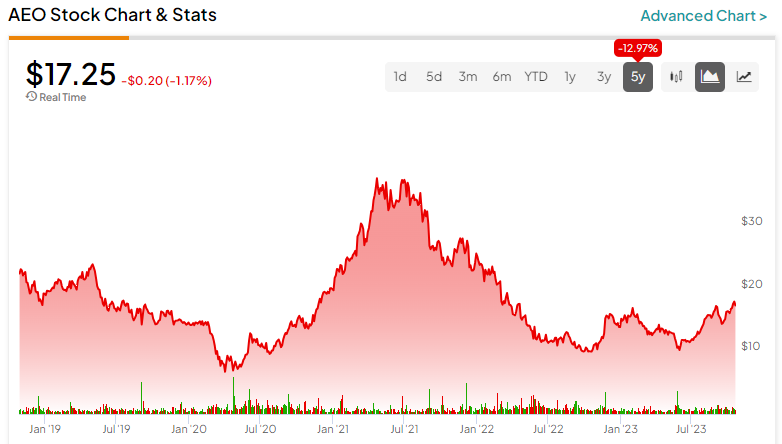

By arguably most logical measures, apparel and accessories retailer and manufacturer American Eagle (NYSE:AEO) represents an incredibly risky investment under current circumstances. Amid rising economic pressures, fewer consumers have access to discretionary funds. Nevertheless, the fashion brand may be a surprising bullish options trade for the daring, as the demand for call options has spiked. Still, I am curious but overall neutral on AEO stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Tough but Compelling Fundamentals for AEO Stock

One doesn’t need to look very far to understand why many investors are hesitant to bet on AEO stock. At the top end, consumer sentiment – while rising sharply from its June 2022 lows – remains deflated compared to pre-pandemic levels. More pressingly, while much progress has been made, inflation remains stubbornly elevated. That has a massive impact on consumer discretionary demand.

At the same time, the surprisingly robust September jobs report shows that while more dollars are chasing after fewer goods, at least those dollars are being spent by more workers. Further, while social-experience-based activities – the so-called “funflation” – have absorbed much of the rise in consumer spending, some evidence suggests that this narrative may be fading.

Specifically, the so-called “revenge travel” catalyst appears to be waning among would-be travelers in other nations. With inflation continuing to crimp purchasing power, it’s possible that consumers may focus on more bang-for-the-buck purchases. That might benefit a trendy fashion brand like American Eagle, thus presenting a possible interesting impetus for AEO stock.

Financial Data Also Nods Favorably for American Eagle

To be fair, American Eagle almost certainly faces the heat from the trade-down effect concept. Basically, consumers facing financial pressures are unlikely to cut all spending cold turkey. Instead, they’ll trade down to cheaper alternatives until an acceptable equilibrium is found between price and quality. However, American Eagle’s financials suggest that the trade-down isn’t a cold, hard headwind.

In particular, data from TipRanks reveals that on a trailing-12-month (TTM) basis, the fashion brand posted total revenue of $4.86 billion. A few line items below, gross profit comes in at $1.79 billion, translating to a gross margin of 36.8%. This metric aligns roughly with prior years’ stats. Significantly, the most important takeaway here is that the company isn’t cutting into its margins to generate revenue under this difficult circumstance.

Put another way, American Eagle – despite being a rather obvious target for the trade-down effect – enjoys pricing power. Even with the perdition that its customers have faced, they’re still willing to open their wallets for its products. That’s an unignorable positive catalyst for AEO stock.

As well, the retailer benefits from consistently positive free cash flow. Again, that’s not a metric to ignore based on the wider context.

Options Dynamics Presents an Intriguing Look

From a common-sense standpoint, investors will want to be extra cautious about AEO stock. While certain factors – such as stable gross margins – point in a positive direction, the consumer economy is still relatively frail. With major corporations still planning or implementing mass layoffs, it wouldn’t take much for consumer discretionary sentiment to drop. Nevertheless, the options market presents an intriguing look for American Eagle.

First, forward-looking options sentiment – as determined by put/call ratios at various future strike prices – appears generally positive. For example, for the upcoming expiration date of Friday, October 27, open interest for put options outnumber that for call options. In particular, that’s because the $16 put currently features an open interest of 2,053 contracts.

However, looking ahead to future expiration dates, the put/call open interest ratio slips below the 1:1 threshold, indicating that more traders are acquiring call options than puts. Since owning calls gives holders the right to buy the underlying security at the listed strike price, consistently greater interest toward calls may be a bullish signal.

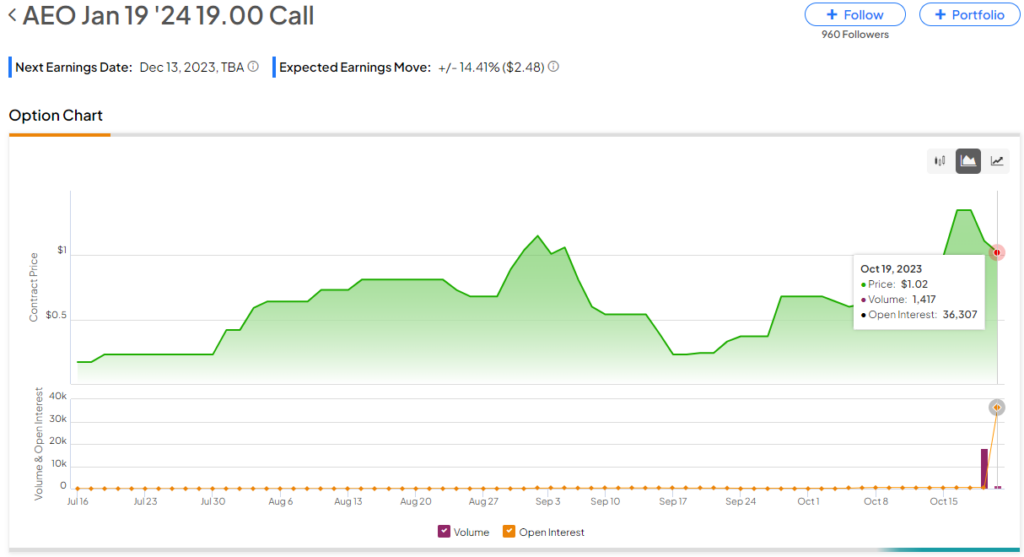

More enticingly, on October 19, options flow data – which screens exclusively for big block trades likely made by institutions – shows primarily bullish activity, either bought calls or sold puts. Specifically, a trader (or traders) bought 1,777 contracts of the January 19 ’24 19.00 Call, paying a premium of $206,132 for the privilege.

What’s fascinating about this trade is that it appears to have caught the attention of retail traders. Subsequently, on October 20, TipRanks showed the open interest for this call jumping from 504 contracts to a staggering 36,307.

If you’re bullish, you might be inspired by the confidence in numbers.

Is AEO Stock a Buy, According to Analysts?

Turning to Wall Street, AEO stock has a Hold consensus rating based on three Buys, three Holds, and two Sell ratings. The average AEO stock price target is $18.19, implying 5.7% upside potential.

The Takeaway: AEO Stock Deserves at Least a Second Look

Arguably, for most conservative investors, AEO stock might be too fundamentally risky to consider. However, for contrarians looking for an unorthodox opportunity, American Eagle could be interesting. There may be enough positives alongside clear demand for call options to warrant calculated speculation.