It might be logical to assume that stocks with heavy short interest – i.e., ones that many investors/traders are essentially betting against – are stocks to stay away from, but that is not always the case.

Opinions on the stock market can be varied, and it’s not uncommon to find stocks with both high short interest and positive recommendations from Wall Street analysts.

But only one can be right, right? And should the analysts turn out to be the ones to hit the nail on the head, panic-induced short covering shenanigans could take place and that could result in a short squeeze – when the short sellers buy back in to cover their losses.

So, with all this as backdrop, we’ve opened the TipRanks database to find 3 names that fit a particular niche; stocks with a high short interest – in the order of 25% and above – but ones which the Street’s analysts have designated as Strong Buys. Here are the details.

Harmony Biosciences Holdings (HRMY)

Let’s begin in the healthcare industry with Harmony Biosciences, a company formed with a mission to develop and bring to market state-of-the-art treatments for people living with rare neurological conditions with unmet medical needs.

A biotech’s holy grail is to get a drug approved by the regulators; a feat already achieved by Harmony. Wakix (pitolisant) is the first non-narcotic treatment for narcolepsy and was approved by the FDA to treat adults with the disorder in 2019. Pitolisant is also being assessed for possible label expansion to pediatric use and other neurological indications, the most advanced program being the Phase 3 INTUNE study evaluating pitolisant in adult patients with idiopathic hypersomnia (IH). The company recently announced an accelerated timeline of the study and now anticipates enrollment will be completed during the current quarter with a topline data readout expected in 4Q23.

The drug has been selling well and helped revenue climb by 40.7% year-over-year to $128.31 million in the most recently reported quarter – for 4Q22, whilst also edging ahead of consensus by $0.97 million. Adj. EPS of $1.01 also beat the $0.78 forecast.

So, sounds fairly successful but with the short percentage of the share float (as of Apr 13) being at 36.16%, many are betting against Harmony’s success. That can be somewhat attributed to a March short report by Scorpion Capital that claimed, “people have blood on their hands.”

As often happens, the report sent the stock into freefall, but its contents are given short shrift by Raymond James analyst Danielle Brill, who believes the report “lacks substance and the short thesis is pretty much baseless.”

“The main argument for why HRMY has blood on their hands is related to Wakix’s QTc prolonging effects, and potential related cardiac toxicity,” Brill went on to say. “The short report believes the FDA failed to do their jobs, but we see zero indication of that, and believe Wakix’s safety profile is not an issue based on our own diligence with prescribers. To put things in perspective, a warning for QTc prolongation is highlighted on front page of Wakix’s label, and its main competitor in the narcolepsy market – is literally the ‘date rape drug.’”

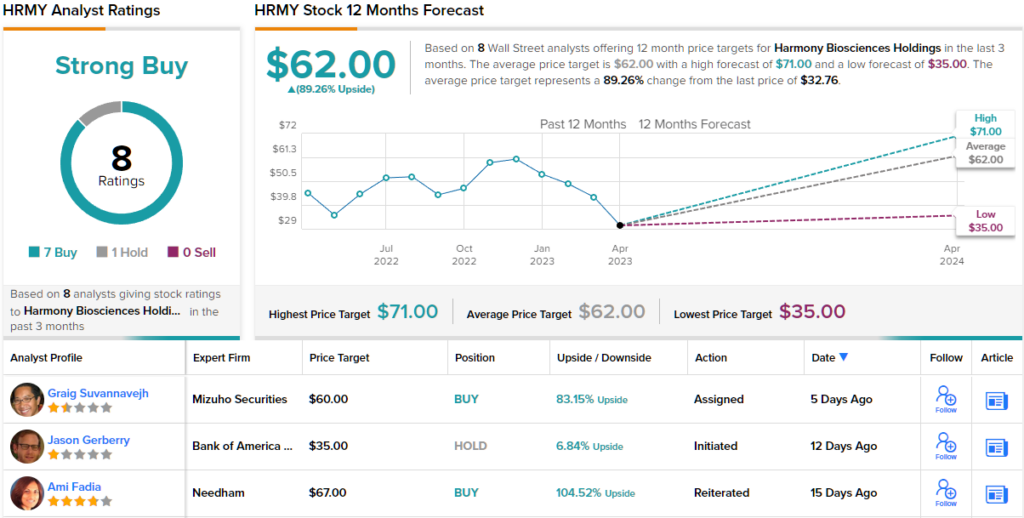

In fact, Brill thinks the shares are severely undervalued. Along with an Outperform (i.e., Buy) rating, the analyst has a $62 price target for the shares, indicating room for growth of 89% in the year ahead. (To watch Brill’s track record, click here)

Barring one fencesitter, all of Brill’s colleagues agree here. With an additional 6 Buys vs. a lone Hold, the stock claims a Strong Buy consensus rating. The $62 average target is identical to Brill’s objective. (See HRMY stock forecast)

Bowlero Corp. (BOWL)

As its name and ticker implies, Bowlero is a company involved in bowling activities. More specifically, the company owns and runs more than 325 high-end bowling centers across the U.S., Canada, and Mexico, making it the world’s leader in bowling entertainment. Furthermore, in 2019, the company purchased bowling’s major league, the Professional Bowlers Association, which boasts thousands of members and a global fan base in the millions. Lane/equipment fees aside, the company also generates additional income from F&B (food and beverages), merchandise, and extra-charge diversions such as arcades/gaming.

