We’re finally in the homestretch of 2023. The year’s end is in sight – but the only certainty is that uncertainty is here to stay with the headwinds piling up faster than ever.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Check off those headwinds one by one: The Federal Reserve has indicated that it will likely hold interest rates higher for longer, due to persistently high inflation. In geopolitics, China keeps rattling its saber at Taiwan, Russia’s Ukraine war keeps grinding on, and the Middle East has erupted into an open battle between Israel and the Hamas terrorist group. The price of oil has spiked, and investors are moving toward safe havens – gold is close to $2,000 per ounce, and the 10-year Treasury bond yield has touched 5% for the first time since 2007.

That’s quite the backdrop, but it doesn’t mean that we should run away from stocks. On the contrary, the Street’s analysts have been tagging their ‘Top Picks’ for 2024, choosing stocks that they see primed for gains even in today’s unsettled conditions. We’ve used the TipRanks platform to look up 3 of these choice stocks – and found that they are Buy-rated and feature upside potentials ranging from ~20% to more than 150%. Here are their details, along with comments from the analysts explaining just why these are their ‘Top Picks.’

Entegris, Inc. (ENTG)

We’ll start in the tech world, with Entegris, Inc. This company provides a line-up of products that solve the bottlenecks and challenges of high-tech component production, particularly in the vital semiconductor industry. Entegris offers everything from production line components to advanced filtration systems to specialty engineered chemicals, solving its customers’ complex processes to permit higher manufacturing yields, faster performance, and greater product reliability.

Based in Massachusetts, Entegris was founded back in 1966 and boasts a market cap over $13.6 billion. Today, Entegris’ stock is on the way up, having gained 42% so far this year – outperforming the NASDAQ’s 24% year-to-date gain by a wide margin. Much of that jump came in May, when the company’s 1Q23 results beat expectations. The last reported financial results, for 2Q23, also came in ahead of expectations.

At its top line, Entegris reported revenue of $901 million in 2Q23, $14.2 million above the estimates and up some 30% year-over-year. The firm’s bottom line figure, reported as a non-GAAP diluted EPS of $0.66, was 9 cents ahead of the forecasts. The firm’s pockets are deep, with $567 million in cash assets as of July 1 this year, slightly more than the $563 million reported at the end of 2022.

A consistent ability to beat the forecasts forms the heart of Charles Shi’s recent notes on Entegris. The Needham analyst writes, “We think ENTG’s outperformance relative to wafer starts should lead to double-digit growth in 2024, and even stronger growth in 2025. We are maintaining our estimate of 13% pro forma growth in 2024. We believe ENTG will be able to grow by 17% in 2025. We think the company’s $6 EPS target in 2025 is achievable.”

For Shi, this adds up to a spot on the ‘Conviction List,’ a Buy rating, and a $120 price target to imply a one-year upside potential of 32%. (To watch Shi’s track record, click here.)

This growth-oriented tech firm has a Moderate Buy rating from the Street’s consensus, based on 7 recent reviews that include 5 to Buy against 2 to Hold. The stock is selling for $90.70 and its average target price of $115 suggests it will appreciate by 27% over the next 12 months. (See Entegris’ stock forecast.)

