Sometimes, playing the stock market can be like playing with a toddler. You just have to make sure to remember how to play opposites. Or, as Warren Buffett put it, “Be fearful when others are greedy, and greedy when others are fearful.”

It’s human nature to want to buy when prices are going up – you’ve heard of FOMO. But you need to keep that impulse at bay, because the time to buy, as Buffett would explain, is when prices are falling. That’s when you’ll find the true bargains.

The key is to find the oversold stocks, those that are showing depressed share prices alongside sound fundamentals. And to find them, we can check with both the data and the experts.

We’ve used the TipRanks database to pull up the latest scoop on three stocks that show all the signs of being oversold, and meet a profile: the Street’s analysts consider them to be Strong Buys, they are showing high upside, even in triple digits, and their share prices are way down. Let’s dive in.

AppLovin (APP)

We’ll start in the software sector. AppLovin is a platform for mobile app developers, offering tools to optimize app creation and marketing, at any scale. The platform supports monetization, as well, and brings a flexibility that app developers can use to their advantage. AppLovin also offers app publishing, advertising, and analytic services. The company’s total revenue is split roughly 2 to 1 between App revenue and software platform revenue.

The total top line is impressive. AppLovin had $793 million in total sales in 4Q21, the last reported, for 56% year-over-year growth. Of that total, $247 million was business software revenue, while Apps revenue came in at $547 million. These top line numbers led to a net income for the quarter of $31 million, which was a dramatic turnaround from the $19 million net loss in the year-ago quarter.

Since going public one year ago, AppLovin has seen its revenues climb consistently – and the Q4 numbers, reported this past February, were record results for the company. For the full year 2021, AppLovin’s growth was even more impressive: revenues grew 92% y/y to reach $2.8 billion, and the full-year net income of $35 million was lightyears ahead of the $126 million loss reported in 2020.

Despite posting strong numbers for recent quarters, shares have suffered great losses amid investor worries over growth deceleration (56% in Q4 vs 90% in Q3). Furthermore, the midpoint of AppLovin’s 2022 topline guidance was $3.7 billion, below the expectations, which had been hoping for guidance of $3.83 billion. Overall, AppLovin shares have lost 59% of their value this year.

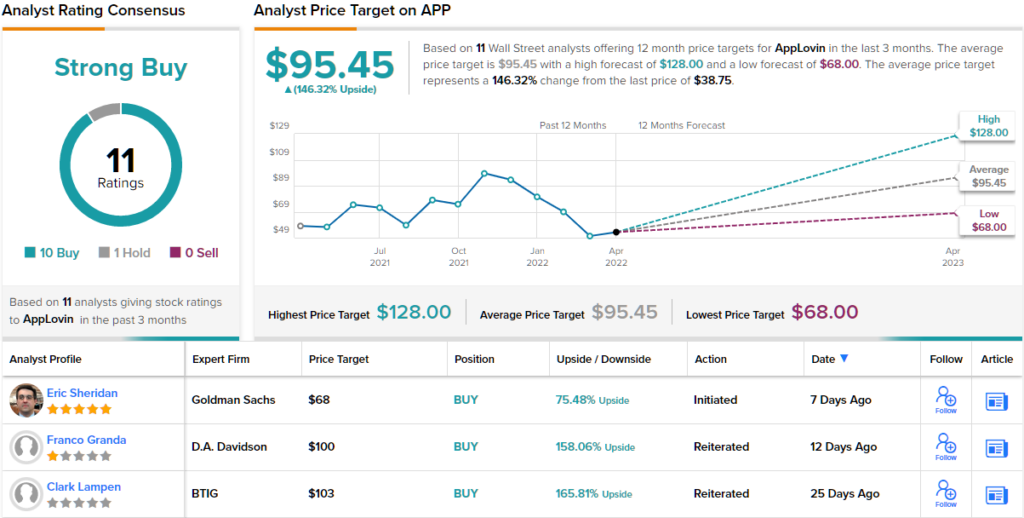

That said, D.A. Davidson analyst Franco Granda likes the current set up and believes AppLovin shares are well oversold.

“We are highlighting AppLovin as another company in our coverage that has been oversold over the past couple of months. Now that the company has achieved significant scale on its Apps business, focus is shifting towards growing the Software Platform that is on the verge of becoming the largest mobile AdTech ecosystem. The current sub-6x EV/’22 sales valuation multiple is unsustainable, in our view, as one would struggle to find other high-growth software companies with a financial profile close to APP’s trading at similar multiples. The disconnect between price and business trajectory presents a buying opportunity,” Granda explained.

These comments support Granda’s Buy rating on the stock, while his $100 price target implies a one-year upside of ~158%. (To watch Granda’s track record, click here)

The bulls are clearly running for this stock, as the 11 recent analyst reviews include 10 to Buy and only 1 Hold. The stock is selling for $38.64 and has an average price target of $95.45, indicating room for 146% share appreciation in the year ahead. (See APP stock forecast on TipRanks)

Kinross Gold Corporation (KGC)

Next up, Kinross Gold, is a mid-cap company– valued at $6.8 billion – with active mining operations in major gold-producing regions of the US, West Africa, and Brazil. But it’s also operating in Russia, and that has exposed it to heavy risk from the Russia-Ukraine war, the resulting trade disruptions, and the sanctions on Russia. Kinross shares, which are down 28% in the last 12 months, have been unable to regain traction this year.

Closing out 2021, Kinross reported in February that it had met last year’s production goals, with the total of 2.07 million gold ounces brought to the surface coming in at the lower half of the published guidance for the year. That production brought Kinross a free cash flow of $196 million for the year, of which just over $100 million came in 4Q21.

In a move to end its exposure to Russian risk factors, Kinross announced on April 5 that it had entered an agreement to sell 100% of its Russian assets. The agreement will see the buyer, Highland Gold, pay Kinross $680 million in cash.

Kinross has also entered an agreement to sell off a major part of its Ghana assets. The company will sell its 90% of its interest in the Chirano mine to Asante Gold, for $225 million in both cash and stock. The Ghanian government will continue to own 10% of that mine. The move, announced on April 25, allows Kinross to streamline its operations.

That streamlining bodes well for the future. Kinross is guiding toward significant increases in its output of gold ounces for the next three years, predicting 2.65 million in 2022 and 2.8 million in 2023. While the 2024 outlook is for 2.6 million, that remains higher than last year’s output. These increases in output are expected to fuel further free cash flow growth, allowing Kinross to continue returning cash to investors. In 2021, the company returned over $250 million to its shareholders.

Analyst Jackie Przybylowski, covering the stock for BMO Capital, takes an upbeat look at Kinross. He writes, “We continue to view Kinross as ‘oversold’ on the Russia risks. The sale of these assets alleviates much of the negative overhang the stock has faced since the start of the Russian conflict… We continue to see significant value from Kinross’s flagship Tasiast mine, as well as Dixie (recently acquired with Great Bear), Bald and Round Mountain, Paracatu and Kinross’s other assets.”

Przybylowski uses these comments to support an Outperform (i.e. Buy) rating on the KGC shares, and her $10 price target suggests a one-year upside of ~88%. (To watch Przybylowski’s track record, click here)

Overall, there are 15 recent analyst reviews on record for Kinross, breaking down 11 to 4 in favor of Buys over Holds and backing up the Strong Buy consensus view from the Wall Street analysts. KGC is selling for $5.18 and its $7.81 average price target implies an upside of ~51% in the next year. (See KGC stock forecast on TipRanks)

BioLife Solutions (BLFS)

We’ll wrap up in the biotech sector, with BioLife, a company that provides support services and products to the pharmacological research sector. BioLife produces and supplies a range of cold-storage for cell and gene therapy firms, including cryopreservation storage units, biopreservation for blood storage, and hypothermic storage and shipping media. In addition to cold storage, BioLife also provides cell thawing media to reverse cryopreservation and allow samples to be used in research labs.

