PayPal stock (NASDAQ:PYPL) has plunged by roughly 80% from its 2021 highs of ~$310. At $64.44 today, shares are currently trading at the same levels they did all the way back in 2017. This is despite PayPal’s progress in growing revenues and profits during these past six years. The market’s response is justified, given the rising competition and interest rate hikes, which warrant a reduced valuation. That said, PayPal seems to present an excellent value proposition at its present valuation. Thus, I am bullish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

What’s Keeping Paypal Stock Under Pressure?

Undoubtedly, the primary factor exerting downward pressure on PayPal’s stock is the rising competition. Over the past decade, the fintech sector has exploded, with venture capital pouring in and private equity driving numerous deals. This has birthed a swarm of startups vying for market share from industry giants like PayPal.

A considerable number of these newcomers, while not direct competitors, share common interests with PayPal, which had held an undisputed reign for the longest time. The era of PayPal’s uncontested reign is now undergoing substantial turmoil. Across the spectrum of digital payments and online banking, formidable contenders are emerging. While PayPal has long maintained its supremacy in the realm of online payments, the new competition is undeniably relentless.

As numerous fintech players aim to unseat PayPal, battles are unfolding in multiple arenas—mobile payments, digital wallets, cryptocurrencies, and online banking. PayPal’s extensive reach faces a growing number of rivals armed with innovation.

The burning question here is whether PayPal can maintain its dominant position in the face of fierce competition. It’s a challenging prospect, especially when you consider that PayPal’s rivals offer similar or even superior services at more competitive prices. Let’s take card payments as an example.

PayPal charges a transaction fee of 2.99% plus $0.49 for each card transaction. In comparison, Block’s (NYSE:SQ) Square charges 2.6% plus $0.10 per card transaction, while Stripe charges 2.7% plus $0.05 per card transaction. In fact, PayPal stands out as the most expensive option among all the prominent players in this industry.

Now, let’s compare PayPal’s international transfers to another leading competitor, Wise (GB:WISE). If you send £1,000 today through Wise to a recipient who will receive the funds in Euros, they’ll get the money within two hours, and they’ll receive 1,156.56 Euros. On the other hand, if you choose PayPal, the transfer could take up to four days, and the recipient will receive only 1,107.66 Euros due to PayPal’s higher conversion fees.

PayPal’s enduring dominance in the industry is undeniable, thanks to its longstanding presence and deep customer relations. However, given the numerous and more beneficial alternatives, it’s apparent why investors are growing uneasy about the company’s sustainability in the long run.

PayPal to Achieve Record Fiscal 2023 Earnings Despite Challenges

Despite the ongoing challenges PayPal is facing, the company is set to achieve record earnings in Fiscal 2023. This is due to a mix of higher revenues due to inflation, disciplined cost management, and notable stock buybacks.

In particular, in its most recent Q2 results, revenues grew by 8% on a currency-neutral basis to around $7.3 billion. This was driven by an 11% increase in Total Payment Volumes (TPV), offset by PayPal’s take rate declining by 11 basis points to 1.74%, and the lapping of certain items that provided an outsized benefit in Q2 of last year.

In my view, PayPal’s top-line results were considerably underwhelming despite the growth. The double-digit TPV increase may sound optimistic, but given the significant inflation of the past year, the metric’s real growth was, in fact, notably inferior.

Wise’s payment volumes, for instance, grew by a much more powerful 37% during Fiscal 2023. Stripe’s volumes are speculative due to the company remaining private but are still estimated to grow by roughly 22% this year to $1 trillion.

Despite this weakness, PayPal’s management has become increasingly disciplined with the expenses it can control. In fact, expenses moderated on multiple fronts in Q2, giving room for profits to grow. Here are some expenses that fell:

- Customer Support and Operations expenses fell by 8.2% to $492 million.

- Sales and marketing expenses fell by 21.8% to $465 million.

- Technology and development expenses fell by 8.8% to $743 million.

- General and administrative expenses fell by 4.5% to $491 million.

Thus, despite higher transaction costs, PayPal’s adjusted EPS grew by 24% to $1.16. PayPal repurchasing $5.17 billion over the past four quarters also boosted this result. Based on the company’s performance in Q1 and Q2, as well as the current momentum of the business, PayPal’s management projects that EPS will rise by roughly 20% and reach a new record of $4.95 this year.

Consequently, despite the ongoing pressure PayPal is facing and concerns competition could have on its future results, its profitability still remains very strong.

What are Analysts Saying About PYPL Stock?

Turning to Wall Street, PayPal has a Moderate Buy consensus rating based on 20 Buys and nine Hold ratings assigned in the past three months. At $88.22, the average PayPal stock forecast suggests 36.9% upside potential.

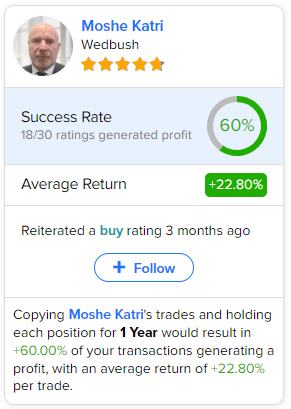

If you’re wondering which analyst you should follow if you want to buy and sell PYPL stock, the most profitable analyst covering the stock (on a one-year timeframe) is Moshe Katri from Wedbush, with an average return of 22.80% per rating and a 60% success rate. Click on the image below to learn more.

The Takeaway

Overall, while PayPal faces mounting competition and pricing challenges, it’s on track for record earnings in Fiscal 2023 due to disciplined cost management and stock buybacks. Adaptation and innovation will be key to its long-term success in an ever-evolving market. Still, with shares currently trading at just 12.7x management’s projected EPS for the year, PayPal seems to be offering a compelling risk-reward ratio with a reasonable margin of safety embedded.