Buoyed by a strong earnings report and optimistic forecasts earlier in the month, major air carrier Delta Air Lines (NYSE:DAL) appears to be poised to continue to benefit from renewed business in the commercial air travel space. The airline’s premium services offer a higher margin than other products, and it also stands to achieve strong loyalty-related sales while working to pay down pandemic debt.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

All of these factors have prompted many analysts on Wall Street to bump up their price targets for DAL shares and name the stock a Buy. I agree with this bullish assessment and believe that Delta offers investors many reasons to get excited. We’ll take a closer look at several of them below.

DAL’s Earnings Momentum and Outlook

Early in April, Delta reported adjusted earnings per share (EPS) of $0.45 on operating revenue of $12.6 billion for the first quarter of the year, a 6% increase over the prior-year quarter. Average analyst predictions for adjusted EPS for the period were $0.35, meaning that Delta significantly outperformed expectations.

Perhaps even more importantly, the company said that strong travel demand anticipated for future months could drive total revenue growth for the current quarter to 5-7% over what it was last year. This forecast—as well as the company’s full-year EPS outlook of $6 to $7—was also ahead of many analysts’ expectations.

Sunny Skies Ahead

What is behind Delta’s lofty forecasts for the coming months? The company pointed in its earnings report to a series of travel demand data points, including a 3% year-over-year improvement in domestic unit revenue and a whopping 14% increase in demand from corporate flyers. International travel has also bounced back from a pandemic-related low, as Delta noted 12% higher revenue in this area compared to last year’s March quarter.

Strong travel demand is a major factor in the success of Delta’s business, but it’s not the only one. The company must balance the total revenue it earns per available seat mile (an acronym known as TRASM) against the costs per available seat mile. TRASM for the most recent quarter was only up 1% year-over-year.

However, the cost per available seat mile actually declined by 6%, alongside the cost of airplane fuel. In total, these shifts helped increase Delta’s overall profitability.

Capturing the Premium Market

With a surge in corporate travel demand comes Delta’s plans to increase its premium-tier offerings. These include new technology available in some of its aircraft, luxury lounges in airports, and co-branded credit cards, including benefits.

The push toward premium may help Delta further differentiate itself from competitors, particularly at a time in which many consumers view airline “junk fees” (fees for extras such as seat selection) negatively. These services are catered toward business travelers as well as members of Delta’s SkyMiles rewards program and generally have a higher margin than similar services offered at a lower tier.

Delta says it will likely spend $5 billion annually to improve the travel experience for SkyMiles customers. This significant upfront investment may pay off, though, as the company continues to address concerns from customers upset by changes to the rewards program announced last September. These changes were subsequently revised following customer backlash.

Addressing Delta’s Pandemic-Related Debt

Like most airlines, Delta took on significant new debt as it dramatically curtailed operations during the early stages of COVID-19. However, the airline now finds itself in an enviable position relative to rivals. Delta CEO Ed Bastian has said he believes his firm will be the only profitable major airline during the first quarter.

With an estimated $3 billion to $4 billion in free cash flow for 2024, Delta could be well-positioned to reduce its debt levels. At a time in which some peers are still struggling to achieve profitability, this could allow Delta to claim an operational advantage lasting well into the future.

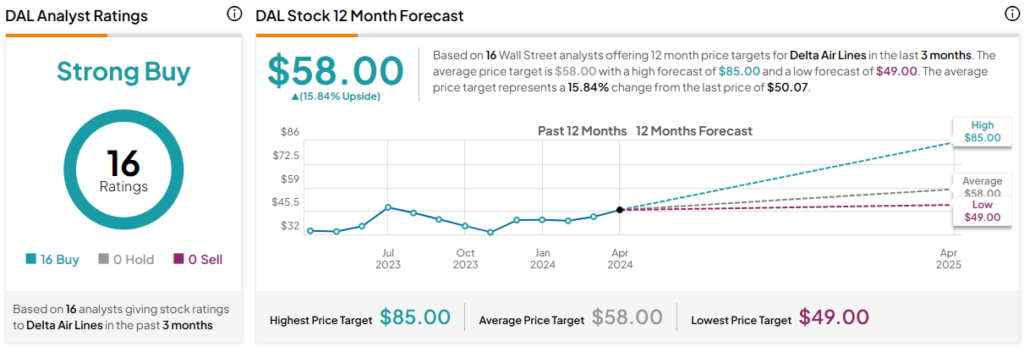

Is DAL Stock a Buy, According to Analysts?

Shares of DAL have climbed by 45% in the last year and have risen steadily since late October. Still, despite these significant gains, analysts believe there is still upside potential. The average DAL stock price target of $58.00 represents 15.8% upside potential. DAL stock is also rated as a Strong Buy across Wall Street based on 16 Buy ratings, zero holds, and zero sells.

The Takeaway: Delta Still Has Room to Soar

Coming off an earnings report for the first quarter that beat expectations in multiple ways, Delta still has room to grow. The company’s newly-raised outlooks for second-quarter and full-year EPS show that it has the potential to capitalize on surging travel demand. Additionally, its strategy to showcase high-margin premium services while working to ease the minds of its SkyMiles members could help accelerate growth.