BigCommerce Holdings (BIGC) is an e-commerce platform. Its software allows individuals and businesses to create online stores.

The company powers both its customers’ branded e-commerce stores and their cross-channel connections to popular online marketplaces, social networks, and offline point-of-sale systems.

BIGC offers a great product that is highly competitive with industry leaders such as Shopify (SHOP). However, although the company is seeing impressive growth, it is currently unprofitable. As a result, we are neutral on the stock.

Recent Earnings Results

BigCommerce recently reported earnings, and investors seemed to like what they saw. The stock rallied the following day on the news. Earnings per share were in line with expectations, but revenue beat by $2.3 million, coming in at $66.1 million.

This equates to a year-over-year growth rate of 42%. Most importantly, subscription revenue made up $48 million of the quarter’s revenue, an increase of 50% compared to the first quarter of 2021. Since subscription revenue is recurring and predictable, it’s a very good sign when it outpaces overall revenue growth and makes up more than half of sales.

However, this growth was not cheap. In fact, BIGC saw its losses widen year-over-year from -$0.04 to -$0.18 earnings per share. It is also worth mentioning that the share count increased from 69.8 million to 72.5 million. This means that shareholders were diluted by approximately 3.9%, in addition to the larger losses.

This can mainly be attributed to two factors: a lower gross profit margin and higher marketing spending. The company’s gross profit margin decreased quite considerably, from 80% to 74%. This might be the result of increased competition, as Shopify also saw a similar decrease in its gross profit margin.

However, the most troubling thing is the fact that the growth in marketing spending is outpacing the growth in revenue. The company needed to spend roughly 54.4% more on marketing in order to achieve revenue growth of 42%.

This has also led to the marketing expense as a percentage of revenue becoming larger. In the first quarter of 2021, it was 44.6% of revenue compared to the 48.6% in the most recent quarter.

We believe investors need to monitor both its gross profit margin and marketing spending going forward to see if these trends improve or continue.

The Rule of 40

A common metric used to measure the effectiveness of Software-as-a-Service (SaaS) companies is the rule of 40, which is calculated as revenue growth plus free cash flow margin.

The way we like to think about this metric is that if the sum of the two numbers is above 40, then a company is growing in an efficient way. In contrast, a sum that is below 40 indicates the opposite.

In BIGC’s case, the sum of its revenue growth and free cash flow margin for the last 12 months is equal to 21.8, which is way below 40. This further adds to the argument that the company’s growth strategy is expensive and potentially suboptimal.

Website Traffic Analysis

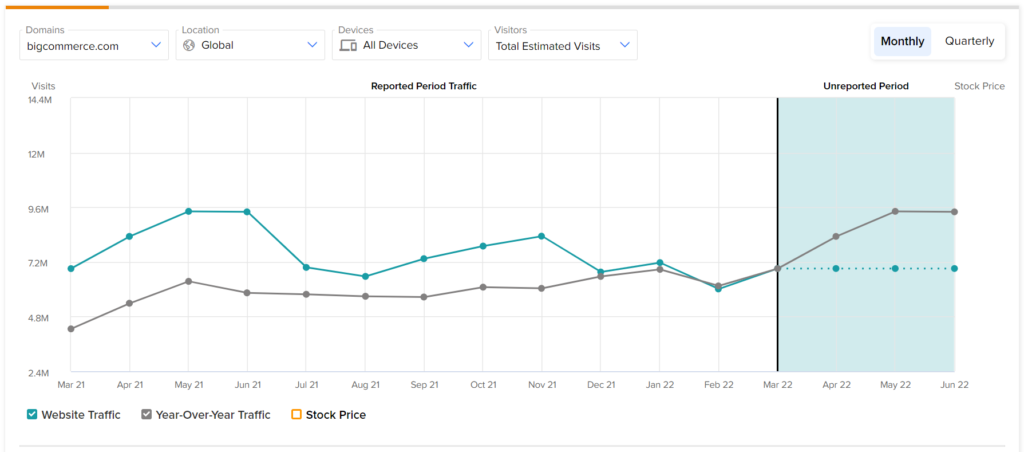

As a software company, customers and potential customers need to visit the website in order to use the service. As a result, monitoring BigCommerce’s website traffic may be a good way to gauge the company’s performance.

By looking at the picture above, we notice a couple of interesting trends that are consistent with the most recent earnings report. The first trend is that total estimated visits were slightly higher year-over-year, which is consistent with the higher revenue growth.

Interestingly, website traffic has been trending downwards since March 2021. This is consistent with the fact that marketing expenses have increased faster than revenue growth. As the cost to acquire new users increases, the effectiveness of each dollar spent decreases. Ultimately, this leads to less traffic.

Risks

To measure BIGC’s risk, we checked if financial leverage is an issue. The company is currently not profitable. Thus, it is unable to cover its interest expenses with its operating income.

Nonetheless, debt doesn’t appear to be an issue because interest payments totaled just $1.5 million in the last 12 months compared to BIGC’s cash pile of $376 million.

However, there are other risks associated with the company. According to Tipranks’ Risk Analysis, BigCommerce has disclosed 63 risks. The highest amount of risk came from the Finance & Corporate category.

This is more than double the S&P 500’s average of 31 risks, making the company relatively riskier than average.

Wall Street’s Take

Turning to Wall Street, BigCommerce has a Moderate Buy consensus rating based on eight Buys, seven Holds, and zero Sells assigned in the past three months. The average BigCommerce price target of $30.31 implies 48.2% upside potential.

Final Thoughts

BigCommerce offers a great product that is mostly tailored to large enterprise companies. In terms of the quality of its platform, it is very competitive, especially when it comes to high-volume product sales.

Unfortunately, it operates in a very competitive industry, which is evident when looking at its widening losses. As a result, we are neutral on the stock.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure