Shares of ride-hailing giant Uber (NYSE:UBER) went public in May 2019 at $45 per share. Since its IPO, Uber stock has returned just over 54%, trailing the S&P 500 Index (SPX) by a wide margin (the SPX nearly doubled in the same period). However, with a market cap of $134 billion, Uber is among the most recognizable brands globally and is poised to benefit from multiple secular tailwinds. I believe UBER stock is an attractive investment this year. I am bullish on the company due to its steady revenue growth, improving profit margins, and the massive potential in the autonomous driving space.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Uber Slumps Post Q1 Results

Shares of Uber are down more than 7% in the past month, primarily due to its earnings miss in Q1. The company reported revenue of $10.13 billion and a loss per share of $0.32 per share. Analysts forecast revenue at $10.11 billion and adjusted earnings at $0.23 per share in the March quarter. Uber increased sales by 15% year-over-year but reported a net loss of $654 million due to unrealized losses totaling $721 million related to its equity investments.

However, Uber’s user base rose by 15%, while gross bookings were up 20% year-over-year. So, the company continues to expand its customer base and customer spending, resulting in steady top-line growth. It seems that while consumer spending is slowing across discretionary retail verticals, services such as ride-hailing and food delivery are experiencing strong demand.

Notably, Uber’s operating income stood at $172 million in Q1, compared to a loss of $262 million in the year-ago period. It expects to end Q2 with an adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) of between $1.45 billion and $1.53 billion, an increase of 58-67% year-over-year, respectively.

Uber’s resilient consumer demand for rides and food delivery, as well as higher profit margins, should help it generate organic cash flows amid a challenging macro environment.

In Q2, Uber expects gross bookings between $38.75 billion and $40.25 billion, indicating 18-23% year-over-year growth. Comparatively, Uber’s gross bookings grew by 19% in 2023. An acceleration in gross bookings is an encouraging sign as consumers continue to wrestle with elevated interest rates and inflation.

A Trillion-Dollar Market?

In Q1 of 2024, Uber paid its drivers $16.6 billion, which was the company’s largest expense. However, given the developments surrounding autonomous driving, the company may completely eliminate this cost within the upcoming decade.

Last year, ARK Invest’s Cathie Wood estimated the autonomous ride-hailing industry to generate $4 trillion in sales by 2028, which might be an ambitious outlook, given that self-driving cars have yet to be approved by the majority of the states in the U.S.

According to a Statista report, Uber has a 25% market share in the ride-hailing space. So, if it can command a similar share in autonomous driving, the company could add a whopping $1 trillion in sales, making it among the largest companies globally.

If we assume a 10% cash flow margin, Uber’s autonomous driving business may generate $100 billion in free cash flow if Wood’s estimates are accurate.

The Network Effect

Among the major benefits of marketplaces is that companies benefit from network effects and economies of scale. After reporting several years of losses, Uber is now turning the corner in terms of profitability.

As drivers and restaurants continue to join the Uber ecosystem, its services become all the more valuable to stakeholders. Creating a profitable marketplace may take several years. However, once the company achieves scale, delivering consistent profits is well within reach.

Despite its huge size, Uber is focused on entering new markets as it aims to gain traction in existing ones. In recent months, Uber announced a partnership with Instacart (NASDAQ:CART) and announced the acquisition of Foodpanda, indicating that the potential for market penetration is far from over.

Is Uber Stock Overvalued?

Analysts tracking Uber stock expect its adjusted earnings per share to grow from $0.81 in 2023 to $0.90 in 2024 and $2.10 in 2025. So, priced at 30.6x 2025 earnings, Uber stock might seem expensive, given that the sector median multiple is much lower at 19.1x. However, Uber’s high growth estimates allow it to command a higher multiple.

Alternatively, Uber’s free cash flow in the last 12 months totaled $4.17 billion. So, the stock is priced at 32x trailing free cash flow, making it a high-risk investment, especially if profit growth doesn’t materialize.

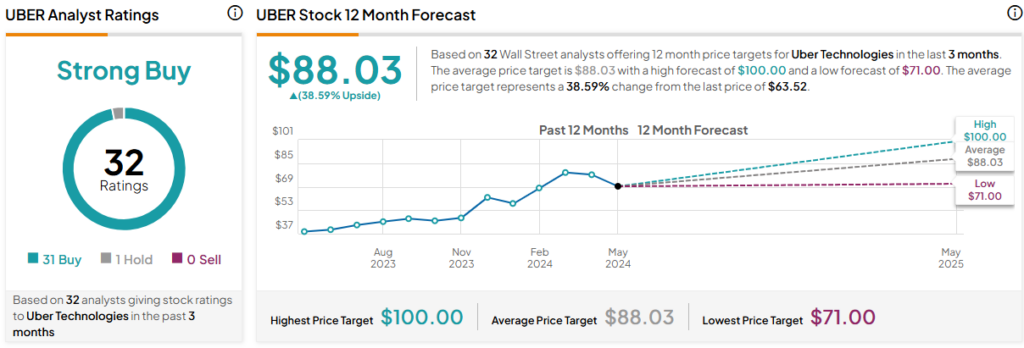

Is UBER Stock a Buy, According to Analysts?

Out of the 32 analyst ratings given to Uber stock, 31 are Buys, one is a Hold, and none are Sells, indicating a Strong Buy consensus rating. The average UBER stock price target is $88.03, implying upside potential of 38.6% from current levels.

The Takeaway

In my view, Uber’s expanding ecosystem and the autonomous driving megatrend make it a compelling investment choice for this year, especially if you can look beyond its high valuation. Allocating a small portion of your equity portfolio to Uber can possibly help you benefit from market-beating gains in 2024 and beyond.