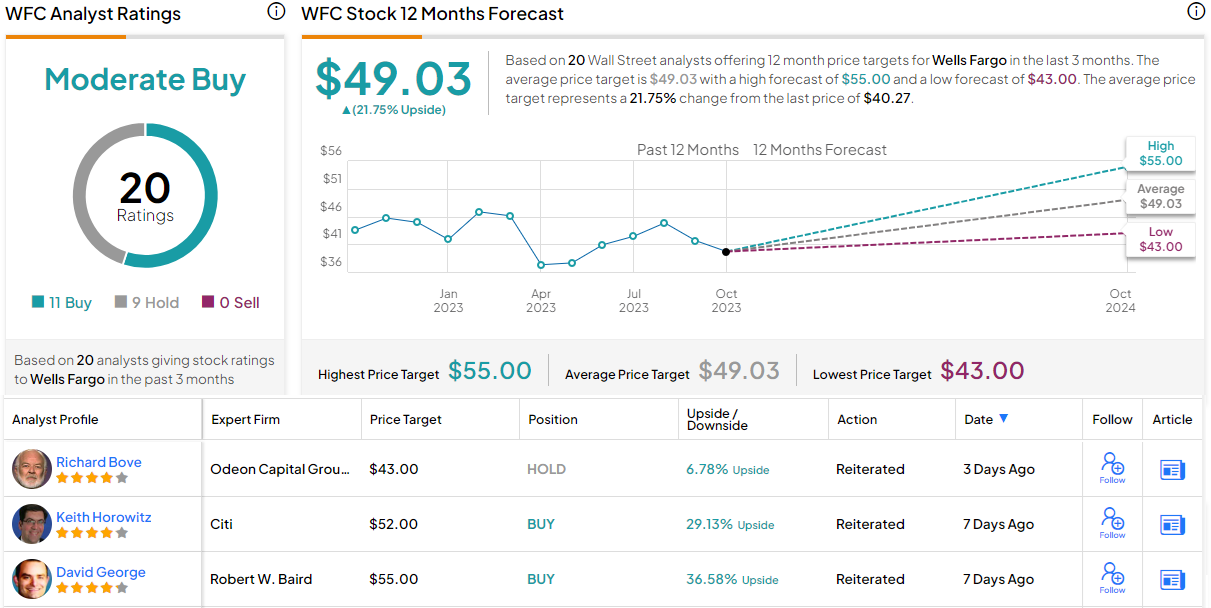

Wells Fargo & Company (WFC)

For the second stock on our list, we’ll switch sights to the banking sector. Wells Fargo is a well-known name, one of the largest banks in the US. The company traces its roots back to 1852, when it provided a combination of banking and express delivery services in the Old West. In its modern form, Wells Fargo boasts a market cap of $147 billion and claims some $1.7 trillion in total assets.

In it primary business, banking, Wells Fargo offers a full range of services, including personal banking, commercial and small business banking, and wealth management for high-income individuals. Specific services include credit cards, mortgage and home equity lending, and capital access for commercial interests. The company has a wide network, totaling some 4,600 branch locations across 36 states plus DC, along with 12,000 ATM machines.

All of that makes a firm foundation for a banking company to stand on – but we should note that against a backdrop of banking sector woes, WFC shares have seen high volatility this year. Currently, the stock is down approximately 1.5% ytd.

Nevertheless, Wells Fargo’s last quarterly report, for 3Q23, came in better than had been anticipated. The company’s quarterly revenue total, at $20.86 billion, was up 6.6% from the year-ago quarter and beat the forecast by $790 million. At the bottom line, EPS of $1.48 was 24 cents better than the estimates. Through the quarter, the company reported carrying an average of $943.2 billion in loans on the balance sheet, more than covered by the $1.34 trillion in average deposits.

During Q3, Wells Fargo bumped up its quarterly common share dividend by 17%, from 30 cents to 35 cents. The new dividend payment annualizes to $1.40 per common share and gives a yield of almost 3.5%.

For analyst Jon Pancari, of Evercore, Wells Fargo presents a solid investment choice, showing a proven ability to maintain its financial performance in a difficult environment. He writes of the stock, “WFC continues to outperform against a tough backdrop marked by challenged funding dynamics, weaker loan demand, low capital markets activity, and normalizing credit. And despite regulatory uncertainty, we remain confident in Wells Fargo’s ability to deliver improving returns and core efficiency gains L/T… Accordingly, we see incremental upside to the stock’s relative valuation at this time, and reiterate our Outperform rating.”

That Outperform (Buy) rating comes along with ‘Top Pick’ status, and a price target of $49 to point toward a 22% upside over the course of the coming year. (To watch Pancari’s track record, click here.)

This is another stock with a Moderate Buy consensus rating; WFC has 20 recent reviews breaking down 11 to 9 in favor of Buys over Holds. The stock’s $49.03 average price target neatly matches the Evercore view. (See Wells Fargo’s stock forecast.)

