While it is true that Applied Materials’ stock (AMAT) has taken a hit in recent months, it is important to remember that the company is still a leader in its industry and has a strong track record of success. As a result, I am bullish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Applied Materials is a leading manufacturer of equipment and services for the global industry of semiconductors, flat panel displays, and solar photovoltaic (PV) energy.

The company applies innovative nanomanufacturing technology to create high-performance materials that enable the production of smaller, faster, and more energy-efficient chips and displays. Applied Materials also provides equipment and services to support the growth of the solar PV industry.

Due to the issues surrounding the semiconductor space, AMAT has lost steam in the year thus far. The company is due to face some short-term challenges, but it is also in the process of solving a big problem — the shortage of semiconductor chips.

In addition, the semiconductor chip manufacturer is not afraid of making new investments during tough times. Applied Materials has recently purchased Picosun Oy, a privately held company based in Espoo, Finland. The target company focuses on chipmaking equipment, just like Applied Materials.

For this reason and other factors that I will point out in the article, Applied Materials is a great stock in any portfolio.

Why is AMAT Stock Down?

AMAT’s stock price fell this year due to operational problems, a shortage of components, and a troubled economy that has brought gloom to the whole stock market. However, if the company can overcome these challenges, then this may actually be a great opportunity for investors. Nevertheless, the guidance suggests there is more pain around the corner.

Guidance is Spooking Investors

Analysts forecast Applied Materials to generate 9% more profits in the current fiscal year and 17% more by 2023. Although these are respectable numbers, they pale in comparison to Fiscal Year 2021, when the company reported an increase in sales and adjusted earnings of 34% and 64%, respectively.

Applied Materials tells us it is doing well in the semiconductor market, with a large backlog of orders that’s at an all-time high and still growing. As a result, it should continue to have robust demand for its equipment into the future.

Customers of Applied Materials are already securing their supply of semiconductor manufacturing equipment that they’ll need beginning in 2023. This major milestone has been reached ahead of schedule and promptly, thanks to automation.

The demand for silicon is growing, leading to a much more productive capacity. Unsurprisingly, foundries and chipmakers are moving ahead with various steps to fully enhance their machines. It will allow the materials engineering solutions provider to continue growing for the foreseeable future.

Macroeconomic Conditions May Cause Headwinds

The global economy has seen its ups and downs over the past few years, but things may be slowing down. The United States’ economic growth rate is lower than before, leading to an upcoming recession if nothing changes soon enough.

The Federal Reserve is tightening monetary policy by raising interest rates to prevent excessive inflation. A total of seven interest rate hikes will take place this year.

This is why the overall macroeconomic environment isn’t very favorable for businesses. Inflation also means consumers will no longer take much interest in new gadgets as they’ll prioritize necessities.

The semiconductor industry is growing rapidly due to various reasons, such as increased demand from smartphones and tablets that use these chipsets for their operating system software or wireless networking capabilities, among others.

However, no one can deny that the company and the rest of the semiconductor sector did not get a boost due to the pandemic. As a result, the need for semiconductors will eventually normalize, meaning there is potential for an oversupply of inventory if demand falls too much.

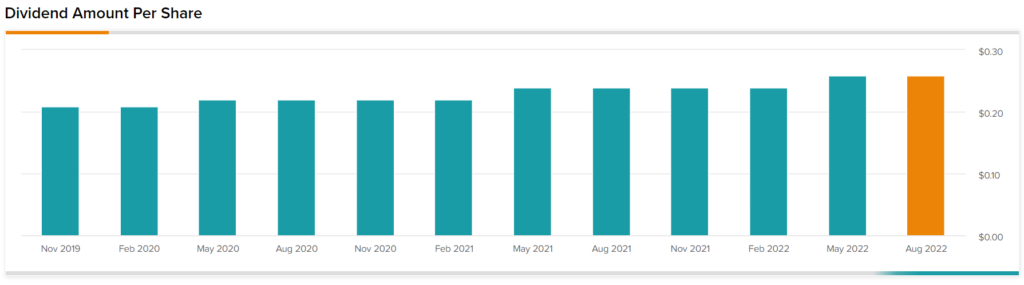

AMAT Stock Has a Growing Dividend

AMAT pays out a small but growing dividend each year, with its latest dividend increase coming in March. The latest increase translates to growth of 8.3%, which is not too bad, considering the state of the markets right now. The company has increased its payouts for five years running.

In addition, the AMAT board has approved a new $6 billion share buyback authorization. This supplements the amount leftover from an earlier repurchase plan worth $3.2 billion. For reference, AMAT has a market cap of $88 billion, equating to a buyback yield of 6.8%

Wall Street’s Take on AMAT

Applied Materials has a Strong Buy consensus rating based on 18 Buys and five Holds. The average price target is $136.50, implying 35.5% upside potential.

AMAT is a Great Stock Trading at a Deep Discount

Applied Materials is a great stock for anyone looking for long-term growth potential. The company is a global leader in the semiconductor industry and has a strong track record of delivering innovative new products. Its products are used in various industries, from consumer electronics to renewable energy. Applied Materials is also a very efficient company with a history of consistently generating strong cash flow and profitability.

In addition, Applied Materials has a strong balance sheet and is well-positioned to benefit from the continued growth of the semiconductor industry. As a result, Applied Materials is a great stock for investors who are bullish on the future of the tech sector.