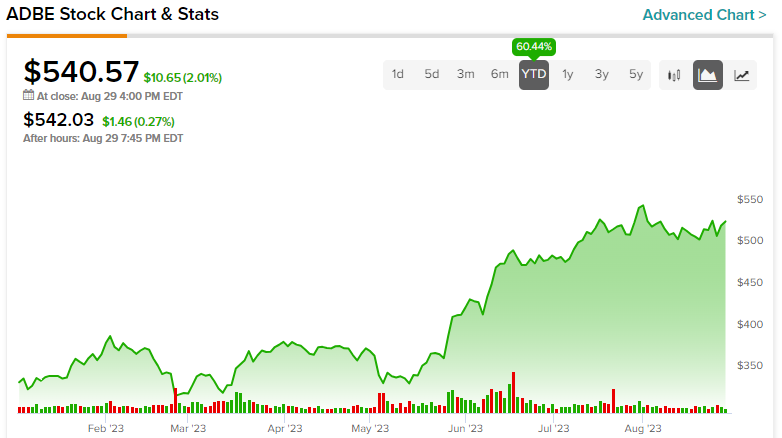

Adobe stock (NASDAQ:ADBE) has gained more than 60% year-to-date, which could urge investors who missed the rally to wait for a better price before potentially allocating capital to the creative software giant’s shares. However, the prospect of awaiting a more opportune entry might prove to be an exercise in futility.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The factors supporting a less cautious stance are compelling. Adobe’s consistent growth trajectory, its dominant position in the industry, and the persistent tailwinds generated by AI-driven innovations all align to project a distinctly bullish sentiment. Despite the seemingly elevated valuation of Adobe, I find ample justification for such a valuation. Hence, I remain bullish on ADBE stock.

Consistent Double-Digit Growth Despite Industry Saturation

Adobe’s remarkable capacity to consistently achieve double-digit growth is truly awe-inspiring, particularly when one considers the initial belief that the creative software industry had become saturated in a post-COVID world.

Specifically, with the rapid expansion of the content creation industry during the COVID-19 pandemic, many anticipated a saturated market and believed Adobe’s revenue would soon plateau without significant catalysts for growth. However, this has not been the case.

In its most recent fiscal Q2 results, Adobe posted revenue growth of 10% (or 13% in constant currency) to a new quarterly record of $4.82 billion. To give you some context regarding Adobe’s ability to consistently grow its revenues in the double-digits, the company’s three-year, five-year, and 10-year revenue CAGRs (compound annual growth rates) now stand at 15.5%, 17.0%, and 16.9%.

Given Adobe’s near-monopoly position in the creative software industry and its continual innovation in the ever-evolving content creation landscape, the reasons for the company’s impressive and sustained growth become clear. Interestingly enough, Adobe finds itself in the midst of the ongoing craze in AI developments, as artificial intelligence has unlimited applications around digital content, positioning Adobe for another era of booming growth.

Adobe’s Firefly & Express’ Effect on Growth

Adobe has been moving fast in the AI world, with its R&D investments leading to the rapid development and deployment of Firefly, the company’s generative AI technology. As you may know already, generative AI’s capabilities depend on the amount of data it can be trained on. This is true for all kinds of AI, such as ChatGPT. In that regard, the company has a significant advantage, as its rich data sets from creativity, documents, and customer experiences enable Adobe to teach models on the highest-quality assets.

From its launch in late March until Adobe’s Q2 results (June 15th), Firefly captured the imagination of the world with over 500 million generations, and the company is “just getting started.” On August 15th, Adobe launched Express, the latest iteration of an all-in-one AI content creation app. Integrated with the Firefly beta’s generative AI capabilities, it’s revolutionizing creative expression, enabling users of all skill levels to design and share exceptional content.

The transformative power of these AI tools extends to novices who might lack prior experience with Adobe’s creative suite. As a result, the company is poised to welcome an influx of new users previously incapable of independently navigating its software. This imminent wave of adoption promises to be a potent driver of growth, particularly considering the persistent surge in demand for content creation solutions.

The Valuation Might Look Pricey, but It’s Likely Justified

With Adobe being in the spotlight of AI innovation in the creative software industry, shares have experienced a strong rally year-to-date that has, in turn, resulted in the stock’s valuation expanding. Based on the company’s performance during the first half of its fiscal year, management expects that Adobe will achieve adjusted EPS between $15.65 and $15.75 for the full year. The midpoint of this range implies that Adobe is currently trading at a forward P/E of 34.4.

While this multiple may seem somewhat rich within the context of rising rates, I find it quite reasonable, given Adobe’s ever-consistent ability to deliver double-digit growth, its unbreakable moat, and the AI-powered growth potential. In fact, analysts expect that Adobe’s EPS growth will be sustained well within the mid-teens, which, along with its underlying qualities, do deserve the underlying premium present.

Is ADBE Stock a Buy, According to Analysts?

Turning to Wall Street, Adobe has a Moderate Buy consensus rating based on 19 Buys, nine Holds, and one Sell assigned in the past three months. At $550.83, the average Adobe stock forecast suggests just 1.9% upside potential over the next 12 months.

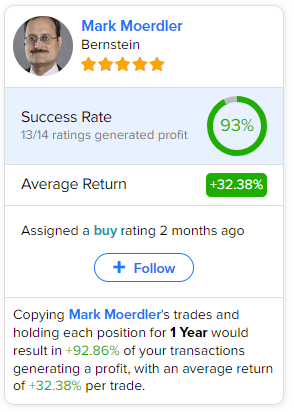

If you’re wondering which analyst you should follow if you want to buy and sell ADBE stock, the most accurate analyst covering the stock (on a one-year timeframe) is Mark Moerdler of Bernstein, with an average return of 32.38% per rating and a 93% success rate. Click on the image below to learn more.

Final Thoughts

In conclusion, as Adobe’s meteoric year-to-date rise prompts potential investors to wait for a more opportune entry point, the prospect of such an entry might be an exercise in futility. The compelling combination of Adobe’s unwavering growth trajectory, dominant industry position, and AI-driven innovations generates robust bullish sentiment. Thus, the prevailing high valuation appears justified, in my view.