Things have gone from bad to worse for Disney (DIS) stock, which is now at risk of falling below $100 per share. It’s been the perfect storm of headwinds since the pandemic began over two years ago.

From shuttered parks to a streaming service that ran out of gas, it’s not been an easy ride for Disney shareholders. Indeed, it’s been frustrating enough to throw in the towel with the never-ending list of problems.

From One Bob to Another

CEO Bob Chapek did not have an easy job when he took the reins from long-time top boss Bob Iger. The CEO change came amid the firm’s worst crisis ever. Undoubtedly, Chapek was thrown right into the deep end when he took the helm.

Though his performance was somewhat decent in the early part of the pandemic, with substantial investment made in the streaming platform Disney+, the meager performance has some questioning the new CEO’s execution. Chapek’s fumbling of the controversial “Don’t Say Gay” bill and the ensuing battle with Florida’s governor Ron DeSantis did not help the cause.

While the list of issues could continue to mount, I do think the second half of 2022 could have the potential to be far brighter than its first half. As Chapek attempts to right his wrongs, I do believe there are a lot of gains to be had by giving shares of the house of mouse the benefit of the doubt during its darkest hour.

Disney Stock: The Second Half Could be Less Hostile

The valuation is incredibly depressed, and with China’s lockdowns likely to lift in time for summer, Shanghai’s Disney Resort may finally be able to power the parks’ business higher. Currently, no reopening date is set for Shanghai Disneyland. Regardless, things likely can only get better for theme parks moving forward.

Further, the streaming business is in a slump right now, thanks to a broader cooling of the industry itself. With intriguing new TV series, including Obi-Wan Kenobi, not far away, we could easily witness Disney+ begin to take market share away from its rivals. Recent weakness in Netflix (NFLX) may be more of a sign that the streaming kingpin’s subscribers are up for grabs rather than signaling the beginning of the end for streaming as we know it.

Streaming may have faced difficult year-over-year comparables, but it’s here to stay. And the company with the most quality content will likely walk away as the winner of the streaming war. In that regard, I think Disney has what it takes to one-up Netflix, even as consumers tighten the purse strings, with a recession likely on the horizon.

Remarkably, Disney+ subscriber growth remained robust in the last quarter, with 7.8 million global subscriber adds, as Netflix shed 200,000. Still, investors seem to think Disney+ is bound to suffer the same fate as Netflix at some point down the road. Indeed, video streaming is no longer worth the same premium multiple it had commanded just over a year ago.

With so much negativity baked into Disney stock, it’s hard to be anything but bullish. Many of the negative headlines are temporary and are clouding the solid long-term fundamentals. The long-term foundation will allow Disney to return to a concrete footing once the tides inevitably turn back in its favor.

Can Disney+ Dethrone Netflix?

Second-quarter Disney+ subscriber additions were a lone bright spot on an otherwise mixed bag of numbers. Chapek and company seem to be putting their foot on the gas, with direct-to-consumer (DTC) operating losses increasing. Undoubtedly, steeper losses and rampant spending are viewed as a negative at a time like this. Streaming used to be the solution to Disney’s COVID woes. Now, investors may view it as more of a money sink, with rates rising.

With a massive $32 billion content budget for fiscal 2022, Disney+ is about to become a lot better. Even for a $192 billion company, the magnitude of spending is jarring. Still, putting the foot on the gas may be the right move, as the flood gates open on Netflix’s subscriber base.

With so many great binge-worthy titles coming out of the Disney+ pipeline, it’s hard not to get excited about the platform’s growth prospects. While the best growth days of Disney+ may be in the rear-view mirror, I think the platform could prove growthiest of all video-streamers over the next three years. Disney is spending money in the right places, and in due time, it will likely be rewarded accordingly.

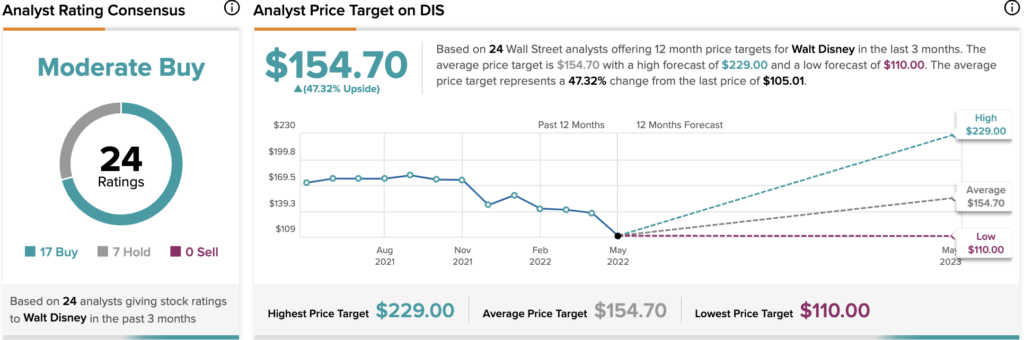

Wall Street’s Take

According to TipRanks’ analyst rating consensus, DIS stock comes in as a Moderate Buy. Out of 18 analyst ratings, there are 15 Buy recommendations, and 10 Hold recommendations.

The average Disney price target is $154.70, implying an upside of 47.32%, as of 10:07am EST., on Thursday. Analyst price targets range from a low of $110 per share to a high of $229.

The Bottom Line on Disney Stock

Disney stock has been easy to give up on, with so much negative momentum behind it. Still, the second half is unlikely to be as ugly as the year’s first half.

The parks business could get a jolt for the summer as restrictions lift globally. Further, I feel that investors are discounting the growth potential of Disney+, which has fallen in sympathy with Netflix of late.

Chapek may be right to cancel the dividend and funnel considerable sums into the DTC segment. At the end of the day, streaming is a fiercely competitive environment, and subscribers will gravitate toward the firms that provide the content.

Read full Disclosure