Not to be outdone by its outperforming mega-cap peers, Facebook (FB) delivered the goods last week, beating the estimates in its 2Q20 earnings report. The buoyant report sent shares soaring by 8% in Friday’s session and the social media behemoth saw out the week notching a new all-time high.

In the coronavirus ravaged quarter, Facebook reported revenue of $18.7 billion, up by 11% year-over-year and handily beating Wall Street’s call for $17.4 billion.

Facebook’s operating income jumped year-over-year by 29% to $6 billion, while EPS came in at $1.80. beating the analysts call for $1.39.

Both Facebook’s daily and monthly active users increased by 12%. DAUs grew to 1.8 billion vs consensus calls for 1.75 billion, while MAUs of 2.7 billion beat the 2.63 billion estimate.

Despite the coronavirus’s impact on ad spend, ad revenues, which make up the bulk of Facebook’s income, rose 10% to $18.32 billion.

Facebook said it expects to feel the impact of the ad boycott on its platform in Q3 but the results so far indicate a minimal impact, with ad revenue in the first 3 weeks of July up by 10%, too, matching the previous quarter’s figure.

All in all, Facebook beat the estimates despite posting its slowest revenue growth since its 2012 IPO. Although Monness analyst Brain White expects Facebook to come up against several challenges over the coming quarters, the 5-star analyst expects the social media giant to navigate its way successfully through the headwinds.

“Clearly,” said White, “Facebook faces increased regulation in the future and still runs the risk of being broken up. Given the expansion of this COVID-19 crisis across a larger swath of the U.S. and a flurry of ad boycotts rippling across the platform, we expect Facebook to remain challenged this year… We anticipate Facebook will continue to struggle with the vicissitudes of digital ad spending, more boycotts, antitrust investigations and a steady flow of negative media headlines; however, we believe the stock remains inexpensive and Facebook has an opportunity to emerge from this crisis stronger.”

Therefore, White reiterated a Buy rating on Facebook, while increaseing the price target from $230 to $290. Investors could be taking home a 15% gain, should White’s thesis play out over the next 12 months. (To watch White’s track record, click here)

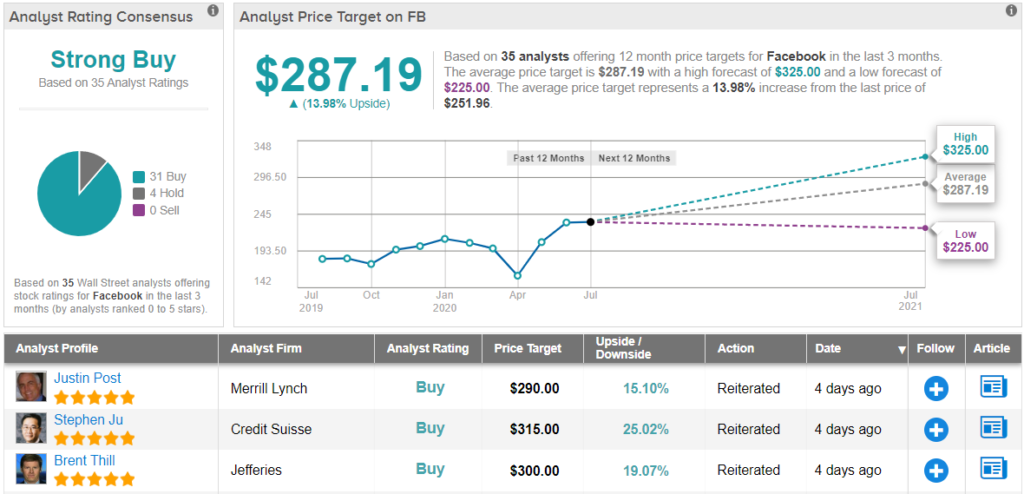

Overall, Facebook remains a firm favorite on Wall Street. Backed by 31 Buys and 4 Holds, FB has a Strong Buy consensus rating. The average price target hits $287.19 and implies possible upside of 14%. (See Facebook stock analysis on TipRanks)