Eventbrite (EB) offers its customers an electronic ticketing, and event planning and promoting platform. It operates in the United States and internationally. Eventbrite went public through an IPO in September of 2018.

I am bearish on EB stock. (See Analysts’ Top Stocks on TipRanks)

Pandemic Ground Zero

Given the nature of Eventbrite’s business, it was bound to be significantly hurt by the pandemic. With events being cancelled worldwide, the business basically ground to a halt in Q2 of 2020.

Quarterly revenue went from $82.7 million for Q4 2019, to $49.1 million in Q1 2020, all the way down to a dismal $8.4 million in Q2 2020. This amounts to a decrease of nearly 90%.

Since then, its revenue has recovered. However, the recovery has been slower than would be optimal. Quarterly revenue languished in the $21 million to $28 million range for the three quarters subsequent to Q2 2020, before rising to a respectable $46.3 million for the three months ended June 30, 2021. This is still nearly 50% less than pre-pandemic figures.

Even worse, Eventbrite has never posted a quarterly operating profit as a public company. Since January of 2020 alone, the company has lost $242.4 million.

Stock Price Disconnect

One would expect that the stock price and market cap would be severely lower than December 31, 2019 — the last full quarter prior to the pandemic in the United States. However, this is not the case. In fact, the stock price is more than 1% higher now than it was then.

The market cap is over 15% higher due to more shares being available on the market. To put it another way, the stock price is telling us that the company should now be worth 15% more than it was when it was a growing company with events being planned worldwide.

If this was not concerning enough, long-term debt has also skyrocketed during the last several quarters. At the March 2020 report date, Eventbrite was long-term debt free. The company has since added $352.6 million in long-term debt.

Nonetheless, EB does have plenty of cash on hand, and is in no imminent danger of not being able to meet its obligations. With that said, it has created positive cash from operations (CFO) through the slow paying of bills.

Increases in accounts payable have amounted to over $150 million increases in cash from operations over the previous two quarters. Total CFO for this period was only $132.6 million despite the changes in payables. This is a concerning trend.

Areas of Opportunity

It is not all doom and gloom for the company’s future. The latest revenue figures are at the very least a large step in the right direction. There is also a general sentiment that pent-up demand exists for event attendance.

Personal spending and disposable incomes are up significantly from the end of 2019. As vaccines continue to take hold and consumers again feel comfortable at events, it is possible that demand increases past 2019 levels in short order.

If this happens, EB has a bright future, however the stock may still be overvalued. EB stock is trading at a price-to-sales (PS) ratio of 15.6x. The stock is trading as though the crushing weight of the pandemic has already been lifted, and it has not been.

Significant risks, such as a new variant or holiday resurgence, still exist. EB was also not growing rapidly even before COVID-19. From December 31, 2018 to December 31, 2019, revenue increased only 8% — not nearly enough to justify current multiples.

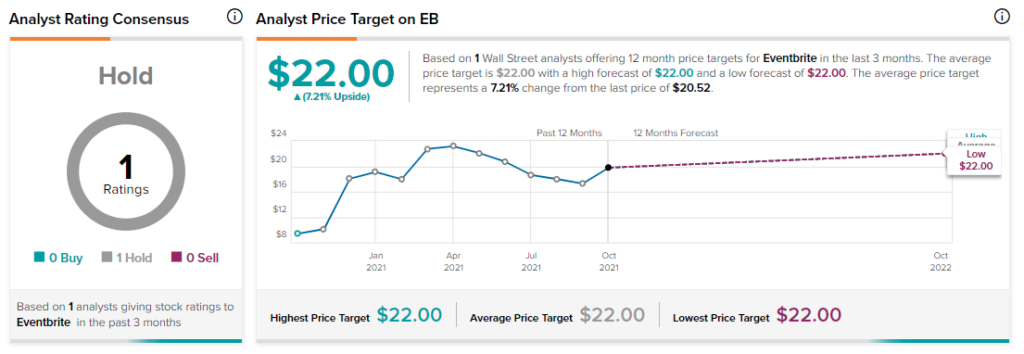

Wall Street’s Take

On Wall Street, there is very limited coverage of Eventbrite. A single analyst reports a Hold rating.

The average Eventbrite price target of $22 implies 7.2% upside from the current price.

Concluding Thoughts on Eventbrite

Eventbrite was caught up in a disaster that the company did not create, but was forced to contend with. Its revenue and earnings were crushed when events around the world were cancelled.

Eventbrite’s revenue has still only recovered to roughly half of what it was. Yet, the stock trades above 2019 levels. The company is also being valued as a growth stock. However, growth was elusive even prior to the COVID-19 spring of 2020.

Disclosure: At the time of publication, Bradley Guichard did not have a position in securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates, and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices or performance.