There’s no other way of saying it, it’s been a rough old 12 months for DraftKings (DKNG). The stock has shed 66% of its value as investors have fled from growth and speculative assets to more safe havens.

BTIG analyst Clark Lampen also thinks recent sentiment about the company and peers has “been muted,” with some apparently worried certain states will shortly raise taxes following NY’s launch of sports betting.

However, Lampen thinks other measures such as restrictions on marketing, or tighter background checks are more likely. Interestingly, it is the former which the analyst believes would be a “positive.” “Either way,” Lampen went on to add, “We expect DKNG to stay focused on growing MUPs (monthly unique payers), given improving net CAC rates and signs that smaller operators may be looking for exits.”

Lampen also gets the sense that in order to help with player retention and engagement, DraftKings is keen on growing its content portfolio. Such a notion is given credence by recent hires for programming and media roles.

All of the above forms the backdrop for the company’s upcoming Q4 earnings report on Friday, Feb 18.

Despite the NFL season kicking off with slightly declining wagers along with a difficult start to the quarter, based on state data and a dissection of B2C revenue, the analyst sees the company surpassing its guidance for revenue of $444 million and EBITDA of ($148 million), both of which are the consensus estimates too.

With the GNOG acquisition anticipated to close by the end of the month, to factor in the contributions from 2Q22 onwards, the analyst has raised his revenue forecasts for 2022 from $1.85 billion to $2.11 billion.

Lastly, over the next few years, Lampen sees a “critical mass of states reaching breakeven to profitable run-rates.” This indicates there’s a good chance DraftKings could report EBITDA profits by 2023 with “sustained profitability from ’24 forward.”

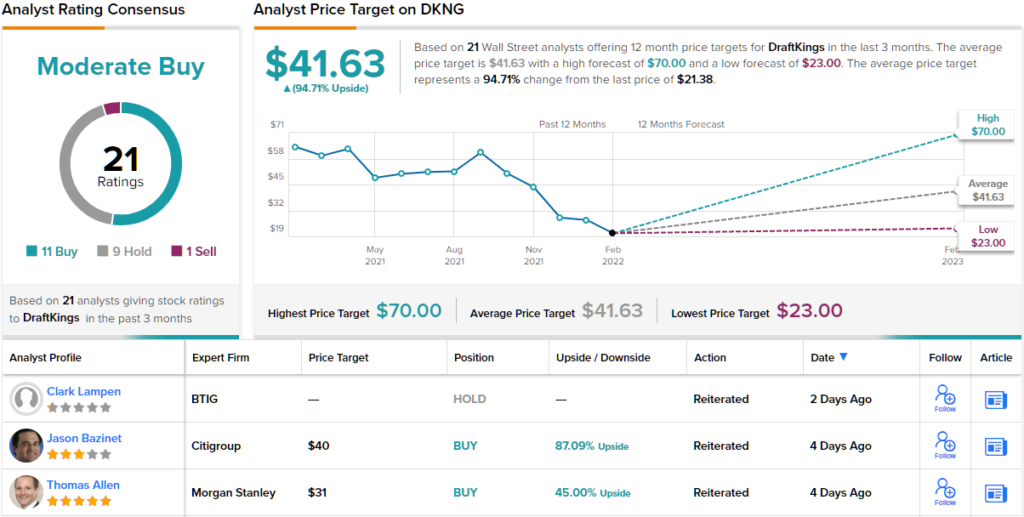

So, what does this all mean for investors, then? For now, Lampen sticks with a Neutral (i.e. Hold) rating and no fixed price target in mind. (To watch Lampen’s track record, click here)

8 other analysts join Lampen on the sidelines, and with the addition of 11 Buys and 1 Sell, the stock qualifies with a Moderate Buy consensus rating. However, the outlook is far more conclusive where the share price is concerned; the forecast calls for one-year gains of a bountiful 91%, given the average price target clocks in at $41.63 and change. (See DraftKings stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.