Domino’s Pizza (NYSE: DPZ) is a legend in the pizza delivery space, often mentioned in the same breath as the biggest pizza chains on the planet. The stock gained in Tuesday’s trading session thanks to an upgrade at UBS (NYSE: UBS). Analyst Dennis Geiger upgraded the company from Neutral to Buy. Geiger noted that, while some corners expressed concern about a potential decline in pizza sales, these concerns were largely overblown.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Moreover, Geiger and UBS noted that there were some factors that could actually step up U.S. sales trends in pizza. Finally, the company also had what was described as a “compelling long-term growth profile.”

I don’t quite share Geiger’s optimism on Domino’s, but I also don’t look for it to lose much ground, either. In fact, I don’t look for it to make much movement in any direction. As a result, I’m neutral on Domino’s.

Some Serious Issues in Investor Sentiment for DPZ Stock

On the surface, Domino’s investor sentiment looks fairly quiet. That’s not the case in some metrics, however. Right now, Domino’s Pizza has a 6 out of 10 Smart Score on TipRanks. That’s slightly above the midpoint of Neutral and implies only a slightly better than even chance the company will ultimately outperform the broader market.

However, it’s a wholly different story among Domino’s insiders. Insider trading at Domino’s is strongly Sell-weighted, both in the aggregate and in informative terms.

The latest “Informative Sell” was just two months ago when director Andrew Balson sold just short of $5.4 million in stock. Meanwhile, there hasn’t been an Informative Buy in a year.

The aggregate only drives the point home harder. In the last three months, insiders staged three selling transactions, and that’s the entirety of insider trading. Meanwhile, in the last 12 months, the picture has worsened in objective terms. While there were 20 Buy transactions staged, there were 54 Sell transactions.

Pizza’s Broad Appeal Limits Downside Risk for DPZ Stock

The problem with trying to project Domino’s Pizza’s future is that its product is surprisingly stable. This makes forecasting the macroeconomic impact rather difficult. While it’s safe to say that some would delay a new car purchase in a souring economy or put off buying a new television, the same can’t be said for pizza.

It’s pizza, after all. It’s a food, and a comparatively inexpensive food as well. There aren’t many readily-available substitute goods to pivot into. Further, there are also those who will pivot into pizza from other options. For every household that decides to forego their Friday night pizza some night to save cash, there’s likely someone picking it up instead of a steak dinner.

However, there are some advantages to Domino’s. For instance, there are those “long-term catalysts” that UBS described. Some of these include new programs to improve driver shortages as well as price increases on certain promotional items. Even UBS notes that Domino’s represents “a very affordable dinner option for families.”

Domino’s is also working to crack new markets with cross-promotional operations. For instance, a recently-announced promotion between Domino’s and several area fire departments is offering free pizza for anyone with working smoke detectors.

Those who order delivery may be chosen at random to have their pizza accompanied by a fire truck. If the smoke alarms in the home work when the pizza arrives, the pizza is free.

Domino’s recently made its affordable dinner option even more so with a 20% discount for everything ordered online. While the deal was for a limited time, customers no doubt welcomed the relief.

Domino’s locations in Malaysia and Singapore took advantage of the popularity of the open-world RPG “Genshin Impact” to offer a promotional deal that brought “emergency food” supplies to gamers. The packages not only offered food and soft drinks but also promotional merchandise related to the game.

At the end of the day, Domino’s has a fairly static customer base. It will lose some customers to worsening macroeconomic conditions, of course, but it likely won’t lose many. In addition, it will likely catch a few new ones stepping down from more expensive dinner options.

Thus, that suggests that Domino’s really can’t swing that far in any one direction. That makes it a good candidate to hold, but not so much a good candidate to buy in on.

Is DPZ Stock a Good Buy?

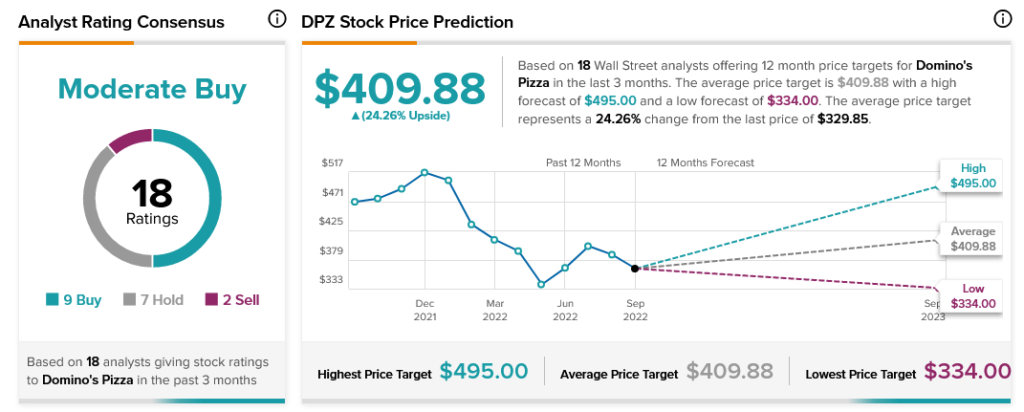

Turning to Wall Street, Domino’s Pizza has a Moderate Buy consensus rating. That’s based on nine Buys, seven Holds, and two Sells assigned in the past three months. The average Domino’s Pizza price target of $409.88 implies 24.3% upside potential. Analyst price targets range from a low of $334 per share to a high of $495 per share.

Conclusion: Domino’s Will Likely be Resilient to Macroeconomic Conditions

It’s safe to say that, on a certain level, UBS’ projections are exactly right. Concerns about losses in the pizza sector are almost certainly overblown. Families aren’t blowing the food budget by getting pizza on a Friday night. Thus, their likelihood of removing it from the budget altogether is slim. Domino’s, by extension, isn’t likely to be much hurt by these macroeconomic conditions.

Its share price, while already quite high enough to scare off many small investors, is still below its lowest targets. That suggests at least a little room for improvement.

Given that Domino’s store counts have been steadily gaining ground over the last 10 years as well, it’s a safe bet that it won’t lose much ground in worsening conditions.

I don’t look for Domino’s to blast up in terms of growth, but I certainly don’t look for it to falter. That’s why I’m neutral on Domino’s; it’s a safe bet, as long as your expectations for growth are sufficiently tempered.