Airbnb Stock (NASDAQ:ABNB) continues to have exciting upside prospects despite rallying by about 50% year-to-date. As a leading global platform for seamless bookings in unique accommodations, Airbnb consistently achieves strong growth and maintains high margins—an encouraging trend poised to persist. While there are inherent risks associated with the company’s investment case, including regulatory concerns, I believe these concerns are overblown. Thus, I am bullish on the stock.

Airbnb’s Lean Model Delivers Robust Growth & High Margins

Airbnb’s bullish case is rooted in the effectiveness of its streamlined business model, which consistently delivers robust growth and impressive profit margins. The company operates with minimal capital as a booking facilitator, enjoying elevated gross margins. This is because Airbnb has become synonymous with travel. Its brand recognition eliminates the need for substantial advertising expenditures. Therefore, the company can record remarkable net income/free cash flow margins as well.

Moreover, the company is fortunate to be able to capitalize on organic growth trends, ensuring sustained expansion in the coming years. In sync with the flourishing global travel industry, which is expected to grow, on average, at 5.8% per year from 2022 to 2032, Airbnb is well-positioned to leverage this momentum. Thus, it should continue to attract increasing bookings over the years naturally.

Additionally, as rising inflation and other factors drive rental prices upward, Airbnb stands to benefit organically, as its fees are a percentage of the total booking value of each stay.

The organic tailwinds Airbnb enjoys remind me of the success story of the most mature player in the field, Booking Holdings (NYSE:BKNG), which has consistently demonstrated growth by leveraging similar trends. With its lean business model, Booking Holdings has showcased remarkable margins, maintaining an EBITDA margin between 30% and 40% over the years, excluding isolated occasions. This further underscores the potential for Airbnb to follow a similar path of sustained success.

Airbnb’s most recent results showcased this theme. In Q3, the company reported revenues of $3.4 billion, marking an impressive 18% increase compared to the previous year. This substantial increase is attributed to heightened demand in the travel sector. Furthermore, Airbnb’s adjusted EBITDA for the quarter reached $1.8 billion, showcasing a remarkable 26% surge year-over-year. This highlights the business’s continued resilience and stresses the adept cost-control measures the management team implements.

In addition, the company generated substantial free cash flow of $1.3 billion. So, back to my argument about margins, Airbnb’s adjusted EBITDA and free cash flow margins stand at 54% and 39%, respectively. It becomes evident, without much elaboration, that the company is effectively printing cash while posting highly attractive top-line growth — all this during a very shaky macroeconomic environment.

Regulatory Risks

Despite Airbnb’s impressive performance and promising future outlook, a cloud of regulatory concerns looms over the company, causing unease among investors. These regulatory concerns pose a potential threat to the stock as worries persist regarding the impact on Airbnb’s performance if they materialize.

The regulatory challenges at hand revolve around recurring conflicts between Airbnb and local governments, driven by concerns that Airbnb rentals may jeopardize the well-being of local residents. This arises when landlords, motivated by the allure of short-term profitability, choose to list their properties on Airbnb rather than pursuing conventional long-term leases.

Consequently, this practice leads to a scarcity of available housing, pushing rental prices for the remaining properties to unattainable levels for most residents. Currently, numerous countries and cities have implemented diverse restrictions on the platform. These include Singapore, Japan, and Thailand, among other destinations. This has further intensified the regulatory landscape surrounding Airbnb.

Despite the perceived risk, I believe Airbnb’s global impact won’t significantly harm its performance. Airbnb is crucial for local economies, especially in tourism-driven areas, where short-term rentals provide vital income for many households. Further, banning Airbnb could disrupt these regions, as hotels may struggle to meet the excess demand, harming local economies reliant on tourism. In the meantime, Airbnb’s continuous growth against all backlash is a testament to the platform’s resilience.

Is ABNB Stock a Buy, According to Analysts?

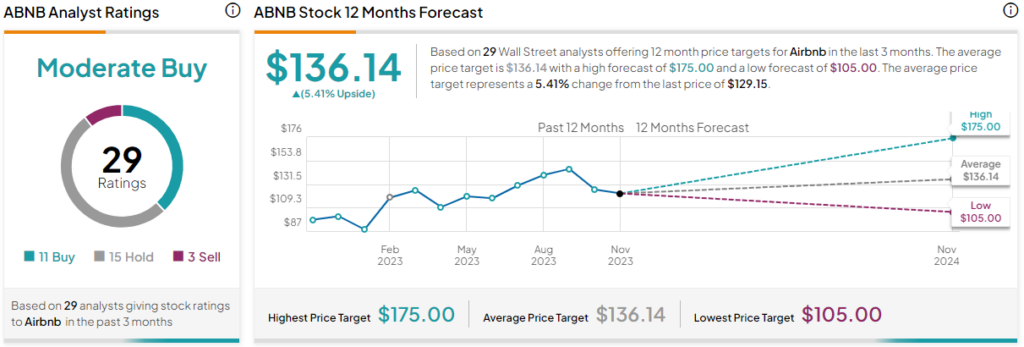

Turning to Wall Street, Airbnb has a Moderate Buy consensus rating based on 11 Buys, 15 Holds, and three Sells assigned in the past three months. At $136.14, the average Airbnb stock forecast implies 5.4% upside potential.

The Takeaway

Airbnb emerges as a compelling investment with its lean business model driving robust growth and high margins. The company is riding the favorable momentum generated by organic growth trends within the flourishing global travel industry, strategically positioning itself for enduring success.

While regulatory concerns cast a shadow, Airbnb’s resilience in the face of challenges and its vital role in local economies underscore its long-term potential. Consequently, despite its already strong year-to-date rally, I will remain invested in the company.