Building systems maker Acuity Brands (AYI) recently released its earnings report. The news was good by all accounts. However, success for Acuity here will depend on a lot of things going just right, and that’s usually not a strategy to count on succeeding. Therefore, I’m neutral on AYI and will not be joining in on buying the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

While Acuity is somewhat narrow in its focus—it mainly produces systems in lighting controls and building management operations—it still has a decent value proposition, going forward.

With a few minor adjustments to its marketing, it may be able to position itself well going into a likely recession. Since a growing number of analysts believe that such an event is in the making, making plans to weather this storm is likely a smart move.

Acuity’s last 12 months have been up and down, and pretty much in that order. A steady rise between late June and early November saw the company climb. Share prices went from around $170 per share to over $220 in that time. The peak didn’t last, however, as Acuity spent the next several months in decline, closing below $150 a little over a week ago.

The latest news at Acuity proved positive, however, and helped get the company off its lows. The company’s earnings report revealed earnings of $3.52 per share for the quarter, which handily beat the Zacks estimates of $2.98 per share.

It also readily beat the year-ago figures of $2.77 per share. Revenue was also a winner, coming in at $1.06 billion, which beat Zacks estimates once more, this time by 6.4%.

The news was good enough to push the company up 5.5% in premarket trading on Thursday. However, the stock is now up only about 1%.

Wall Street’s Take

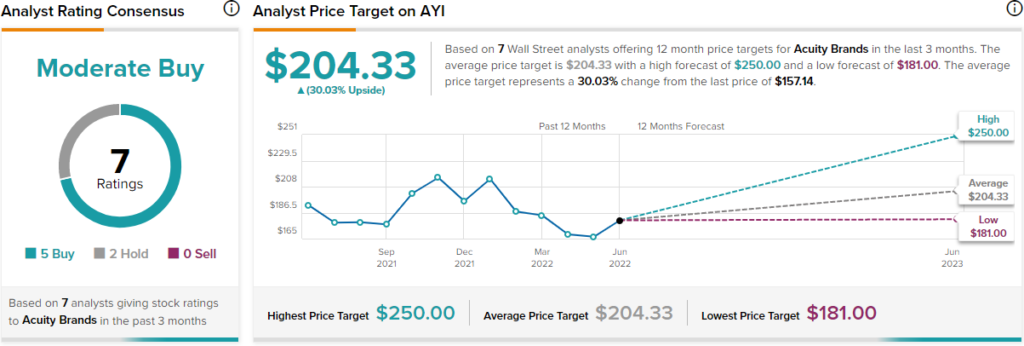

Turning to Wall Street, Acuity Brands has a Moderate Buy consensus rating. That’s based on five Buys and two Holds assigned in the past three months. The average Acuity Brands price target of $204.33 implies 30% upside potential.

Analyst price targets range from a low of $181 per share to a high of $250 per share.

Investor Sentiment is Going Dark

There are still those who look for big things from Acuity Brands. Acuity currently has a Smart Score of 8 out of 10 on TipRanks, putting it at the lowest level of “outperform.” That makes it more likely than not to do better than the broader market. There is certainly a case for this to happen, but many metrics of investor sentiment aren’t looking for that to happen.

