We’re in a turbulent economic environment right now, and the headwinds are piling together, putting up an ominous cloud on the financial horizon. Billionaire Leon Cooperman, the CEO of Omega Advisors, has noted the coming storm, and sees the commercial real estate market as the eye of the developing hurricane.

In Cooperman’s view, several factors are about to hit hard at commercial real estate: first, declining occupancy rates; second, rising interest rates; and third, reduced credit access in a tighter monetary regime. These three will, together, exacerbate a fourth: the impending rollover of commercial real estate debt, that was originally financed when interest rates were low. Added to this, small- to mid-sized banks make up some 80% of the commercial real estate lending market, and if that market crashes, we could see a rash of bank failures.

While Cooperman sees a downturn ahead, he also sees plenty of sound stocks to use for defensive portfolio positions. In his portfolio, there are names that over the past year have outperformed the market by a wide margin. By holding on to them, Cooperman evidently thinks that while bad times are coming, these stocks will keep on delivering.

With this in mind, we dipped into the TipRanks database and pulled up the details on two Cooperman-owned stocks. Do the Street’s cadre of stock experts also think these are worth picking up right now? Let’s take a closer look.

SunOpta Inc. (STKL)

The first Cooperman pick we’re looking at is SunOpta, a food and beverage company specializing in the health food niche. SunOpta’s product range includes a variety of plant-based snacks, nutritional additives, and beverages, produced and marketed in-house for distribution through third-party retailers and food service distributors. The company caters to a wide range of tastes in the health-food market, with lines of fruit products; oat-, soy-, and almond milk drinks; broths and stocks; and roasted seed snacks.

SunOpta’s products can be found under several brand names, including Sunrise Growers for fruit products, Dream and West Life for plant-based milk replacements, and Sown for plant-based, organic oat creamers, and other non-dairy milk substitutes. SunOpta also distributes its products under its own name. The company was founded in Canada, is currently based in Minnesota, and has been in business since 1973.

On the financial side, SunOpta’s posted a bottom line profit in its last reported quarter, 4Q22. Prior to the earnings release, forecasters had predicted a 1-cent EPS loss; the company saw a non-GAAP EPS profit of 2 cents, however, which easily beat the expectations. At the top line, the company reported revenues of $221.3 million, up 8.4% year-over-year. The revenue growth was driven by a 10.8% increase in plant-based foods and beverages. A 9.8% increase in pricing also contributed to the boost in revenues.

During the fourth quarter, SunOpta began operating a new plant-based beverage production facility, a $125 million factory located in Midlothian, Texas. The facility produces SunOpta’s full line-up of plant-based milks and creamers, along with various other beverages, including the company’s teas. Although the company reported $4.6 million in start-up costs for the factory in the quarter, SunOpta’s quarterly gross profit still grew by over 56%.

This background helps put Cooperman’s stance on STKL into perspective. He currently holds 2 million shares of the stock, which has shown a 42% appreciation over the past 12 months – definitely a gain that will provide defensive protection for any portfolio. Cooperman’s holding in SunOpta is currently valued at $15.24 million.

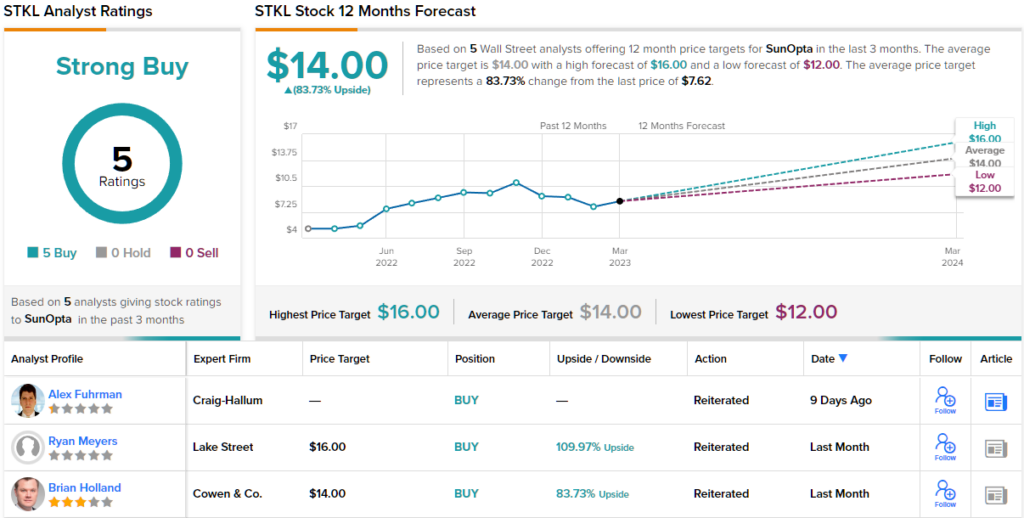

This fast-growing stock hasn’t just caught the attention of Leon Cooperman. Craig-Hallum analyst Alex Fuhrman is also impressed with it, noting that the company’s stable earnings make it a good defensive stock in times of recession.