BioLife’s revenues have been growing steadily since the second quarter of 2020, reflecting an ongoing demand for cold storage and transport in the biosciences industry. In the most recent earnings report, for 4Q21, the company showed $37.3 million at the top line, up 153% from the fourth quarter of 2020. Breaking down that revenue total, BioLife realized $14.8 million from its cell processing platform, $16.6 million from freezers and thaw systems, and $5.9 million form it storage and storage service platforms.

While revenue was up, the company’s gross margin fell year-over-year from 50% to 15%. The company attributed the fall in margins to a shift in its product mix and a series of inventory write-offs after last years’ acquisition of its competitor, Stirling. BioLife finished 2021 with $69.9 million in cash on hand, and is guiding toward 2022 revenue in the range of $159.5 million to $171.0 million. Achieving that revenue guidance will mean growth of 34% to 44% in 2022.

Even though the BioLife’s business showing was generally sound, the company’s stock is down 65% year-to-date.

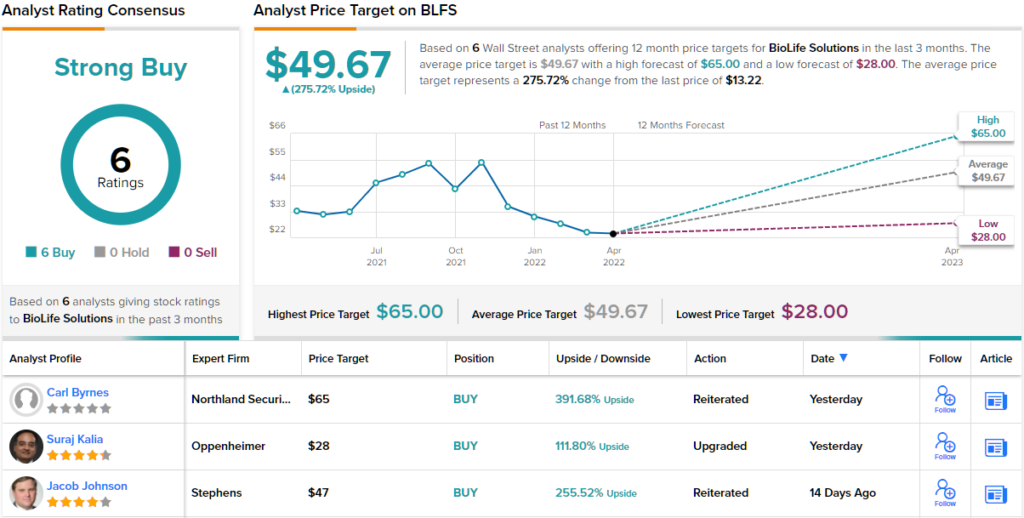

Stephens analyst Jacob Johnson likes what he sees in BioLife, saying: “As it relates to oversold small-cap growth names, BLFS is our Best Idea.”

Getting into details, Johnson writes, “While the Stirling operational issues will likely weigh on 1H22 margins, we are hopeful this headwind bottomed in 4Q21. If BLFS can show sequential margin improvement, we think the stock will begin to work. We think these Stirling moving pieces have masked otherwise strong performance at BLFS… In short, ex-Stirling, BLFS continues to post results that highlight the strength of the CGT end-market. With shares trading at 5x FY22 revenues (4x FY23) vs. a three-year average of 10x and CYRX at 6.5x/5x, we think BLFS shares remain too cheap.”

In line with those bullish comments Johnson gives BLFS shares a Buy rating, along with a $47 price target indicating a robust 257% one-year upside. (To watch Johnson’s track record, click here)

Other analysts don’t beg to differ. With 6 Buy ratings and no Holds or Sells, the word on the Street is that BLFS is a Strong Buy. The shares are selling for $13.22 and the $49.67 average target implies ~276% upside from that level. (See BLFS stock forecast at TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.