The company delivered a robust set of financial results in the most recently reported statement – for the fiscal second quarter of 2023 (January quarter). Revenue reached a record $273.4 million, amounting to a 33.2% YoY increase and beating the forecast by $16.58 million. Adjusted EBITDA reached $97.0 million, 45.2% higher compared to the same period a year earlier.

BOWL has only been a public entity since December 2021, having entered the markets via a SPAC merger. However, in contrast to many companies that went public via the blank cheque route and suffered badly during 2022’s bear, BOWL shares have done well, and have gained 33% over the past 12 months.

Nevertheless, at 28.53%, the short percentage of the float (as of Apr 13) is very high. But for Stifel analyst Steven M. Wieczynski, those betting against BOWL are in for a rude awakening.

“The legendary bowler Pete Weber once proclaimed, ‘Who do you think you are? I am!,’” quoted Wieczynski, making good use of his bowling knowledge. “In our opinion, no better words could be used to describe how we view the long-term growth story of BOWL. What we mean is we believe BOWL sits at the beginning of a compelling growth story with a dominant position in a fragmented market, a rich opportunity set of assets to roll-up, a successful acquisition and margin expansion blueprint, and powerful secular tailwinds. Putting that all together, it’s been a long time since we have come across a story within our universe with such strong growth characteristics.”

Quantifying these bullish comments, Wieczynski rates BOWL a Buy, to go alongside a $26 price target. This suggests the shares will deliver returns of 76% over the coming year. (To watch Wieczynski’s track record, click here)

The short sellers might be lining up, but Wall Street’s analysts all agree this is a stock to own. Based on Buys only – 7, in total – the stock claims a Strong Buy consensus rating. Going by the $21.17 average target, investors will pocket returns of ~44% in a year’s time. (See BOWL stock forecast)

Sunnova Energy (NOVA)

Let’s change gears once again and turn to the renewable energy sector for our final heavily shorted name. Sunnova Energy is a leading US provider of residential solar power installations. The company’s offerings run the full gamut of home solar installation services – from putting the rooftop panels in place to setting up storage batteries to providing repairs and replacing equipment when required. Additionally, the company also provides financing for the purchase whilst also offering insurance and maintenance plans. Sunnova operates in 41 states and territories and counts a customer base of 309,300.

30,100 of those were added in the first quarter of 2023, while the company increased its full year customer additions guide to between 125,000 and 135,000 from the prior 115,000 to 125,000.

Elsewhere in the recently reported Q1 statement, the revenue haul increased dramatically by 146% from the same period a year ago to $161.7 million, in turn beating the Street’s call by $2.16 million. However, at the other end of the scale, the losses piled up; the company delivered a net loss of $110 million compared to a loss of $22 million a year ago. This resulted in EPS of -$0.70, worse off than the -$0.59 anticipated by the analysts.

Many might think the losses are set to continue, making the stock one to stay away from – the short percentage of NOVA’s float stood at 30.42% (as of Apr 13).

However, that’s certainly not the view of Baird analyst Ben Kallo. Scanning the recent print, Kallo finds plenty to be upbeat about.

“NOVA increased its customer addition guidance by 10K at the midpoint and cited increased confidence in its ability to service new markets after expanding its credit facilities and securing a pathway to low-cost capital,” the analyst explained. “We are encouraged by signs of a deflationary environment and believe lower costs for batteries and other equipment will lead to increases in NOVA’s battery attach rate and number of services per customer. We continue to believe the long-term setup is strong.”

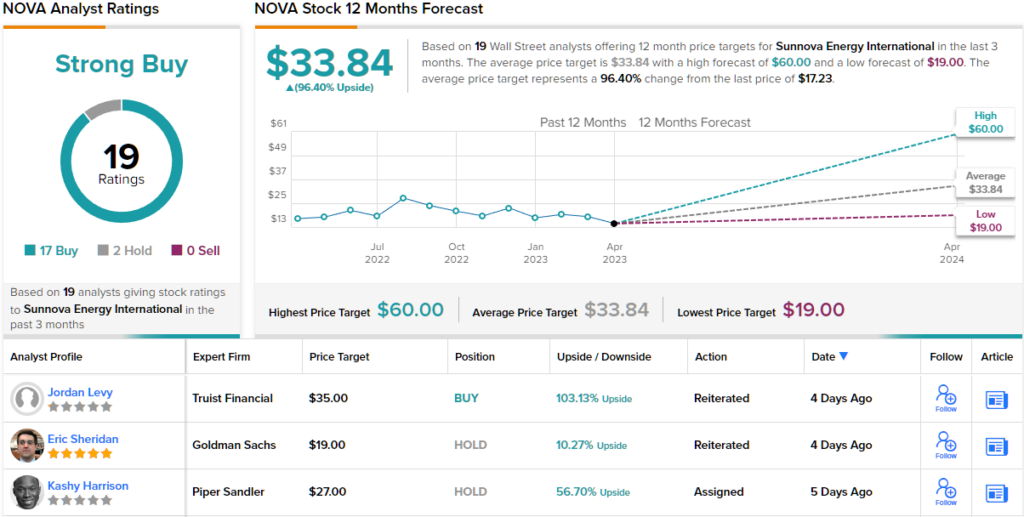

Calling NOVA a ‘Fresh Pick,’ Kallo has an Outperform (i.e., Buy) rating for the shares, backed by a $44 price target. The implication for investors? Upside of a big 145% from current levels. (To watch Kallo’s track record, click here)

All in all, NOVA gets strong support from the rest of the Street. Based on a total of 17 Buys and 2 Holds, the stock claims a Strong Buy consensus rating. The forecast calls for one-year gains of 96% considering the average target clocks in at $33.84. (See NOVA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.