Markets finished last week on a down note, with the S&P 500 and the NASDAQ falling 2.8% and 3.8%, respectively. The Friday collapse came in the wake of the September jobs report, which further fed into investor worries that the Federal Reserve will continue pushing interest rate hikes even at risk of a recession.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

The headline number, 263,000 new jobs in the month, came in below the forecast of 275,000, and was well below the August print of 315K. At the same time, the headline unemployment rate slipped down to 3.5%. The deceleration in job creation, and the drop in unemployment, signals continued tightening in the labor market, and has investors predicting another 75 basis point rate hike from the Fed later this year. At a time like this, investors are showing a growing interest in finding strong defensive portfolio moves.

It’s a mindset that naturally turns us toward dividend stocks. These are the traditional defensive investment plays, offering steady payouts to shareholders that guarantee an income stream whether markets go up or down. The best dividend stocks will combine a high regular payout with a solid share appreciation potential, giving investors the best of both worlds when it comes to returns.

Wall Street’s analysts have been looking for just such investments, and have picked out several; using the TipRanks database, we’ve pulled up the details on two of these stocks – including one that pays as high as 16% yield. That’s more than enough, on its own, to assure a positive real rate of return, but each of these stocks also brings a double-digit upside potential to the table. Let’s take a closer look.

Sabra Healthcare REIT (SBRA)

If we’re talking high-yield dividend payers, then we’re going to talk about real estate investment trusts, or REITs. These companies own, lease, and manage a range of residential and commercial properties, and in compliance with tax code regulations they pay out a high proportion of profits directly back to shareholders – and dividends a common mode for that return. Sabra Healthcare, the first dividend stock we’ll look at, focuses its operations on properties in the healthcare field.

As of the end of 2Q22, Sabra had investments in 406 real estate properties, with the largest portion of those, 272 properties, being in the Skilled Nursing/Transitional Care niche. The company also had 55 Senior Housing Communities and 50 Senior Housing Communities operated by third parties. Sabra also had investments in smaller numbers of Behavioral Health and Specialty Hospital facilities. Overall, these properties included 40,669 beds or units, and were spread across the US and Canada.

Sabra is scheduled to release its 3Q22 numbers at the beginning of next month – but we can get a feel for the company’s standing by looking into its last quarterly report, for 2Q22. Sabra reported a top line of $155.9 million in revenue for the quarter, a modest gain of 2% year-over-year. Earnings, however, showed a far stronger improvement; EPS was negative in the year-ago quarter, with a loss of 61 cents per share, but in this year’s 2Q report the company showed an EPS profit of 7 cents per share.

Of particular interest to dividend investor, however, is the reported normalized AFFO, or normalized adjusted funds from operations – a key metric as it supports the regular dividend payment. This metric was reported at 38 cents per share in Q2, allowing the company to declare a common share dividend payment of 30 cents. That dividend represented 78% of the normalized AFFO returned directly to shareholders. At the current rate, the dividend annualizes to $1.20, and gives a robust yield of 9.5%.

What all of this adds up to, in the eyes of JMP analyst Aaron Hecht, is a stock that deserves a second look from investors.

“Over the next 12 months we are looking for SBRA to benefit from improving senior housing occupancy, greater availability of non-contract workers, and conversions of low performing facilities to new operators or facility types. In addition, SBRA is looking to dispose of assets, which will bring down leverage to target levels. SBRA currently trades at 9.1x 2023 FFO compared to the healthcare REIT group at 15.9x and we are looking for SBRA’s multiple to expand as the business plan is executed,” Hecht noted.

“Given our analysis, we believe the dividend is safe, assuming there are no further major lease adjustments,” the analyst summed up.

