Easterly Government Properties stock (NYSE:DEA) recently hit record lows, resulting in its dividend yield climbing to a hefty 9.6%. With a portfolio of 89 purpose-built properties leased to key U.S. agencies such as the FBI, DEA, ICE, and FDA, among others, Easterly Government is a distinctive REIT in the sector. While prevailing macroeconomic challenges justify the stock’s prolonged decline, the REIT’s one-of-a-kind qualities should continue generating strong income for investors. Thus, I am bullish on the stock.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

What are Easterly Government’s One-of-a-Kind Qualities?

Before discussing Easterly Government’s dividend, it’s essential to appreciate the distinctive qualities that set this company apart. These attributes play a pivotal role in shaping the company’s prospects, including the quality of its dividends.

For those unacquainted with Easterly Government, the company specializes in providing mission-critical properties to various U.S. government agencies. As mentioned earlier, the company owns 89 operational properties in the United States, primarily leased to agencies such as the Federal Bureau of Investigation (FBI), the U.S. Department of Veterans Affairs (VA), the Defense Health Agency (DHA), the Environmental Protection Agency (EPA), and the U.S. Citizenship & Immigration Services (USCIS).

Therefore, a staggering 98.5% of its annualized lease income is secured by the full faith and credit of the U.S. government.

The immense advantages of having the U.S. government as your sole tenant create a formidable moat. The key differentiator setting Easterly Government apart from typical real estate investment trusts (REITs) lies in the unwavering faith and credit of Uncle Sam. The U.S. government stands as one of the most dependable creditors globally, having never defaulted on its obligations. Thus, the REIT essentially faces no counterparty risk.

Also, it is safe to say that no matter the underlying conditions, the agencies Easterly Government leases its properties to will never go away. They are fundamental for vital operations and national security. Thus, along with no counterparty risk, the company also enjoys no vacancy risk.

These arguments are evident by the fact that since its IPO, Easterly Government has consistently maintained a near 100% occupancy ratio, underscoring the resilience of its operations. The mission-critical nature of its properties is also apparent in agencies opting for long-term leases, evident in Easterly Government’s impressive weighted average remaining lease term of 10.4 years. With full occupancy and exceptional leases, the company showcases remarkable predictability and superior cash-flow quality.

Finally, as a pioneering force within its niche sector, the company has cultivated profound know-how of the intricate General Services Administration (GSA) appropriation process, protocols, and organizational culture. Management not only comprehends the intricacies of missions and the hierarchical structures of tenant agencies but has also forged distinctive relationships. Because of this and the high barriers to entry in the GSA space, the company’s competitive advantage and overall solidity are further reinforced.

How Safe is Easterly Government’s 9.6%-Yielding Dividend?

With shares of Easterly Government plunging in recent months, it’s no wonder investors are questioning the safety of the stock’s hefty 9.6% dividend yield. Well, in my view, the company’s dividend is quite safe, backed by the unique qualities discussed earlier. The stock’s high yield on Wall Street is likely a reaction to concerns about elevated interest rates hampering growth prospects, leading to an emphasis on dividends for returns.

However, there is something important to note here: Easterly Government’s exceptional qualities have garnered favor from creditors, with 97.7% of its debt fixed at advantageous rates and extended maturities. Despite widespread interest rate increases, the company’s Q2 interest expenses rose only by 2%. For context, most REITs have experienced spikes anywhere from 30% to 100% during this period. Still, elevated interest rates may pose a hurdle to the company’s growth prospects by discouraging additional financing.

Another factor that diminishes Easterly Government’s growth prospects is the enduring nature of its long-term leases. Despite containing modest periodic adjustments, the extended duration of these leases—often spanning a decade or more—restricts the company’s ability to revisit and renegotiate terms for an extended period. In opting for prolonged leases, the company has prioritized added security and predictability, albeit at the expense of leasing rate growth opportunities.

In the meantime, however, Easterly Government should have no issue covering its current level of payouts. The $1.06 annualized dividend should remain covered by its core funds from operations per share (FFO/share, a cash-flow metric used by REITs), which management expects to land in a range of $1.13 to $1.15 for Fiscal 2023.

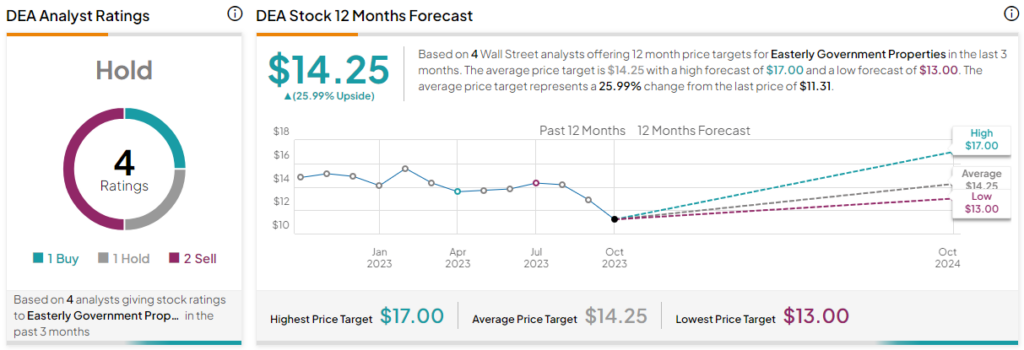

Is DEA Stock a Buy, According to Analysts?

Turning to Wall Street, Easterly Government has a Hold consensus rating based on one Buy, one Hold, and two Sells assigned in the past three months. At $14.25, the average DEA stock forecast implies 26% upside potential.

Conclusion

In conclusion, Easterly Government Properties stands out as a compelling high-yield opportunity in the real estate sector. The company’s mission-critical properties leased to U.S. government agencies, secured by the full faith and credit of the U.S. government, provide an unparalleled moat and insulate it from counterparty and vacancy risks.

With a near-100% occupancy ratio, impressive lease terms, and deep know-how of the GSA’s intricacies, Easterly Government has proven its resilience and competitive advantage.

The safety of Easterly Government’s 9.6% dividend yield is underpinned by these qualities and favorable debt terms. While concerns about interest rate hikes may impact growth prospects, the company’s ability to cover its dividends should remain solid remains solid. Thus, income-oriented investors are likely to find the stock suitable for their needs.