If we learned anything in 2020 about the modern workplace and our digital footprints, it was the ongoing importance of solid cybersecurity. A look through the news from the past 18 months reveals the extent of the danger. A few examples will suffice – that identity theft spiked during the pandemic crisis, with the 1.4 million reports to the Federal Trade Commission (FTC) doubling the 2019 numbers; that on average, each data breach in 2020 incurred costs of $3.86 million; and that, by the year 2025, according to Cybersecurity Ventures, cybercrimes are projected to cost the global economy some $10.5 trillion per year.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

At a macro level, the scale of the problem is hard to conceive. So let’s scale down a bit, and look at cybercrime’s potential impact on companies. Here, the worries revolve around vulnerability. A recent IDG survey of more than 200 C-level IT professionals and execs found that 78% are not confident their organizations are prepared to meet the possible threats. Another statistic: in a major cybersecurity industry survey, it was found that in 53% of companies, there were more than 1,000 sensitive files open for every employee. The lack of protection is mirrored in careless use; only 5% of companies’ folders – just the ordinary information folders used in every computer memory – have any sort of proper data protection.

What this means going forward can be measured in dollars and cents, and opportunity. Cybersecurity is a huge market, meeting an essential need in today’s digital society, the market for cybersecurity services and products is predicted to see a compound annual growth rate approaching 12.5% for the next several years, to reach $403 billion by 2027. This will open up enormous vistas for investors.

Using the TipRanks platform, we’ve looked up three cybersecurity stocks that have attracted recent notice from Wall Street’s analyst corps. These are Buy-rated names, for which these analysts project at least 30% upside potential in the year ahead. Let’s take a closer look.

Zscaler (ZS)

We’ll start with Zscaler, a large-cap firm that brings cybersecurity through cloud applications. The company operates data centers supporting cloud-based security apps, designed to protect internet access and local applications. The company aims to provide secure internet use, so that customers can use the existing internet as a network – safely. Zscaler boasts more than 400 of the Forbes Global 2000 companies among its customers.

In February this year, Zscaler reported its fiscal Q2 results, and showed strong growth across the board. Revenue was up 55% year-over-year, reaching $157 million, driven by billings growth of 71%, to $232 million. The company’s cash flows improved dramatically over the past year; in the recent Q2, operating cash flow increased from $5.4 million last year to $30.4 million, while free cash flow rose from a negative $1.9 million to $18 million.

Zscaler is making moves to grow by acquisition, as well. The company announced in April that it will be entering into an acquisition agreement with the cloud security posture management company (CSPM) Cloudneeti, a move that will make Zscaler’s cloud security platform available to Cloudneeti’s existing customer base. While transaction terms were not disclosed, the move is expected to close during Zscaler’s fiscal third quarter.

