After a prolonged bull rally, volatility once again rules the markets. The S&P 500 finished the week in the green, but Friday June 19’s session saw dramatic swings due to technical factors as well as alarming headlines related to a COVID-19 resurgence and a slowdown in the economic recovery.

Against this backdrop, what investors want, what will really bring back the animal spirits of the marketplace, is long-term stability. They aren’t looking to day trade; they are looking to park their money and watch it grow. Fiscal stimulus policies have pushed interest rates down to near zero. Treasury bonds are yielding less than 1%. This leaves the stock market. Fortunately, Wall Street pros believe compelling plays are still out there.

Today, we’ve pulled up three stocks from the TipRanks database that have sparked the interest of Wall Street’s analysts. These are stocks that have impressed the analysts, who have responded by noting their solid upside potential and clear investment value for the long haul, with each ticker earning a “Strong Buy” consensus rating. For all three, an analyst has noted the long-term potential in the headline. Let’s find out why they’re so compelling.

Sportsman’s Warehouse (SPWH)

Based in Utah, Sportsman’s Warehouse operates 95 retail locations in 25 states. The chain specializes in outdoor gear and clothing, for a clientele heavily involved in camping, fishing, hunting, and shooting.

The first thing to note, when assessing SPWH as an investment, is the recent stock performance. SPWH shares have climbed an astounding 145% over the last three months. The stock does not pay a dividend, but the recent share appreciation delivers a fine return.

The next thing to note is that the company beat the forecast in its most recent quarterly report. This win came despite it being an outdoor apparel and equipment chain during the lockdowns of recent months. Some points to note: SPWH operates in rural regions, where the coronavirus pandemic was less severe, and the calendar Q2 is, for seasonal reasons, the company’s slowest. In this most recent quarter, SPWH posted a 1-cent profit instead of the 6-cent loss expected.

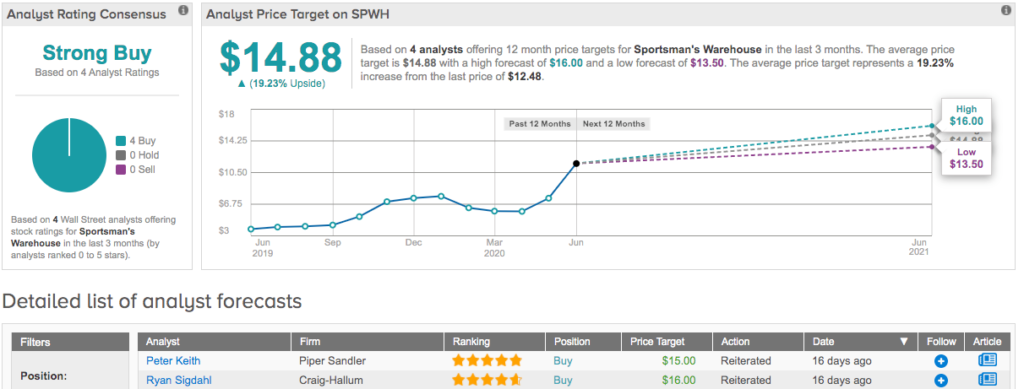

5-star analyst Ryan Sigdahl, of Craig-Hallum, calls SPWH in his headline, “One Of The Best Positioned Retailers In The Near And Long Term.” Going into detail, he elaborates: “We believe SPWH is one of the best positioned specialty retailers in the current environment (COVID and social unrest) as it has spurred demand for necessities and personal protection, but it is also one of the best positioned over the medium term with several key competitors de-emphasizing/exiting the ‘hunting’ category (market share opportunity) and increased participation in outdoor recreation. Shelter-in-place restrictions have driven increased interest in camping, hiking and fishing, and we don’t think these trends will change anytime soon.”