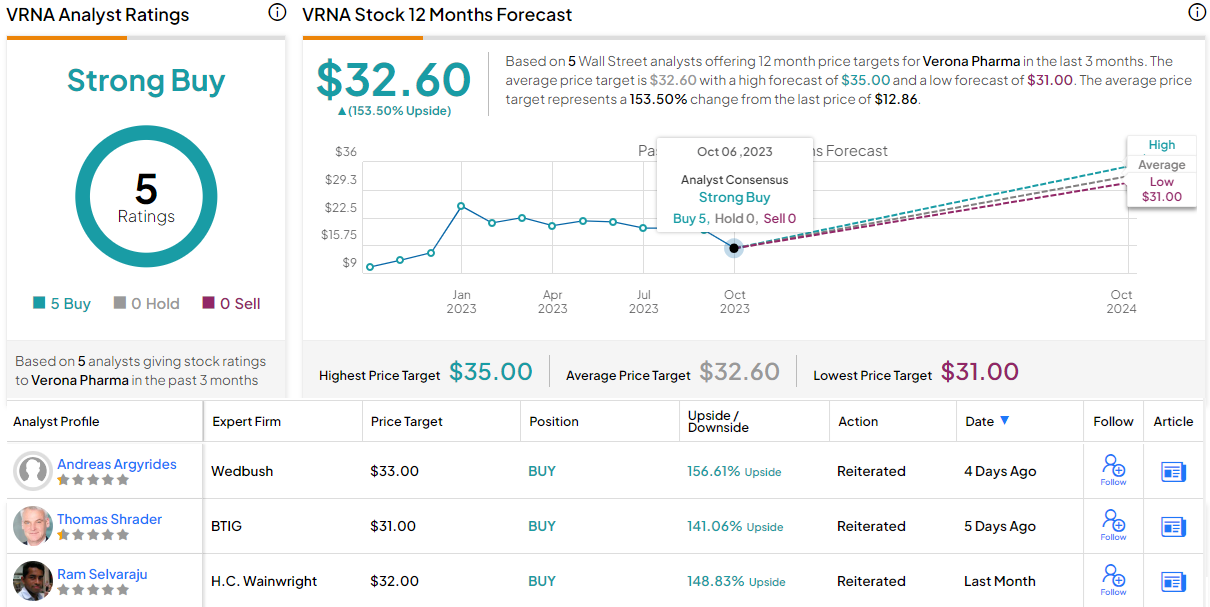

Verona Pharma, Plc. (VRNA)

Last on our list is Verona Pharma, a clinical stage biotech company working on new treatments for breathing disorders. The company has developed a drug candidate, ensifentrine, that combines both bronchodilation and anti-inflammatory activity in one compound – and is non-steroidal. The new drug is a potential treatment for a broad spectrum of lung diseases, including asthma, cystic fibrosis (CF), and chronic obstructive pulmonary disease (COPD).

That last-named indication is the key point when looking at this stock. Verona has already moved ensifentrine through an intensive clinical trial series, from Phase 1 through Phase 3, and has submitted the new drug application (NDA) to the FDA; the application seeks approval of ensifentrine as a maintenance therapy in patients suffering COPD. The application was based on the previous sets of positive clinical trial data, and acceptance was announced on September 11 of this year. The FDA has set a PDUFA date of June 26, 2024, and has not indicated any plans to conduct an advisory committee meeting on the NDA submission.

At the end of 2Q23, Verona reported having $270.7 million in cash on hand, compared to $227.8 million at the end of 2022. With expected UK tax credit receipts and a $150 million credit facility, Verona anticipates a cash runway through the end of 2025 – long enough to include a commercial launch of ensifentrine on approval.

That would be a game changer, and Andreas Argyrides, of Wedbush, sees it as a strong attractive factor for investors, writing of VRNA stock, “We currently project blockbuster FY30 sales of $2.4BN for ensifentrine as a COPD maintenance therapy with an added $412.7M in COPD exacerbations. As such, we continue to see VRNA shares at current levels represent an attractive entry point ahead of the potential U.S. approval in June 2024 and a U.S. launch in H2:24.”

Along with an Outperform (Buy) rating, Argyrides gives VRNA shares a $33 price target to suggest a robust 12-month upside of 157%. (To watch Argyrides’ track record, click here.)

All 5 of the recent analyst reviews here are positive, making the Strong Buy consensus rating unanimous. Verona’s $12.86 current trading price and $32.60 average target price together imply a gain of 153% on the one-year horizon. (See Verona’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.