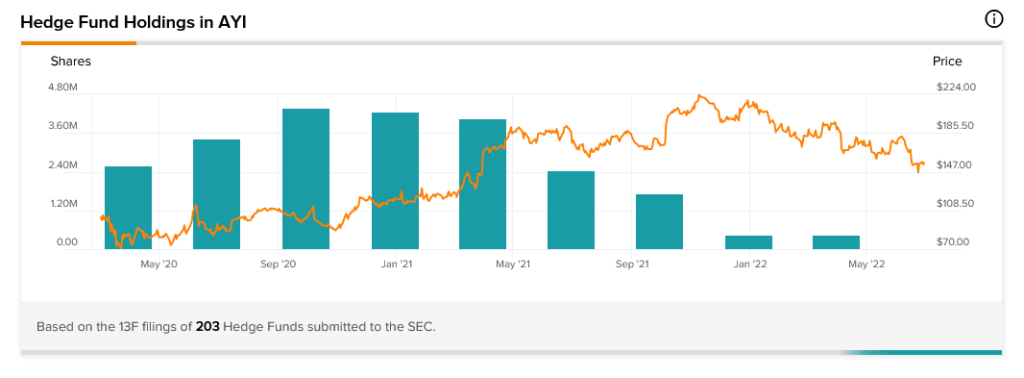

Hedge fund involvement, for example, isn’t looking for that outcome to occur. The TipRanks 13-F Tracker reveals that hedge funds’ stakes in Acuity have been in continuous decline since September 2020.

While hedge funds only reduced their stake by a collective 6,200 shares in the drop between December 2021 and March 2022, the 439,325 shares owned today is a drop in the bucket against September 2020’s high-water mark of about 4.39 million shares.

Insider trading also suggests a declining picture. Insiders have not bought shares of Acuity since December and, so far this year, have only sold. For 2022, Sell transactions outpaced Buy transactions by five to zero.

It’s a bit different for the full year, in that there is some buying activity. However, sellers are still ahead, with an overall transaction score of 17 Sell transactions to nine Buys.

Retail investors—at least, those who hold portfolios on TipRanks—were with the company but are swinging negative. TipRanks portfolios holding Acuity were up 1.8% in the last 30 days. However, in the last seven days, they’re down 1.8%.

Perhaps most interesting of all is Acuity’s dividend history. The company has maintained a stable dividend of $0.13 per share for the last three years. This includes the pandemic. The dividend has seen no raises in that entire time. However, it has also seen no decline.

Last One Out of Acuity, Please Turn Out the Lights

The biggest reason behind Acuity’s gains, reports note, was the strength in its lighting division. This makes a certain sense; looking at Acuity’s product line shows that a lot of the company is the lighting division, in one way or another.

It has applications for UV sterilization, horticultural lighting, and of course, for lighting in general. Indoor, outdoor, commercial, and residential; if it lights up, Acuity likely has something related to it – and that’s part of the problem.

Acuity is likely reliant, at least in part, on new building construction. Granted, that’s not all of Acuity’s business; renovations and repairs are likely to be part of the picture as well.

However, new building construction is certainly a leg in the stool that is Acuity’s earnings picture. That leg is looking very shaky and will probably fall out of the stool altogether before much longer. The National Association of Home Builders found builder confidence in the residential market at a low not seen since June 2020.

Granted, with some effective marketing, Acuity might be able to get through an upcoming recession. After all, its focus on lighting controls can represent significant savings in power bills.

The U.S. Chamber of Commerce took a look at energy costs in the U.S. back in May and found that 2021 saw electricity prices go up 5.6%. That, at the time, was a record. A record that’s likely been broken at least once since then, too.

By positioning itself as a way to save money on electric bills, Acuity can likely keep its sales going long enough to hold itself over until new construction starts up again. However, that’s still a recession footing strategy. It’s likely not going to prompt big gains over the next few years like we only recently saw. It’s essentially going to be a survival strategy.

Concluding Views

It’s likely tempting to Buy in on Acuity Brands. The company is trading well under its lowest price targets. Sufficiently so, in fact, to make even the average target look like a challenge to reach. However, there’s no denying that Acuity is likely to face some challenging times, going forward.

Its product line is rather diversified but within a narrow framework. With new construction likely about to decline with an upcoming recession, there won’t be near so much call for lighting controls—especially not the kind that exceeds the previous year’s sales figures.

Keep an eye on Acuity Brands. It’s probably got more ground to lose. However, when things start to recover from the recession that’s all too likely to hit, it’s just as likely to be one of the first to recover along with the overall economy. That’s why, for now, I’m neutral on the company that’s probably going to be hit hard but is also likely to recover quickly.