Last week closed with a sudden market rally after October’s inflation data was better-than-anticipated, but this week’s trading has been unpredictable. There’s a level of uncertainty here; investors want to buy – but inflation remains high, and interest rates are still rising, making for a tough economic environment.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

But it’s been tough all year long, and that hasn’t stopped legendary billionaire investor Warren Buffett from taking his Berkshire Hathaway firm on a months-long stock shopping jaunt. Buffett has been buying up stocks despite inflation, and it’s worth taking a moment to look at just what he’s seeking when he picks a stock.

His key point, in nearly every purchase, is to buy into a company that makes stuff. This has been a long-standing policy of his, but it’s ever more important during an inflationary period. Buffett believes that investors should buy into firms that make products which customers will want or need to buy, no matter the price. These are the companies that will succeed even in an inflationary regime. As he puts it, if customers like or want the products, “It doesn’t make any difference what’s happened to the price level.”

So let’s check in with Berkshire Hathaway. According to the firm’s most recent regulatory filings, Buffett has bought heavily into two stocks that at first glance are feeling the pressure. We ran them through the TipRanks database to see whether Wall Street’s cadre of experts agree with his selections. Let’s take a look at the results.

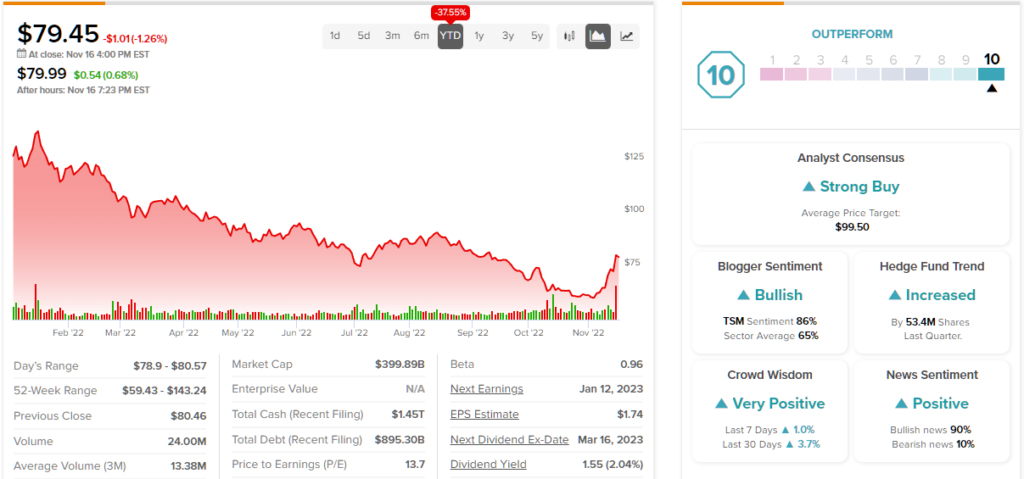

Taiwan Semiconductor Manufacturing (TSM)

We’ll start with Taiwan Semiconductor, a major firm in one of Taiwan’s major industries. The island country is one of the world’s largest producers of semiconductor chips, and TSM is the largest of its chip companies – and one of the largest chip makers in the world. TSM doesn’t just product chips designed in-house; it is also the global leader in contract chip production, acting as the foundry for other firms. The company boasts a market cap of more than $400 billion, even after seeing its share price drop 33% this year.

Semiconductor chips are big business, and TSM saw $56.8 billion in total revenue last year. So far this year, the company has seen year-over-year revenue growth in each quarter; the most recent report, for 3Q22, showed $20.2 billion at the top line, up 36% y/y. On earnings, the company reported $1.79 per ADR unit, up from the $1.08 billion in 3Q21, for 66% increase. Furthermore, the company is guiding toward a 4Q22 top line between $19.9 billion and $20.7 billion. Looking beyond Q4, however, TSMC expects customer inventory drawdowns will weigh on 1H23 results.

TSM has committed itself to a strong program of cash return to investors, and pays out a regular quarterly dividend. The company has not missed a payment since 2004, and boasts that it has never reduced its quarterly payment. Taking into account currency exchange rates between Taiwan and US dollars, the dividend per US share does sometimes fluctuate. The last payment was declared at 44 cents per share (US currency); at this rate, it annualizes to 2.2%.

This company combines two attributes that Warren Buffett has always sought after – a necessary product and a reliable dividend. In his Q3 filings, Buffett revealed a massive buy-in to TSM, of over 60 million shares. This holding is now worth $4.77 billion at current share price.

Needham analyst Charles Shi agrees that TSM is a stock to buy, as it offers “a positive risk/reward.”