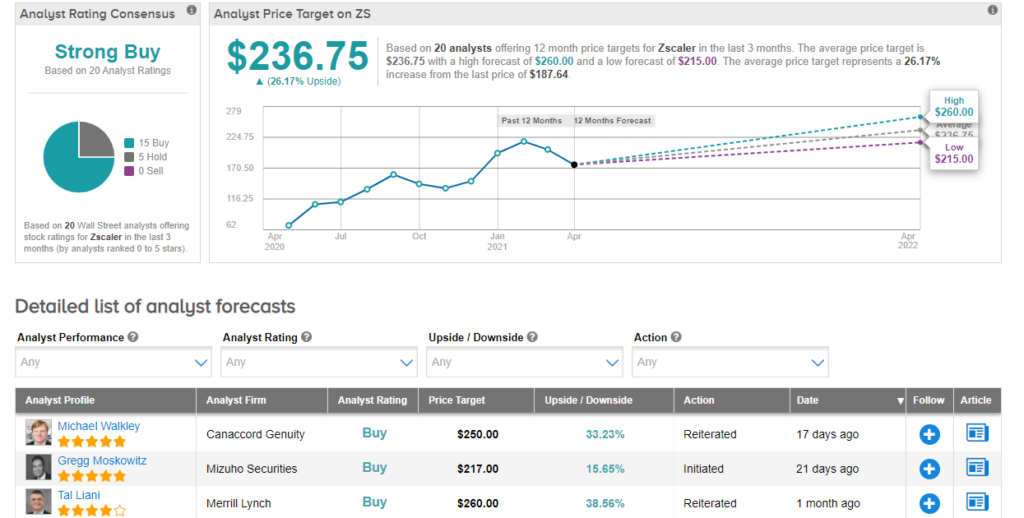

Covering this company from Canaccord Genuity, 5-star analyst Michael Walkley writes, “Our positive thesis is based on the company’s ability to securely facilitate customers’ cloud adoption initiatives, which is disrupting an estimated $20B+ spent annually on the entire perimeter defense stack. We believe Zscaler is a core centerpiece of a robust cybersecurity framework and expect the company will continue to deliver ~30%+ topline growth to $1B+ in revenue in F2023E with accelerating operating leverage and FCF generation as the market continues to converge on native cloud security and zero trust principles.”

Walkley’s comments support his Buy rating on the stock, and his $250 price target implies a strong upside of 33% for the next 12 months. (To watch Walkley’s track record, click here.)

Walkley is no outlier in his bullish take on Zscaler; the company has a Strong Buy rating from the analyst consensus, based on 20 reviews with a 15 to 5 breakdown between Buys and Holds. The shares are selling for $187.64, and their $236.75 average price target suggests an upside of 26% over the coming year. (See Zscaler’s stock analysis at TipRanks.)

Crowdstrike Holdings, Inc. (CRWD)

The next company on our list, Crowdstrike, is a $46 billion cybersecurity tech firm from Silicon Valley. It’s offerings include cyberattack response services, threat intelligence, and security for both workloads and endpoints. Crowdstrike has, in recent years, been involved in after-the-fact investigations of several high-profile cybersecurity breaches, including the Sony hack of 2014 and the hacks of the Democratic National Committee during the 2016 election cycle.

Crowdstrike has seen rapid growth in both revenues and share value in recent year. On the financial end, the company’s top line rose 74% year-over-year in the recent fiscal 2021 Q4, from $152.1 million to $264.9 million. This was supported in part by a 77% gain in subscription revenue, which hit $244.7 million in the quarter. Another key metric, annual recurring revenue, grew 75% year-over-year, and hit $1.05 billion by end of January 2021. Of the ARR, more than 14% was new net revenue added during the quarter. The company’s cash flow increased more than 3.5x during fiscal 2020, from $99.9 million to $356.6 million.

Like Zscaler above, Crowdstrike has been making acquisition moves in recent months. In September of last year, it completed an acquisition of Preempt Security, which provides Zero Trust and conditional access tech for threat prevention. More recently, this past March, Crowdstrike acquired Humio, the cloud-log management company, in a move worth almost $400 million. Of that total, 40 million was paid in stock and options, while $352 million was paid in cash.

Through all of this, CRWD shares have shown consistent growth. The stock is up 201% in the last 12 months.

This company’s strong, sustained growth has impressed Needham analyst Alex Henderson, rated 5 stars by TipRanks, who says, “We think investors will be rewarded for buying and holding onto these shares. We recognize the potential for downdrafts in CRWD from time to time as the company moves with market swings given its high beta. We are long-term buyers of CRWD for multi-year out-performance…. We think the estimates on the Street are overly conservative. We think the company is likely to grow in excess of 50% for the next 2-3 years and 30%-plus longer term.”

Henderson gives CRWD shares a Buy rating, along with a $275 price target that indicates his confidence in 32% stock appreciation for the year ahead. (To watch Henderson’s track record, click here.)

There is broad agreement on Wall Street with Henderson’s outlook, and Crowdstrike has earned 15 recent positive reviews – out of 18 published – to back its Strong Buy consensus rating. The stock is selling for $208.51, and has an average price target of $251.39, suggesting a 20% one-year upside from current levels. (See Crowdstrike’s stock analysis at TipRanks.)

FireEye, Inc. (FEYE)

Last up, FireEye, has been in the cybersecurity business since 2004 and is another of Silicon Valley’s large-cap tech firms. FireEye provides both software and hardware for protection against cyberattacks, along with investigative services, malware protection, and IT security risk analysis. The company has numerous high-profile clients, in the energy, communications, healthcare, financial, and government sectors.

