostic product pipeline, which includes immunoSEQ Dx from its collaboration with Microsoft, as well as its drug discovery pipeline that features the Amgen-partnered COVID-19 program, are capable of driving significant upside.

On top of this, ADPT made its foray into the world of drug development, collaborating with Genentech on the development of cellular therapies in oncology. Going beyond this agreement, Richter thinks the company could potentially pursue other opportunities in cell therapy separate from the partnership, including other disease states like autoimmune diseases and cancer vaccines.

“We view the collaborations with industry-defining leaders such as Genentech, MSFT and AMGN as validating to ADPT’s approach to advance immune-driven medicine, and note the Genentech agreement provides ADPT with significant milestone (potentially up to $1.8 billion in aggregate) and royalty payments on future sales of drugs that are created by utilizing ADPT’s platform,” Richter explained.

To sum up her take, Richter noted, “Overall, we have a positive view on the fundamental trajectory of the business and innovative platform technology, and see immunoSEQ Dx and drug discovery as significant value drivers in the future, supported by steady revenue growth from ADPT’s base businesses for clonoSEQ and immunoSEQ.”

Based on all of the above, it’s no wonder Richter kicked off her coverage of ADPT by publishing a Buy recommendation. With a $60 price target, shares could climb 55% higher in the next twelve months. (To watch Richter’s track record, click here)

All in all, other analysts echo Richter’s sentiment. 3 Buys and no Holds or Sells add up to a Strong Buy consensus rating. Given the $52 average price target, the upside potential comes in at 34%. (See Adaptive Biotechnologies stock analysis on TipRanks)

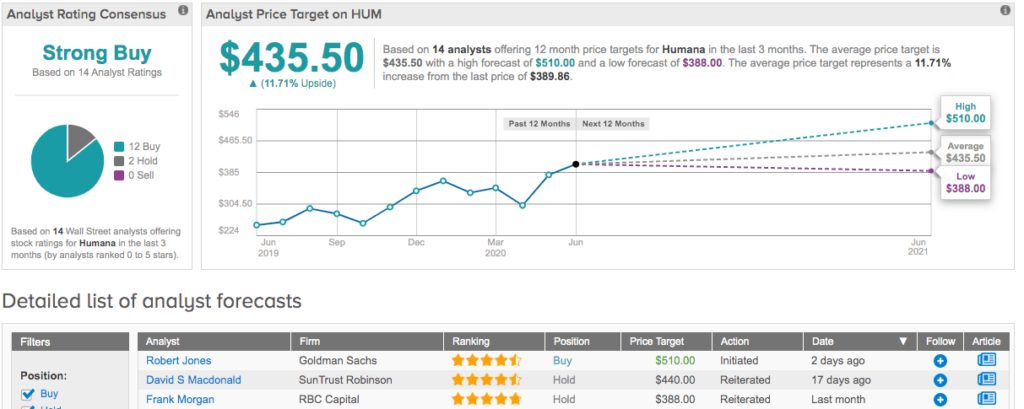

Humana Inc. (HUM)

While acknowledging that health insurance company Humana has faced newer entrants in the Medicare Advantage (MA) market, its mix of business and sheer size make it a stand-out, in Goldman Sachs’ opinion.

Weighing in on the stock for the firm, five-star analyst Robert Jones sees HUM’s scale, brand reputation and provider infrastructure as positioning it to “continue to gain share in the fastest growing vertical of Managed Care.” He added, “Importantly, continued growth in this end-market also has a more pronounced impact to HUM’s bottom line versus other managed care organizations (MCOs) given HUM’s more concentrated exposure to MA.”

In the past, the company’s exposure within the MA space has been “an attractive value proposition given the secular growth drivers that are present”, but now, the segment looks even stronger, according to Jones. For the most part, MA has managed to escape the impacts of COVID-19, which could help drive multiple expansion.

Another key component of Jones’ bullish thesis is its primary care strategy. As part of this approach, HUM has opened payor-agnostic, senior-focused primary care centers, with it building over 260 of these owned, joint venture or alliance primary care centers. The company also announced another 35 are set to open in 2020.

Expounding on the benefits of its strategy, Jones commented, “Looking forward, we think HUM’s primary care strategy could be a meaningful growth lever for the company. In our view, the opportunity from these centers is threefold, in that it could help HUM (1) recruit and retain MA members, (2) increase the profitability of the members that are managed under these value-based arrangements, and (3) recognize long-term EBITDA growth from the providers themselves.” Of these, the analyst believes the possibility of stronger growth and retention, as well as improved member profitability are “the most meaningful.”

Everything HUM has going for it prompted Jones to take a bullish stance. In addition to initiating coverage with a Buy rating, he set a $510 price target. This target suggests shares could surge 31% in the next year. (To watch Jones’ track record, click here)

Turning now to the rest of the Street, most other analysts are on the same page. With 12 Buys and 2 Holds assigned in the last three months, the word on the Street is that HUM is a Strong Buy. Additionally, the $435.50 average price target brings the upside potential to 12%. (See Humana stock analysis on TipRanks)