“We believe SunOpta is well positioned to weather a recession. Food tends to be something that consumers don’t cut back on during recessions, and STKL’s plant-based business is split roughly 50/50 between the grocery and food service channels. While consumers would likely buy fewer almond milk lattes from Starbucks in a recession, this would at least partially be made up for in the grocery channel. A recession could potentially slow the rate of share gains for plant-based milks given their higher costs, however the trend away from dairy is unlikely to ever reverse given compelling environmental benefits of switching,” Fuhrman opined.

Furhman’s bullish outlook backs his Buy rating on the stock, and his $18 price target implies a robust upside of 136% for the next 12 months. (To review Furhman’s track record, click here)

Overall, SunOpta has attracted 5 recent analyst reviews, and they are all positive, for a unanimous Strong Buy consensus rating. The stock is currently trading at $7.74 and its $14 average price target suggests ~84% gain from that level. (See SunOpta stock forecast)

Las Vegas Sands (LVS)

The next Cooperman-endorsed stock is Las Vegas Sands, a casino and resort company based in Las Vegas, Nevada and operating several properties in East Asia, in Singapore and Macao. While the company’s Singapore resort property is its largest, Macao is home to five Vegas Sands resorts.

The company boasts a total of 14,697 guest suites across all six properties, as well as more than 7.9 million square feet of gaming and retail space, and another 3.669 million square feet of conference and meeting space.

While Las Vegas Sands has a pretty impressive foundation, the company’s 4Q22 financial results – the last quarter reported – came in below expectations. The revenue figure of $1.12 billion was up more than 10% year-over-year – but was also $60 million below the forecast. At the bottom line, the company had a non-GAAP EPS loss of 19 cents, 10 cents worse than had been expected.

The miss doesn’t seem to have phased investors. Over the past 12 months, LVS has registered share price growth of 52%.

Cooperman must think that LVS stock will keep on outperforming. The billionaire is currently holding 723,300 shares of LVS. This gives him a stake of $41.70 million in the company.

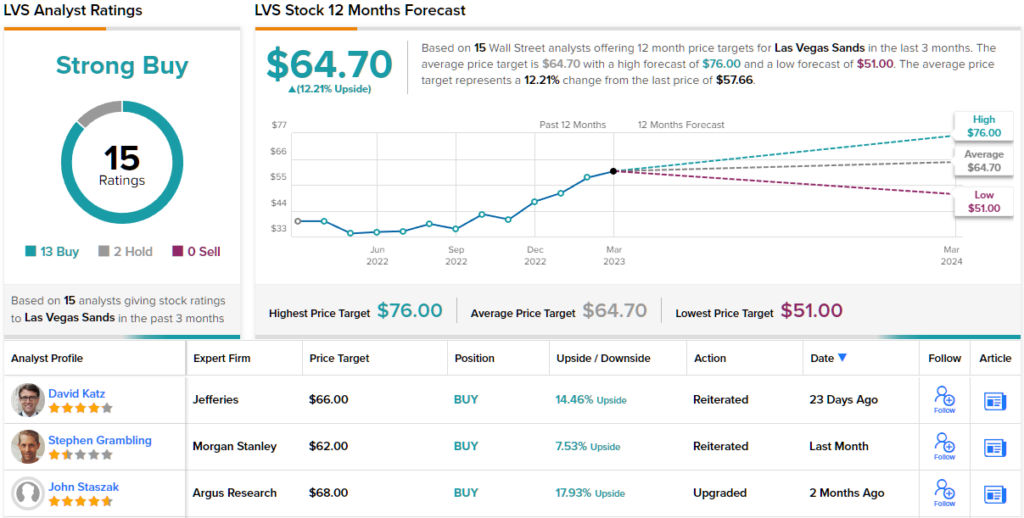

5-star analyst Joseph Greff, of JPMorgan, has been following LVS, and like Cooperman, he’s impressed with the potential here.

“We continue to believe that LVS shares represent an appealing China re-opening play given improving travel and spend trends since the market has become more accessible and recent trends reflect pent up demand that is not dissimilar to what U.S gaming and leisure travel markets experienced earlier in their respective recovery…. While LVS and the Macau stocks have meaningfully outperformed the SPX over the last 3 months, we still see attractive upside given the early stages of recovery in Macau,” Greff opined.

Greff quantifies his bullish stance with an Overweight (i.e. Buy) rating, and his price target, currently set at $68, indicates potential for an 18% one-year upside. (To watch Greff’s track record, click here)

All in all, 15 analysts have chimed in on Las Vegas Sands, and their reviews include 13 Buys and 2 Holds, for a Strong Buy consensus rating. (See LVS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.