Jonathan Golub of Credit Suisse (CS) recently opined on stock valuations and concluded that cyclical stocks are trading cheaply.

According to Golub: “Cyclical valuations are the most favorable of any group, with Materials and Energy trading at the largest discounts relative to history.” He added that the financial services sector is looking up by stating that “among groups, Banks appear the most inexpensive relative to history.”

I agree with Golub’s take on the market. Here are three cyclical stocks that I’m bullish on.

Sibanye-Stillwater (SBSW)

After a nearly 40% year-to-date drawdown, Sibanye stock is in an investable territory. The South African precious metals mining company has been faced with various idiosyncratic problems lately, with its employees going on strike due to wage demands. In addition, the Montana region was hit with floods lately, subsequently disrupting its U.S. platinum group metals (PGM) operations.

Although 2022 has been a tough year for Sibanye, its operating capacity will likely pick back up soon, meaning its stock could bear fruit.

Furthermore, Sibanye stock is undervalued, which plays into Credit Suisse’s narrative. Firstly, the stock’s price-earnings ratio (3.87x) implies that Sibanye’s trading at a sector discount of 71.60%. In addition, Sibanye stock is underpriced relative to its sales as it exhibits a price-sales ratio of only 0.74x.

Alternatively, Sibanye provides a monumentous dividend with a yield of 9.52% and a payout ratio of 61.18%. Moreover, the stock’s dividend is sustainable, with a dividend coverage ratio of 2.76x.

Turning to Wall Street, Sibanye earns a Strong Buy consensus rating based on five Buy ratings and one Hold rating assigned in the past three months. The average SBSW stock price target of $19.08 implies 78.65% upside potential.

Bank of America (BAC)

Goldman Sachs (GS) recently included Bank of America stock in its rebalanced portfolio, which includes a variety of high Sharpe Ratio assets.

Bank of America is a solid option at the moment because it exhibits high-quality return metrics. For instance, its diluted earnings per share have surged by 50.80% during the past year and are forecasted to proliferate by another 27.96% in the following year. Also worth noting is the banking stock’s net income margin of 33.61%, which exceeds the sector median by 15.58%.

Bank of America’s solid financial statement metrics should be of no surprise, as it eclipsed its first-quarter earnings estimate by 80 cents per share amid surging deposits (+13% year-over-year) and a solid Common equity tier 1 ratio of 10.4%.

On the downside, the bank has a few cost issues to deal with in the wake of rising non-core inflation. However, the company’s CEO Brian Moynihan believes rising interest rates could soften the expenses over the full year as he was quoted saying: “At the end of the day, we’re saying expenses are flat this year, and NII improvement is going to flow to the bottom line.”

Bank of America’s stock is undervalued at the moment as its price/book ratio is at a 6.17% discount to its normalized average, and its PEG ratio of 0.17x implies that the stock market underscores its tremendous earnings-per-share growth.

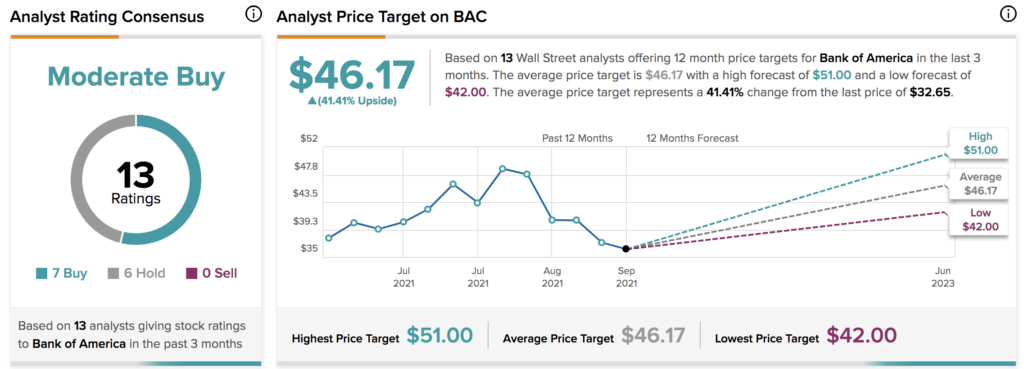

Turning to Wall Street, Bank of America earns a Moderate Buy consensus rating based on seven Buys and six Hold ratings assigned in the past three months. The average BAC stock price target of $46.17 implies 41.41% upside potential.

Matador Resources (MTDR)

Matador Resources is a high beta energy stock, meaning it’s the purest of pure conviction plays. Matador operates across the upper to midstream oil and gas space, with its operations based in the United States.

The company owns 124,800 acres of production in the Delaware Basin and 50% of a midstream joint-venture (San Mateo). Cohesively, the firm is able to market a competitively priced product at a reasonable cost. Matador is a growing energy firm, meaning its golden days in oil production are still ahead.

From a style-based analysis viewpoint, Matador is in prime shape. The company’s five-year EBITDA CAGR of 49.38% means that it’s adding value to its income statement at will. Moreover, the firm’s normalized net income five-year CAGR of 1.04x implies that much intrinsic value is being passed through to Matador’s shareholders.

Turning to Wall Street, Matador Resources earns a Strong Buy consensus rating based on eight Buys ratings assigned in the past three months. The average MTDR stock price target of $78.63 implies 59.11% upside potential.

Concluding Thoughts

Credit Suisse has highlighted the fact that cyclical stocks are undervalued. Whether cyclicals reach their full value or not is debatable. However, the stocks mentioned in this article are at good odds of living up to their potential.