One of the worst-hit publicly traded companies during the COVID-19 crisis was Carnival (NYSE:CCL). Symbolizing the poster child of the pandemic, Carnival and the wider cruise ship industry could do nothing more than wait for the normalization of mobility. To reach this point sooner, the Washington machinery implemented a series of fiscal and monetary stimulus programs. Unfortunately, it’s these very efforts that now threaten to sink CCL stock. As a result, I am bearish.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

When the SARS-Cov-2 virus ceased to be the exclusive domain of the foreign and exotic and instead rapidly proliferated across the globe, Carnival could not have asked for a worse headwind. In 2019, the company generated revenue of $20.8 billion with a net income of $2.99 billion. Fast forward one year later and revenue fell to an alarming $5.59 billion. Worse yet, the cruise ship operator incurred a net loss of over $10 billion.

With people understandably concerned about spending time in close quarters with complete strangers, many consumers chose to shelter in place. Unfortunately, then, CCL stock could only benefit from speculators anticipating a recovery in the cruise liner industry. Until the actual recovery occurred, Carnival could not begin the slow and painful process of fiscal restoration.

Fortunately, after a hard-fought battle, local, state, and federal government agencies began relaxing COVID-related restrictions. In so doing, CCL stock fundamentally benefitted from revenge travel and the pent-up demand for real experiences. However, the narrative for Carnival was short-lived.

To reach the economic summit, the Federal Reserve had to make a deal with the devil, and the devil wants his end of the bargain now.

Monetary Policy Doomed CCL Stock

As the COVID-19 crisis began to proliferate, the Fed had little choice but to implement a dovish monetary policy; that is, it sought to introduce liquidity into the system via bond buybacks. In doing so, the money supply grew along with the central bank’s balance sheet. While few were thinking about it at the time, it was at this point when CCL stock slipped into the path of downward inevitability. Heading into 2022, consumers began realizing very quickly that inflation escalated to a worrying level.

With the money supply expanded to an unprecedented degree, the Fed now had to scale back its earlier excesses. This meant shrinking the balance sheet and in so doing, reducing liquidity in the system.

However, the current source of anxiety now is whether the Fed might accidentally push the needle too far. As Reuters reported earlier this month, liquidity in the bond market deteriorated partly because of the Fed’s hawkish pivot. Left unchecked, the monetary trajectory could lead to a recession.

Now, the problem for CCL stock is that whether the issue centers on too much liquidity (inflation) or not enough (deflation), consumers either way will suffer. Under the former framework, people will see the purchasing power of their dollars erode. However, under the latter framework, people may end up losing their jobs due to a broader deceleration of commercial activity.

For CCL stock, all roads lead to fiscal perdition. Indeed, while Carnival is presently on its recovery trek, its trailing-12-month revenue stands at only $9.6 billion. That’s less than half of what the company posted in 2019. Therefore, the cruise ship industry needs a substantial boost which sadly doesn’t appear to be on the horizon.

Is Carnival Stock a Buy Sell or Hold?

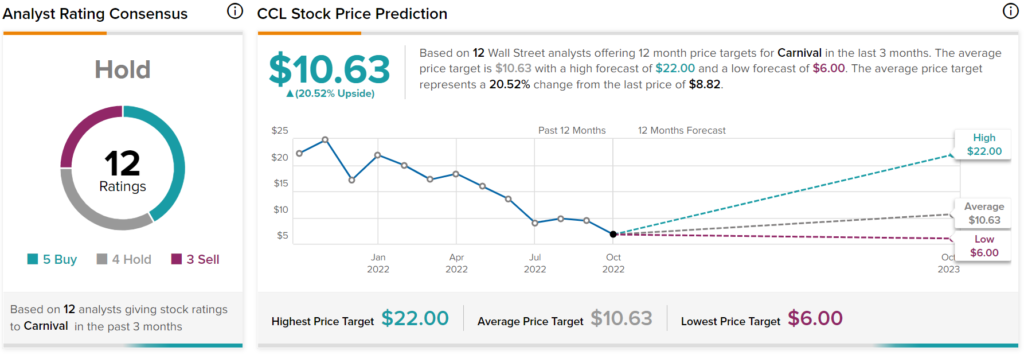

Turning to Wall Street, Carnival stock has a Hold consensus rating based on five Buys, four Holds, and three Sells assigned in the past three months. The average CCL price target is $10.63, implying 20.52% upside potential.

Travel Stats Don’t Augur Well for Carnival Stock

Contrarian investors might have the urge to bet on CCL stock. However, data upon data reveals that travel sentiment appears to be waning. For instance, according to the U.S. Bureau of Labor Statistics, the producer price index for the cruise and tour bookings industry continues to rate below the level seen in March 2020. Of course, this represents a troubling prospect as March 2020 data is itself well below levels seen throughout much of 2019.

Next, investors should consider vehicle miles traveled, which has generally been on the decline since February 2022. While not directly related to cruise ship stats, the reduction of people driving on U.S. roadways indicates a systemic concern. Simply, people are just not interested (or capable) of traveling.

Finally, market participants should note revenue passenger miles for U.S.-based air carriers. Since April of this year, air travel sentiment appears to have peaked, subsequently declining into June. Again, it’s not directly related to cruise ships. However, across various modes of transportation, the data sources present a consensus assessment: mobility trends declined.

Thus, investors must recognize harsh realities. Carnival’s total addressable market is shrinking, which does not augur well for CCL stock.