As a narrative, Airbnb (NASDAQ:ABNB) – which specializes in providing an online marketplace for short and long-term homestays – weaves a brilliant tale. Essentially, the company caught the attention of investors by leveraging unused space in a capitalistic endeavor, thereby legitimately unlocking value. However, a lack of a distinct business offering and the fading “revenge travel” phenomenon are two issues that may hurt the company. Therefore, I’m bearish on ABNB stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

A Strong Q3 Print Only Tells Part of the Story of ABNB Stock

At first glance, Airbnb might seem like an attractive opportunity. While ABNB stock has gained over 44% since the start of the year, in the trailing half-year period, it slipped more than 2%. Thus, on a relative basis, it appears undervalued. Also, the company posted strong results for its third-quarter earnings. However, that only told part of the story.

At a quick glance, Airbnb posted earnings per share of $6.63. This figure handily beat the consensus target of $2.12 per share. Additionally, Airbnb rang up sales of $3.4 billion, beating the consensus of $3.37 billion.

Adding to the robust results, Total Nights and Experiences Bookings landed at 113.2 million in Q3. In the year-ago period, this stat came in at 99.7 million. As well, the sharing economy specialist beat the consensus view of 112.9 million.

However, management expects Q4 revenue to reach between $2.13 billion and $2.17 billion. Unfortunately, this forecast slipped a bit under the $2.18 billion that analysts anticipated. It appears that key catalysts for ABNB stock are losing steam. Even more worrying, that’s not a far-fetched speculative argument.

In October, Airbnb Founder and CEO Brian Chesky admitted concerns about low bookings and their profits during a Bloomberg interview. “We need to get our house in order. We need to make sure the listings are great, we’re providing great customer service and we’re affordable. And I’ve told our team that we can get back to creating new and exciting things once we’ve fixed that foundation.”

Moving ahead, though, the challenge is that not all of Airbnb’s headwinds are directly addressable.

Diminished Revenge Travel Could Impact Airbnb’s Core Business

During the worst of the COVID-19 pandemic, the concept of retail revenge materialized. Basically, consumers sought retail therapy, and it had a massive impact, with e-commerce representing 16.5% of all retail transactions in Q2 2020. Later, the travel equivalent soaked up vast swathes of consumer dollars. Sadly, all good things must come to an end.

For ABNB stock, the revenge travel phenomenon needs to accelerate, not wane. As the CEO admitted and as the company’s Q4 forecast revealed, industry data points to decelerating travel demand. Tragically, the Hamas attack on Israel, along with Russia’s ongoing invasion of Ukraine – not to mention other geopolitical flashpoints and tensions – don’t help matters.

By pure numbers, for every major conflict that emerges, that leaves fewer areas which people may travel. Moreover, economic headwinds such as high inflation and simultaneously high borrowing costs crimp consumer sentiment. Subsequently, airliners arguably face serious concerns. By logical deduction, if fewer people are flying, less demand exists for lodging services.

In addition, corporate layoffs are still occurring because of reduced spending broadly. That may stymie discretionary spending, which in turn may hurt ABNB stock.

First Mover, Not Only Mover

Previously, some analysts have made the point about Airbnb creating a practical monopoly in the short-term rental space. Certainly, the company carries the first-mover advantage of monetizing individual homeowners’ unused space. However, as other companies catch wind of the concept, ABNB stock will almost invariably suffer from stiff competition.

That’s especially worrisome if Airbnb rentals march toward parity with their hotel equivalents. The latter offers heavily regulated professionalism and protocol standardization; the former simply does not. If price parity becomes a reality, ABNB stock risks losing relevance.

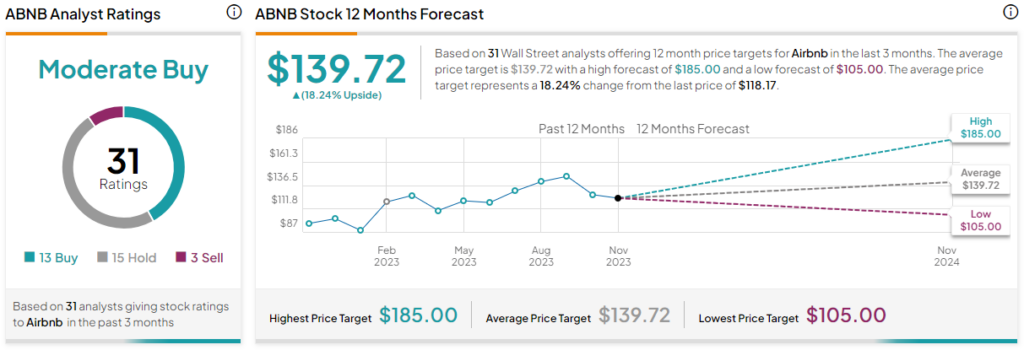

Is ABNB Stock a Buy, According to Analysts?

Turning to Wall Street, ABNB stock has a Moderate Buy consensus rating based on 13 buys, 15 Holds, and three Sell ratings. The average ABNB stock price target is $139.72, implying 18.2% upside potential.

The Takeaway: Read the Signs About ABNB Stock

While Airbnb deserves respect for identifying a business opportunity and thus unlocking billions of dollars of hidden value, the realities of the post-pandemic economy may be catching up to the business. Investors only need to read the signs of travel-related headwinds along with the company’s own broadcasted anxieties. Therefore, a cautious approach to ABNB stock may be prudent.