FireEye has buffeted about in recent months, by a series of good and bad news cycles. Starting in November, the company was on an upswing, announcing its acquisition of Respond Software in a transaction valued at $186 million, paid in both cash and stock. The move gives FireEye access to Respond’s XDR engine, which can be integrated into FireEye’s Mandiant platform. Also in November, FireEye announced a $400 million strategic investment from a coalition led by Blackstone Tactical Opportunities. The funds made available to FireEye paid for the Respond acquisition, as well as supported company platform expansion.

In December, the news was mixed. FireEye acknowledged that its own network system had been breached. The cyberattack against this leading cybersecurity firm was carried out, according to FireEye, by a nation-state, and the hackers got away with a number of cybersecurity software tools. FEYE stock slipped on this news – but surged just days later when FireEye discovered and revealed publicly the highly sophisticated SolarWinds hack attack.

Despite the mixed headlines, FireEye’s recent 1Q21 financial results were solid. At the top line, revenue was up 10% year-over-year, coming in ahead of the consensus estimate by $9.3 million to reach $246 million. Annualized recurring revenue reached $643 million, up 9% yoy and a company record. FireEye’s cash flow shifted from negative $24 million one year ago to a positive figure of $21 million in 1Q21.

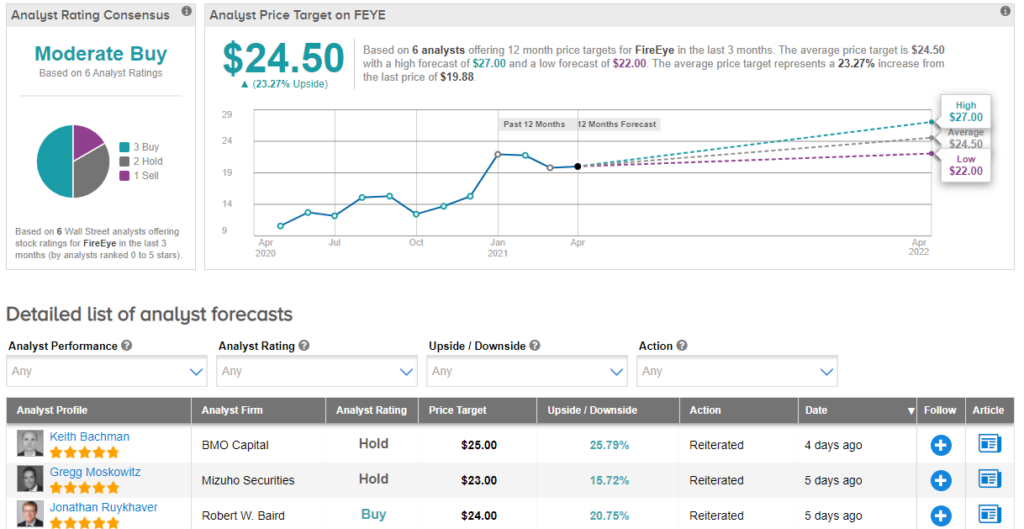

According to Catharine Trebnick, of Colliers Securities, FireEye’s success is based on the ongoing threat of cybersecurity attacks in the current digital environment. She writes, “Revenue outperformance was primarily due to strong adoption of cloud security products and Mandiant solutions. Management noted that the company continues to benefit from the heightened threat landscape, as the company uncovered numerous zero day exploits and threat actors over the course of the quarter.”

Trebnick gives FEYE shares a $26 price target, suggesting a 30% upside on the one-year time frame and backing her Buy rating. (To watch Trebnick’s track record, click here.)

The mixed news on FireEye has generated some mixed reviews from Wall Street, yet the bulls are still in control. The stock’s 6 recent ratings include 3 Buys, 2 Holds, and 1 Sell, making the analyst consensus view a Moderate Buy. The shares have an average price target of $24.50, which indicates a 23% upside potential from the trading price of $19.88. (See FireEye’s stock analysis at TipRanks.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.