Sigdahl’s Buy rating on the shares is supported by his new $16 price target, which was raised from $12. This indicates confidence in a robust 28% upside potential for the coming year. (To watch Sigdahl’s track record, click here)

With 4 Buy ratings, the Strong Buy analyst consensus view on SPWH is unanimous. The stock has risen sharply in recent weeks, but the analysts have set their sights higher, and see room for continued growth. Shares are selling for $12.48 apiece, and the average price target of $14.88 implies a one-year upside potential of 19%. (See Sportsman’s Warehouse stock analysis on TipRanks)

Ciena (CIEN)

Next up is a telecom company, the world leader in optical connectivity. Ciena is a major name in networking equipment and software services. The company boasts an $8.2 billion market cap, over 2,000 patents, and 1,500 customers, as well as a presence in 35 countries. Ciena’s products include software for analytics and intelligence, control and automations, and programmable infrastructure.

This is another company that has strongly outperformed the markets in recent months. CIEN shares are up 49% over the last three months, gaining on the company’s usefulness as millions of workers switched to remote work and telecommuting. Like many companies, Ciena did see a dip in Q1 earnings, but that was mitigated by two related points: calendar Q1 is the lowest earning quarter in the company’s cycle, and earnings bounced back strongly in Q2. That most recent quarter showed non-GAAP profits of 76 cents per share, which was well above the estimates.

Covering the stock for J.P. Morgan, 4-star analyst Samik Chatterjee calls it an “attractive long-term investment,” and rates CIEN a Buy. His $63 price target, raised from $53, implies an upside potential of 17% for the coming 12 months. (To watch Chatterjee’s track record, click here)

Fleshing out his opinion, Chatterjee writes, “We recommend CIEN shares as our top pick within Networking Equipment coverage given favorable positioning with: 1) secular growth for the underlying optical industry levered to growing bandwidth needs; 2) benefit from accelerating bandwidth needs in a post-COVID-19 normal; 3) continued share wins from well-established technology leadership…”

CIEN shares have 16 recent analyst reviews, including 12 Buys and 4 Holds, giving the stock a Strong Buy consensus rating. Rapid share appreciation recently has pushed the trading price close to the price target – but the stock still shows a healthy 14% upside potential. Shares are trading for $53.62, and the average price target is $61.27. (See Ciena stock analysis on TipRanks)

Science Applications International Corporation (SAIC)

Last on our list, Science Applications, is a Washington DC consulting firm and government contractor. Like all of the ‘Beltway Bandits,’ SAIC is heavily dependent on the Federal government for revenues; fortunately for the company, that’s a well that typically does not run dry. SAIC provides engineering, scientific, and technology expertise to governmental service agencies.

While shares are down since the start of 2020, SAIC has gained 54% over the last three months.

Aside from share appreciation, SAIC also offers investors a reliable dividend payment. The company recently declared its next payment, at 37 cents per share, to go out in July. SAIC has been keeping the dividend reliable, and slowly growing the payment, for the past seven years. The current payment provides a yield of 1.8%. While this doesn’t sound like much, it beats the tech sector peer average by a full half-percentage point.

SAIC has been able to weather the coronavirus storm, at least in part by winning several new US government contracts in recent months. The company won a $655 million contract with the Air Force, and a $325 million contract with the Department of Homeland Security, in February. Both contracts are IDIQ – indefinite delivery, indefinite quantity. In May, the company signed a $650 million national security contract, and earlier this month, it signed a contract for torpedo testing with the US Navy.

The run of new contracts gives SAIC a stable foundation going forward, which has not escaped the notice of the analysts. Josh Sullivan, 5-star analyst with Benchmark, says that the “Record IDIQ Contracts Supports Long-term,” and in his comments writes, “2021 FCF outlook improved to $500 million from $450 million… the record IDIQ wins in the quarter supports the long-term momentum…”

Sullivan puts a Buy rating on SAIC, with a $105 price target to suggest room for 31% upside potential. (To watch Sullivan’s track record, click here)

8 Buy ratings and just a single Hold give SAIC shares a Strong Buy from the analyst consensus. The average price target is an even $100, and indicates an upside potential of 24% for the coming year. (See Science Applications International stock analysis on TipRanks)