Hecht quantified his bullish stance with an Outperform (i.e. Buy) rating and a price target of $16; at current price levels, this figure implies ~28% upside for the stock in the next 12 months. Based on the current dividend yield and the expected price appreciation, the stock has ~37% potential total return profile. (To watch Hecht’s track record, click here)

Overall, it’s clear that Wall Street agrees with Hecht on the forward prospects for SBRA. The stock’s 8 recent analyst reviews include 7 Buys and 1 Hold, for a Strong Buy consensus indicative of a bullish outlook. The shares are selling for $12.53, and their $16.16 average price target suggests one-year gain of ~29%. (See SBRA stock forecast on TipRanks)

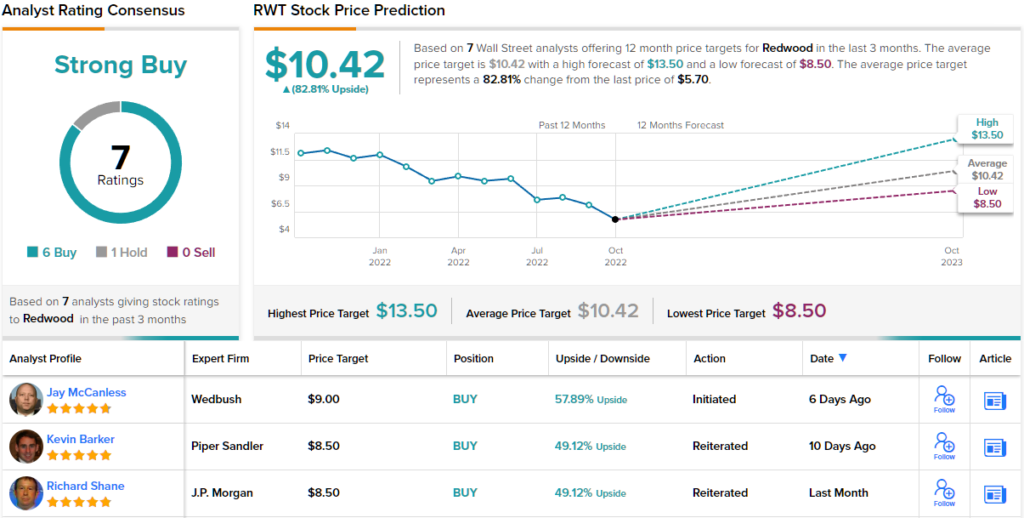

Redwood Trust (RWT)

For the second stock we’ll stick with the REIT sector. Redwood Trust holds a portfolio of residential mortgages and loans; the company acts as a specialized finance company, making capital available to property buyers and builders, through prime rate jumbo residential loans, as well as investments in multifamily securities and mortgage-backed securities. Redwood offers capitalization directly, and works with Federally backed loans through Freddie Mac and Fannie Mae.

Redwood has a long history of keeping reliable dividend payments, going back to 1995. The company’s last dividend declaration was made this past September, for 23 cents per common share, and was paid out on September 30. The current dividend annualizes to 92 cents; while that sounds modest, it represents an impressive yield of 16.1% – not many companies of any sort can offer a dividend yield in that range.

The high-yield dividend is supported by Redwood’s strong balance sheet, which showed a total of $371 million in unrestricted cash at the end of 2Q22, and an available capital total of $190 million. The company was highly active in Q2, funding $932 million in business purpose loans and $1.2 billion in jumbo residential loans.

5-star analyst Jay McCanless, covering this stock for Wedbush, sees Redwood gaining support from the natural population pressure on the housing market – and he believes that support will allow maintenance of the dividend into the near future.

“While we have no insight into future trends in rates and credit spreads, we are of the view that demand for housing should be supported by demographic data that suggests another 5-10 years of demand for housing outstripping supply, and underlying credit metrics should be supported by both stricter underwriting seen over the last decade and more favorable loan to value ratios,” McCanless opined.

“While reported earnings are expected to remain depressed for the rest of 2022, with some recovery likely in 2023, our analysis suggests that the company has more than enough in the way of operating earnings to sustain its current quarterly dividend of $0.23 per share,” McCanless added.

To this end, McCanless gives RWT shares an Outperform (i.e. Buy) rating with a $9 price target to indicate room for a strong 58% upside potential in the coming year. (To watch McCanless’ track record, click here)

Overall, this REIT has picked up attention from 7 Wall Street analysts, and their reviews include 6 to Buy and 1 to Hold, for a Strong Buy consensus rating. The shares have an average price target of $10.42 and a current trading price of $5.70, which translates to an upside of 82% on the one-year time horizon. (See RWT stock forecast on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.