Thanks to the randomness of timing, embattled retailer Big Lots (NYSE:BIG) might not seem like such a bad bet, given its recent upward price swing, going from a low of $3.47 last week to over $4 now. It’s quite possible that in the near term, speculators could be looking for a quick profit. However, over the long run, it’s difficult to see a circumstance where the discount retail chain recovers. I am bearish on BIG stock because of its spiraling business.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

A Competitor Sounds the Alarm for BIG Stock

Usually, bad news directly impacting a company is responsible for its volatility. Certainly, Big Lots offers plenty to make all but the most intrepid speculators sweat. For example, year-to-date BIG stock has cratered 72%. However, it was a competitor that perhaps broadcasted the loudest warning.

Recently, TipRanks reporter Radhika Saraogi stated that Walmart (NYSE:WMT) succumbed to red ink following its third-quarter earnings disclosure and, more importantly, its Q4 sales expectations. On paper, the Q3 results were fairly solid. Adjusted earnings per share landed at $1.53, beating analysts’ target of $1.52. On the top line, sales of $160.8 billion exceeded the consensus view of $159.72 billion.

However, it was the current-quarter guidance that sent jitters. Management disclosed expectations of weak consumer spending for the upcoming holiday season. It also revealed a lower-than-expected Fiscal 2024 EPS forecast. Subsequently, WMT tanked as investors digested the news.

Still, in the long run, Walmart should be fine. It’s a massive big-box retailer, a one-stop shop for consumers across the income spectrum. Unfortunately, the same confidence cannot be applied to BIG stock.

If a powerhouse like Walmart anticipates a weak holiday season, that doesn’t speak highly about Big Lots. Per TipRanks data, after Q4 2021, the embattled retailer has posted consecutive losses per share. Unless it rights the ship quickly, more pain could be on the way.

Fundamental Cracks are Starting to Appear

Looking at the framework for BIG stock from a fundamental perspective, it almost seems as if the enterprise is fighting against a downward spiral. Amid tough pressure points like stubbornly-high inflation and fierce retail competition, a less-equipped firm like Big Lots sits at a disadvantage.

To be sure, BIG stock has gained in the past week. Much of this may stem from contrarian bullish activity in the options market. Specifically, many pessimists have sold calls against BIG, betting that it won’t rise above $5 by certain expiration dates. However, as the security marches higher toward this level, the bears may be forced to cover their position.

Therefore, it’s important to remember that selling BIG stock now may come at the penalty of an opportunity cost. Nevertheless, the fundamentals seem exceedingly ugly. In particular, Big Lots’ gross profit margin hit 41.57% in its second quarter of Fiscal 2020. Since then, however, its gross margin has tumbled to 33% in Q2 2023.

In contrast, Walmart – while printing a lower overall gross margin of 24.6% as of the latest reading – has seen this metric stabilize over several years. This consistency affords confidence for investors. On the other hand, the lack of consistency, along with a recent deterioration, casts a dark cloud over BIG stock.

Financials Seem to Indicate a Value Trap

Now, at first glance, BIG stock might seem like a bargain to novice investors. After all, the security trades hands at a subterranean trailing-year revenue multiple of 0.02x. In contrast, the specialty retail sector’s average price-to-sales ratio stands at 0.68x. Seems like a killer deal, right?

Well, the problem is that because Big Lots’ annual revenue tally has been declining since Fiscal Year 2021, the low multiple is deceptive. In this case, it may be better to seek a higher sales premium but with a superior probability of growth. At the very least, investors should consider enterprises that enjoy stable revenue trajectories, not negative ones.

Is BIG Stock a Buy, According to Analysts?

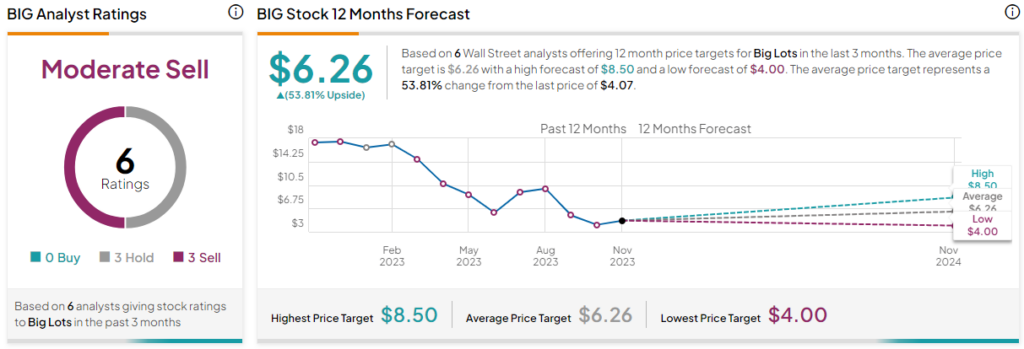

Turning to Wall Street, BIG stock has a Moderate Sell consensus rating based on zero Buys, three Holds, and three Sell ratings. The average BIG stock price target is $6.26, implying 53.8% upside potential.

Takeaway: BIG Stock Can’t Run from Its Fundamentals Indefinitely

In recent sessions, BIG stock popped higher, likely due to options market speculation. Because of the power of such speculation, it should be respected. At the same time, the fundamentals arguably should be respected more. Here, the Big Lots narrative is suspect because of its contracting revenue and gross margin, along with other headwinds.