While a deep retrenchment is expected in early 2023, Shi believes the company will find support in the form of better pricing. He writes: “We estimate TSMC’s average wafer price will grow by 23% YoY in 2023, including 6% pricing increases that have been executed across the board, with the rest of the growth coming from the mix shift to advanced nodes, driven by the 5nm ramp of all non-Apple Tier-1 customers and the 3nm ramp of Apple. The pricing growth will offset unit declines and set the stage for a ~10% growth year for TSMC.”

To this end, Shi rates TSM shares a Buy along with a $110 price target, indicating potential for 38% upside in the coming year. (To watch Shi’s track record, click here)

Overall, TSM has 4 recent analyst reviews on record, and they all agree: this is a stock to Buy, giving it a unanimous Strong Buy consensus rating. The shares are priced at $79.45 and their $99.50 average target implies a 25% one-year upside potential. (See TSM stock forecast on TipRanks)

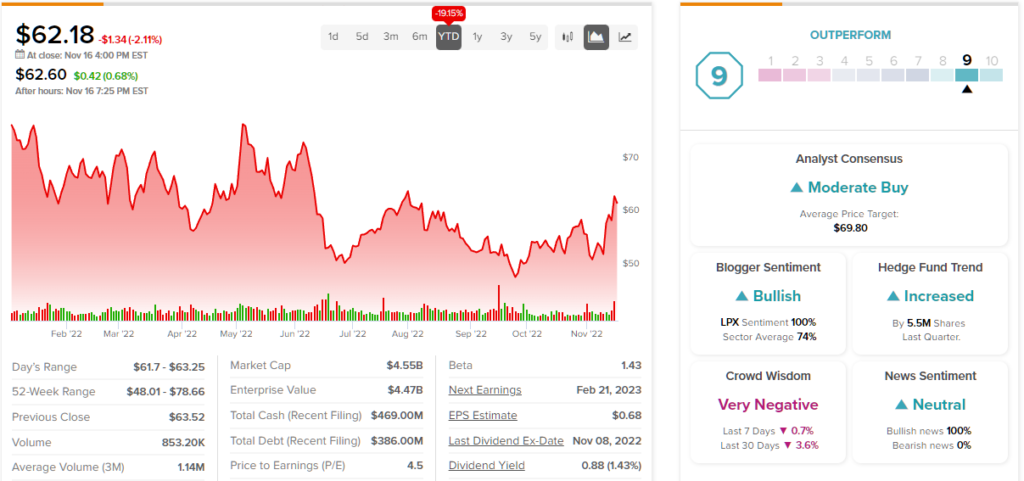

Louisiana-Pacific Corporation (LPX)

The second ‘Buffett-pick’ we’ll look at is Louisiana-Pacific, a Tennessee-based construction materials firm. This company holds a leading position in the global market of oriented strand board and other engineered wood construction and building products. LP markets its product line to builders, contractors, and homeowners, and the current line-up includes wood products for siding, framing, and paneling. LP offers a range of options and upgrades, including fireproofing, weather proofing, and insulation, needed in home construction.

LP’s business can vary quarter to quarter, due to fluctuations in the homebuilding industry caused by weather, mortgage rates, and average house prices. That said, the company brought in $852 million in net sales for 3Q22, down 36% from the year-ago period. Adjusted EPS, at $1.72 per share, was down sharply from the $3.87 reported in 3Q21, although it did handily beat the $1.50 forecast. The company has $482 million in cash at the end of the quarter.

Looking at the dividend, this firm has been paying out consistently since 1974. The current payment, declared in October for a December 1 payout, is set at 22 cents per common share. The annualized rate of 88 cents per share gives a modest yield 1.4%. The key to it is the reliability.

Even though the US home building sector is facing pressures from rising mortgage rates, houses are still getting build – and that means LP’s unique products are still essential. Buffett gave a nod to that in Q3, with a buy of 5,795,906 shares, a new position that is now valued at over $360 million.

Is it a good buy? Seaport analyst Mark Weintraub believes so, laying out an argument that this stock can reward a patient investor. He writes, “For those willing to look through we’d re-emphasize the following: (1) we think LPX has product-driven competitive advantage in Siding with more market share gains, especially in repair/remodel, as well as product mix improvement ahead; (2) its balance sheet remains strong, and (3) valuation is undemanding relative to our sum-of-the parts work. What’s more if LPX’s assessment on return potential from the newly announced Houlton expansion are on the mark, then the company is still in rapid rate value creation mode.”

Based on all of the above factors, Weintraub puts a Buy rating on LPX shares, and his $72 price target implies a one-year upside potential of ~16% for the stock. (To watch Weintraub’s track record, click here)

All in all, LPX currently has a Moderate Buy consensus rating based on 3 Buys and 1 Hold and Sell, each. The average price target stands at $69.80 and suggests upside potential of ~13% in the year ahead. (See LPX stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.