President Joe Biden’s decision to pardon all those doing time for simple marijuana possession sent shockwaves through the beleaguered cannabis industry last week.

Stocks across the sector soared on the news, which came as timely relief for a segment beaten to a pulp after hope of any federal legislative progress had mostly evaporated since the Biden administration came in to power at the start of last year. Investors had hoped that Biden’s win along with the Dems taking control of both the House and Senate, would see change take place, but that hasn’t happened yet.

“Yet” could be the key word here. Biden also said he was pushing for a review by the Attorney General and Secretary of the Department of Health and Human Services which could take cannabis off the list of Schedule I drugs which currently classifies weed in the same category as heroin and fentanyl.

While that process will take a while, there could be more immediate implications, notes Cantor’s cannabis expert Pablo Zuanic.

“We believe the President’s actions will facilitate the negotiations between Senate Democrats and Republicans to pass SAFE Plus in the lame duck,” Zuanic said. And that could provide a real catalyst for U.S. MSOs (multistate operators) in the shape of possible uplistings (currently U.S. based cannabis stocks are unable to trade on the main exchanges) and better access to banking services.

So, potentially exciting times ahead for the cannabis industry. With this in mind, let’s take a look at two leading cannabis names which could benefit from this new paradigm. According to the TipRanks database, both are considered Strong Buys by the analyst consensus. Let’s see why the experts find these stocks so appealing right now.

Curaleaf Holdings, Inc. (CURLF)

We’ll start with the U.S. cannabis industry’s largest company by market cap; Cuarleaf has a footprint in 21 states, where it operates via both retail and wholesale channels. The company boasts 144 dispensaries and 29 cultivation sites, and targets heavily populated states such as Arizona, Florida, Illinois, New Jersey, New York, Pennsylvania and its home state of Massachusetts.

Curaleaf is also the largest revenue generator amongst cannabis companies, a position it held on to following the Q2 report – released in August. Revenue reached a record $337.5 million, amounting to an 8.1% year-over-year increase. The company delivered adjusted EBITDA of $86 Million, representing a sequential uptick of 18% and 2% y/y growth.

The results were boosted by the launch of AU (adult use) in New Jersey and a growing focus on vertical sales, with CURLF products making up 65% of retail revenue. These helped counter higher inflationary costs and pricing pressure seen elsewhere.

One segment which remains relatively small but which the company thinks could provide some outsized growth over the coming years is that of the international market—Europe in particular. International revenue rose by 50% y/y, and Curaleaf thinks its U.S. experience will help it make headway in countries which will legalize medical and AU.

Given the potential here, and despite anticipating fierce competition, Seaport analyst Sonny Randhawa expects European exposure to be a “bigger contributor to upward estimate revisions in coming quarters.”

And like the impact New Jersey has had, with other markets opening up, the future bodes well for the MSO.

“With CURLF’s dominant position in NY and CT, the start of AU sales could have a similar impact on wholesale revenues in coming quarters,” Randhawa said. “We believe CURLF’s depth and scale across most of the attractive US cannabis markets and burgeoning international expansion makes it one of the best ways to play the cannabis sector.”

Accordingly, Randhawa rates CURLF shares a Buy, backed by a $9 price target, which makes room for 12-month growth of 55%. (To watch Randhawa’s track record, click here)

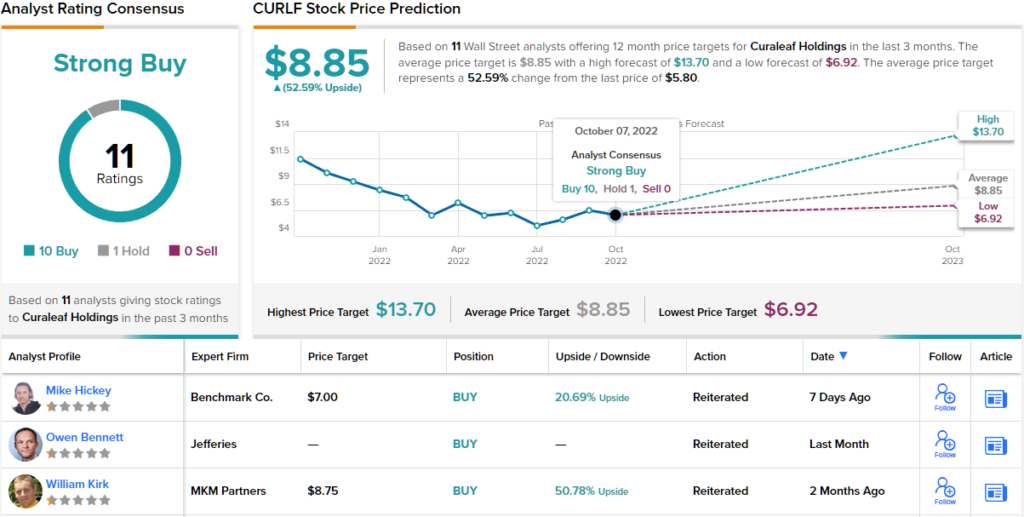

Overall, 11 analysts have chimed in with reviews of this cannabis stock over the past 3 months, and barring one skeptic, all 10 others are positive, making the consensus view a Strong Buy. At $8.85, the average price target suggests shares will climb ~53% higher over the coming months. (See Curaleaf stock forecast on TipRanks)

Cresco Labs (CRLBF)

Next up is another major player in the U.S. cannabis industry. Cresco Labs has a presence in 10 states, where it has 21 production facilities, and 53 owned dispensaries. The Chicago, Illinois-based company’s portfolio boasts some of the most well-known cannabis brands such as Cresco, Remedi and Mindy’s edibles which were developed by Mindy Segal, a James Beard Award-winning chef.

The company has prioritized its wholesale channel and held on to its position as the country’s top seller of branded cannabis products in Q2. Wholesale revenue reached $95 million, out of a total of $218.22 million, amounting to a 1.8% year-over-year uptick. Adjusted EBITDA increased by 11% from the same period a year ago to $51 million.

While MSOs with a presence in the Garden State saw the benefit of New Jersey adult use open up in Q2, with no operations in the state, Cresco was not privy to this tailwind. However, that could change shortly. Cresco is merging with fellow MSO, the smaller Columbia Care, which does have access to NJ. If all goes according to plan, the transaction should close before the end of the year.

The new look Cresco will be a formidable force, says Ladenburg analyst Glenn G. Mattson.

“The combined entity will cover 180 million people and serve a market that is expected to grow to $31 billion by 2025,” the 5-star analyst explained. “Importantly the acquisition gives Cresco access to a number of markets poised to convert to adult rec over the next 18-36 months, including NJ, VA, WV, MD, as well as other key markets like CO. This coupled with an existing presence in soon to covert markets like PA and NY provide a long series of tailwinds to drive growth in 2023 and beyond. In the end, we think that combining Cresco’s solid operational performance with Columbia Care’s broader footprint will make for a powerful combination.”

Mattson is evidently bullish on Cresco’s prospects; along with a Buy rating, the analyst’s $9 price target implies 12-month share appreciation of 183%. (To watch Mattson’s track record, click here)

This is another cannabis stock with a Strong Buy consensus rating, based on 7 Buys vs. 2 Holds. The forecast calls for one-year gains of ~155%, considering the average target currently stands at $8.10. (See Cresco Labs stock forecast on TipRanks)

To find good ideas for cannabis stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.